Indonesia Stock Exchange (IHSG) Deep Learning Trading System

Paperium: IHSG Deep Learning Trading System

System Type: Deep Learning Quantitative Trading\ Target Market: Indonesia Stock Exchange (IHSG)\ Model Architecture: LSTM (Long Short-Term Memory)\ Labeling Scheme: Triple Barrier Method

Paperium is a sophisticated quantitative trading system for the Indonesia Stock Exchange (IHSG). It implements state-of-the-art Deep Learning (LSTM) trained on raw OHLCV sequences, guided by Triple Barrier Labeling, as described in recent financial machine learning research.

Paper: https://arxiv.org/pdf/2504.02249v1

[!IMPORTANT]

Paperium V0 and Paperium V1 still available in the branch section with differnt model architecture

Paperium Ensemble

Go train the paperium v1 xgboost model on paperium-v1 branch and combine it with paperium v2 to get more accurate signaling with entry and dynamic SL/TP, instead of fixed 3%.

Table of Contents

- Core Philosophy

- Key Innovations

- Architecture

- Quick Start

- Usage Guide

- Model Details

- Data Pipeline

- Training Strategy

- Portfolio Management

- Configuration

- Performance Optimization

- Known Issues & Future Work

Core Philosophy

Paperium has transitioned from traditional ML (XGBoost + Technical Indicators) to Deep Learning on Raw Data. The hypothesis is that neural networks can learn better feature representations from raw price sequences than human-engineered indicators (RSI, MACD, etc.).

By feeding the LSTM raw OHLCV data, we avoid:

- Feature selection bias

- Over-engineering indicators

- Look-ahead bias from complex transformations

Key Innovations

1. Deep Learning Core

Uses a 2-layer LSTM (Long Short-Term Memory) network instead of traditional tree-based models (XGBoost). LSTMs excel at capturing long-term dependencies in time-series data.

2. Raw Data Input

Eliminates "feature engineering" bias. The model learns directly from 100-day sequences of raw Open, High, Low, Close, Volume (OHLCV) data.

3. Triple Barrier Labeling (TBL)

Instead of fixed "Close-to-Close" returns, we use TBL to capture the path dependency of trading.

- Barrier 1 (Profit): +3% gain within horizon

- Barrier 2 (Loss): -3% loss within horizon

- Barrier 3 (Time): 5-day expiration (neutral)

- Result: The model predicts the probability of hitting the profit barrier first

- If High > Entry × 1.03 first → Label 2 (PROFIT)

- If Low < Entry × 0.97 first → Label 0 (LOSS)

- If neither happens by Day 5 → Label 1 (NEUTRAL)

Architecture

Directory Structure

paperium/

├── data/ # Data storage and fetching

│ ├── fetcher.py - Yahoo Finance API integration

│ ├── storage.py - SQLite database operations

│ ├── universe.py - Stock universe definitions

│ └── ihsg_trading.db - Price data storage

│

├── ml/ # Machine Learning components

│ ├── model.py - PyTorch LSTM implementation

│ └── features.py - Sequence generation & TBL logic

│

├── signals/ # Signal generation

│ ├── screener.py - Liquidity & circuit breaker filters

│ └── combiner.py - Signal aggregation (Pure ML confidence)

│

├── strategy/ # Portfolio management

│ ├── position_manager.py - Trade state persistence

│ └── position_sizer.py - Volatility-adjusted sizing

│

├── scripts/ # Executable workflows

│ ├── train.py - Main training loop (PyTorch)

│ ├── tune_lstm.py - Hyperparameter optimization

│ ├── eval.py - Backtesting engine

│ ├── signals.py - Stock prediction signals (ML-based)

│ ├── eod_retrain.py - Evening updates (post-market)

│ ├── sync_data.py - Data synchronization

│ ├── download_ihsg.py - Index data fetching

│ ├── optimize_tbl.py - Barrier optimization tool

│ └── clean_universe.py - Universe filtering

│

├── utils/ # Shared utilities

│ └── logger.py - Timestamped logging

│

├── models/ # Trained model checkpoints

│ └── best_lstm.pt - Production model

│

├── run.py # Main entry point (Interactive CLI)

└── config.py # System configurationComponent Status

| Component | Status | Notes | | ----------------------- | ---------- | ---------------------------------------- | | Data Fetcher | Stable | SQLite backend with hourly caching | | Screener | Simplified | Blacklist filtering for illiquid stocks | | Feature Engineering | Replaced | Generates sequences + TBL labels | | Model | PyTorch | Saved as best_lstm.pt | | Training | Active | train.py handles loop & early stopping | | Evaluator | Active | eval.py runs walk-forward backtest | | Signal Generator | Active | signals.py with confidence weighting |

Quick Start

1. Installation

# Install dependencies using uv

uv syncDependencies: PyTorch, Pandas, NumPy, Rich, yfinance, scikit-learn, SQLite3

2. Initial Setup

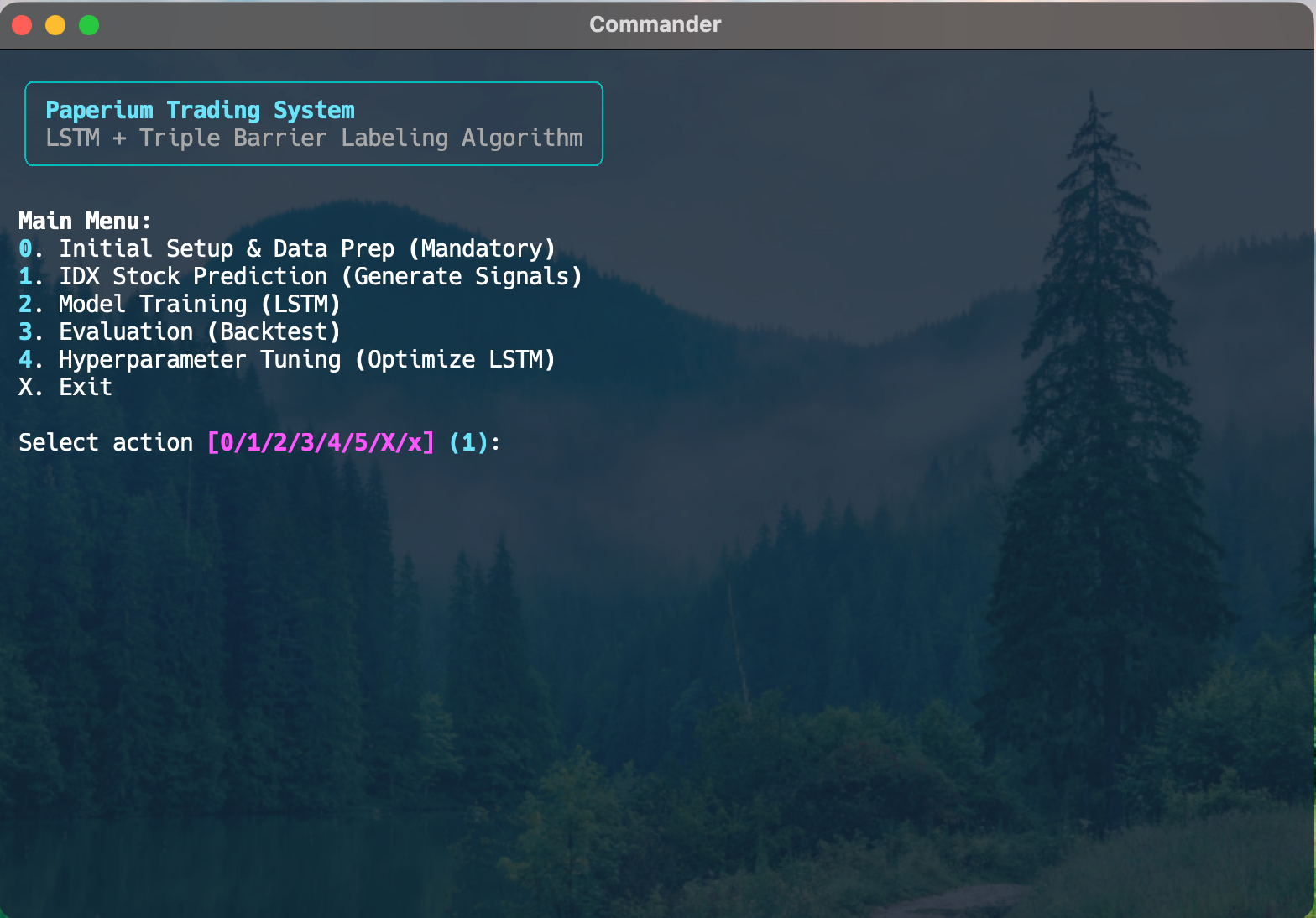

# Launch interactive menu

uv run python run.py

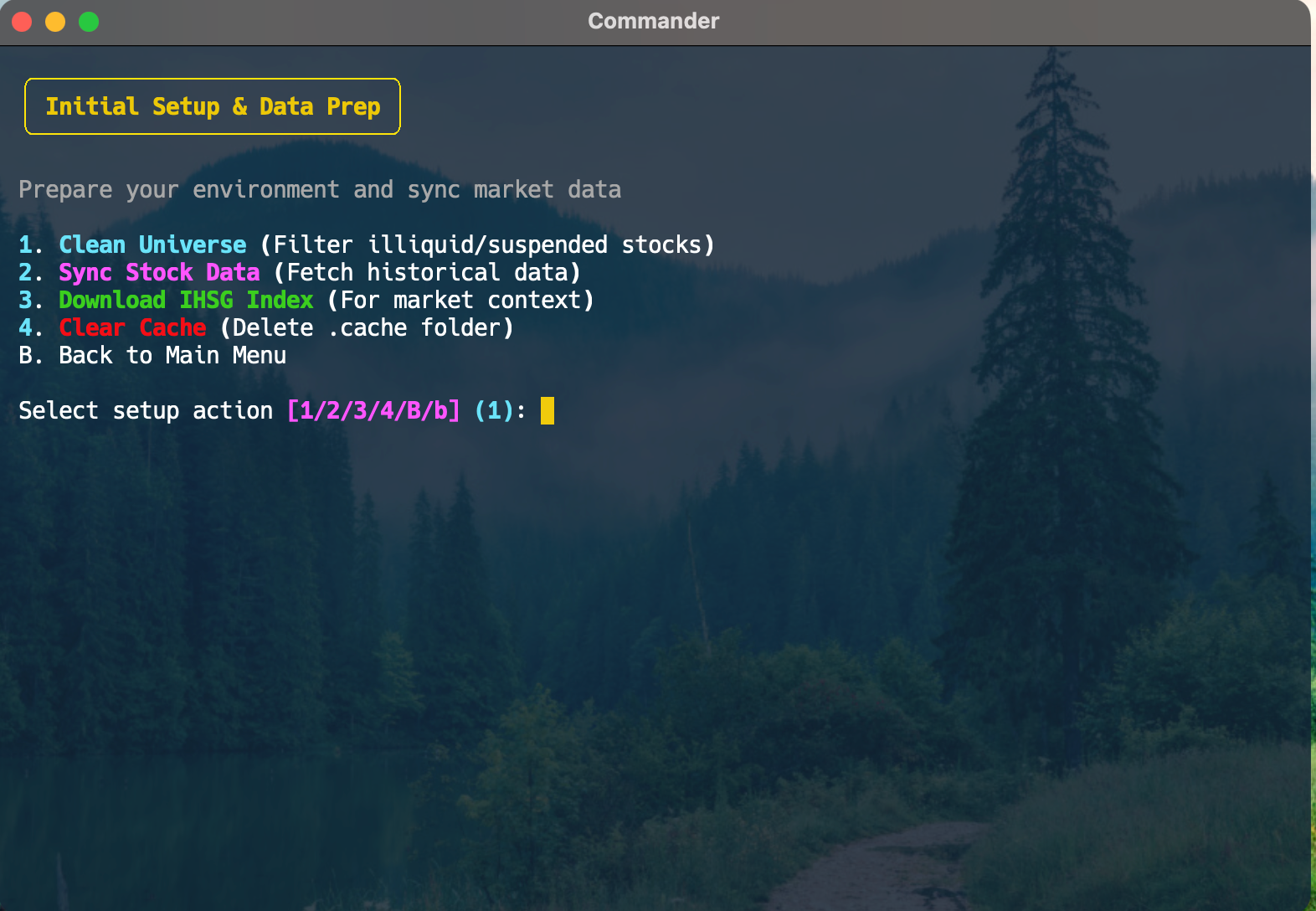

Select Option 0: Initial Setup & Data Prep, then:

- Clean Universe - Filter illiquid/suspended stocks

- Sync Stock Data - Fetch historical data (5 years recommended)

- Download IHSG Index - Market context data

3. Train Your First Model

From the main menu, select Option 2: Model Training

Choose:

- Fresh training: Start new model from scratch

- Retrain: Continue from existing

best_lstm.pt - Set epochs (default: 50)

The training dashboard will show:

- Real-time loss/accuracy metrics

- Batch-level progress

- Time elapsed/remaining

- Early stopping status

4. Generate Trading Signals

From the main menu, select Option 1: IDX Stock Prediction

This will:

- Load the trained model

- Scan the stock universe (filtered by blacklist)

- Generate ML-based buy signals

- Display predictions with confidence scores

- Optionally allocate capital across top N stocks with confidence weighting

Usage Guide

Main Workflows

Stock Prediction Signals

When: Before market opens (08:30 WIB) or anytime for analysis

# Basic mode - show all signals from database

uv run python scripts/signals.py

Fetch latest data from Yahoo Finance first

uv run python scripts/signals.py --fetch-latest

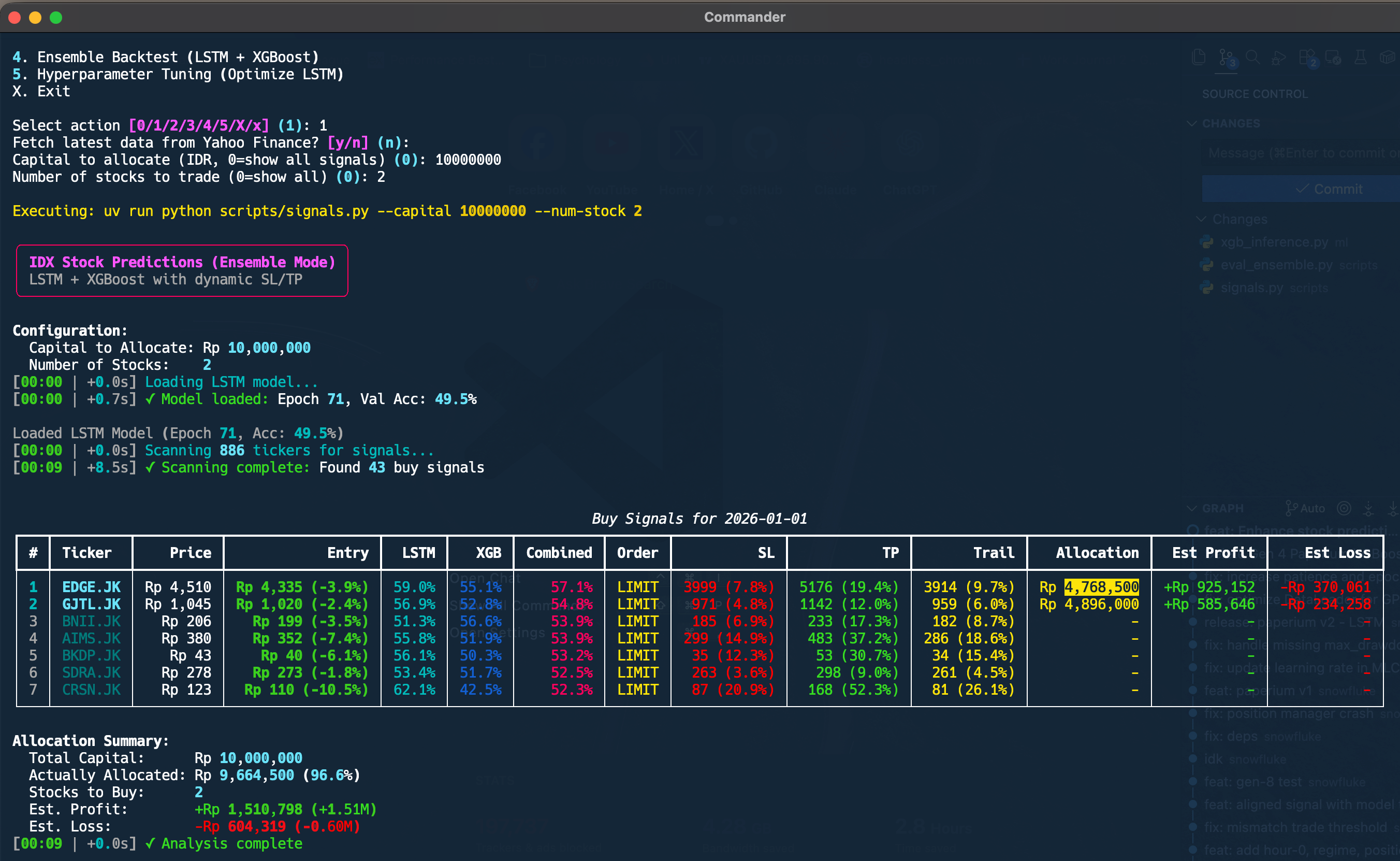

With capital allocation (confidence-weighted)

uv run python scripts/signals.py --capital 100000000 --num-stock 5

Fetch latest + allocate capital

uv run python scripts/signals.py --fetch-latest --capital 50000000 --num-stock 3What it does:

- Optionally fetches latest market data from Yahoo Finance

- Runs LSTM inference on all tickers

- Filters blacklisted stocks (illiquid/suspended)

- Ranks signals by confidence (Class 2 probability > 50%)

- With allocation: confidence-weighted capital distribution across top N stocks

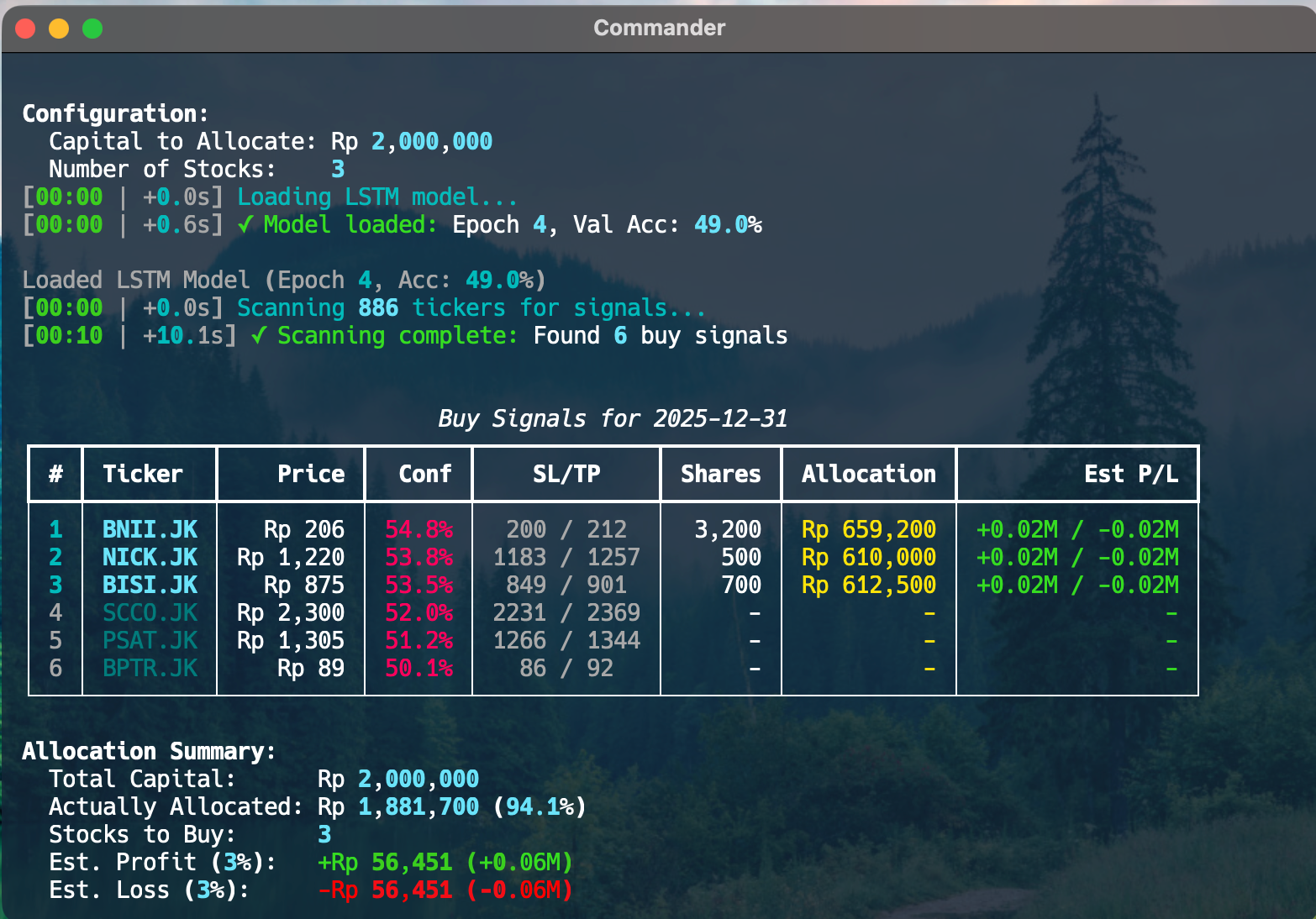

Configuration:

Capital to Allocate: Rp 100,000,000

Number of Stocks: 5

Buy Signals for 2025-01-01 ┏━━━┳━━━━━━━━┳━━━━━━━━━━━┳━━━━━━┳━━━━━━━━━━━┳━━━━━━━━┳━━━━━━━━━━━━━━┳━━━━━━━━━━━━━━━━━━━┓ ┃ # ┃ Ticker ┃ Price ┃ Conf ┃ SL/TP ┃ Shares ┃ Allocation ┃ Est P/L ┃ ┡━━━╇━━━━━━━━╇━━━━━━━━━━━╇━━━━━━╇━━━━━━━━━━━╇━━━━━━━━╇━━━━━━━━━━━━━━╇━━━━━━━━━━━━━━━━━━━┩ │ 1 │ BBCA │ Rp 9,500 │ 72% │ 9215/9785 │ 4,000 │ Rp 38,000,000│ +1.14M / -1.14M │ │ 2 │ ASII │ Rp 5,200 │ 65% │ 5044/5356 │ 5,800 │ Rp 30,160,000│ +0.90M / -0.90M │ │ 3 │ BBRI │ Rp 4,800 │ 58% │ 4656/4944 │ 4,100 │ Rp 19,680,000│ +0.59M / -0.59M │ └───┴────────┴───────────┴──────┴───────────┴────────┴──────────────┴───────────────────┘

Allocation Summary: Total Capital: Rp 100,000,000 Actually Allocated: Rp 87,840,000 (87.8%) Stocks to Buy: 5 Est. Profit (3%): +Rp 2,635,200 (+2.64M) Est. Loss (3%): -Rp 2,635,200 (-2.64M)

Key Features:

- Blacklist Filtering: Automatically excludes 72 illiquid/suspended stocks

- Confidence Weighting: Higher confidence signals get larger allocation

- Latest Data: Optional

--fetch-latestensures up-to-date predictions - Flexible Display: Shows all signals or only allocated positions

Model Training

Command line:

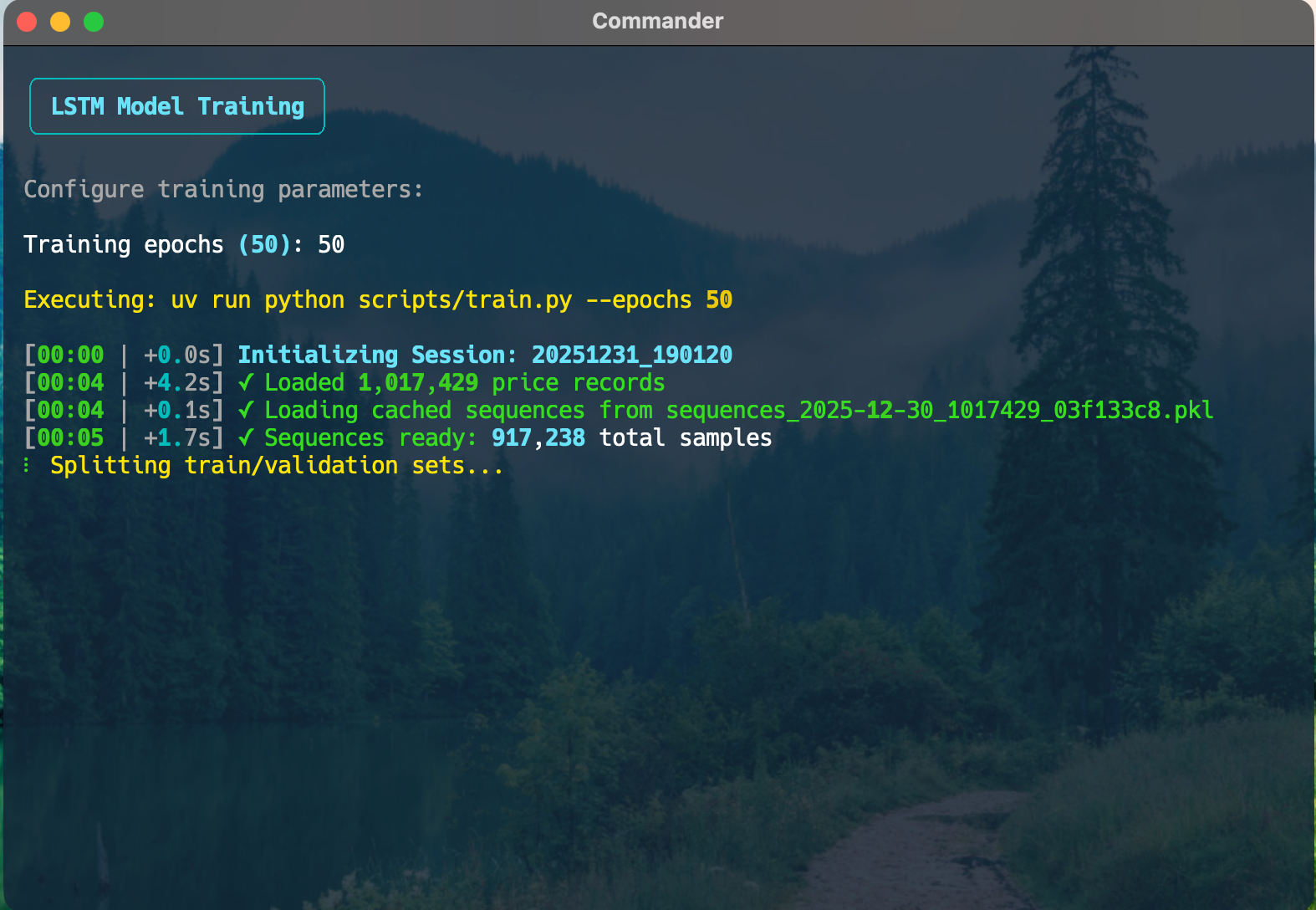

# Fresh training

uv run python scripts/train.py --epochs 50

Retrain from best model

uv run python scripts/train.py --epochs 50 --retrain

Resume from specific checkpoint

uv run python scripts/train.py --resume models/session_X/last.ptInteractive menu:

uv run python run.py

Select: 2. Model Training

Features:

- Real-time training dashboard with batch progress

- Timestamped logging for performance tracking

- Automatic early stopping (patience: 10 epochs)

- Session management (saves to

models/trainingsession<timestamp>/) - Best model saved to

models/best_lstm.pt - Sequence caching (dramatically speeds up subsequent runs)

[00:00 | +0.0s] Initializing Session: 20251231_143022

[00:01 | +1.2s] ✓ Loaded 1,234,567 price records

[00:02 | +0.9s] ✓ Loading cached sequences

[00:03 | +0.8s] ✓ Sequences ready: 45,678 total samples

[00:04 | +1.1s] ✓ Data Loaded: 36,542 train, 9,136 val

[00:05 | +1.2s] ✓ Model ready on device: mps

[00:05 | +0.1s] Starting training for 50 epochs...

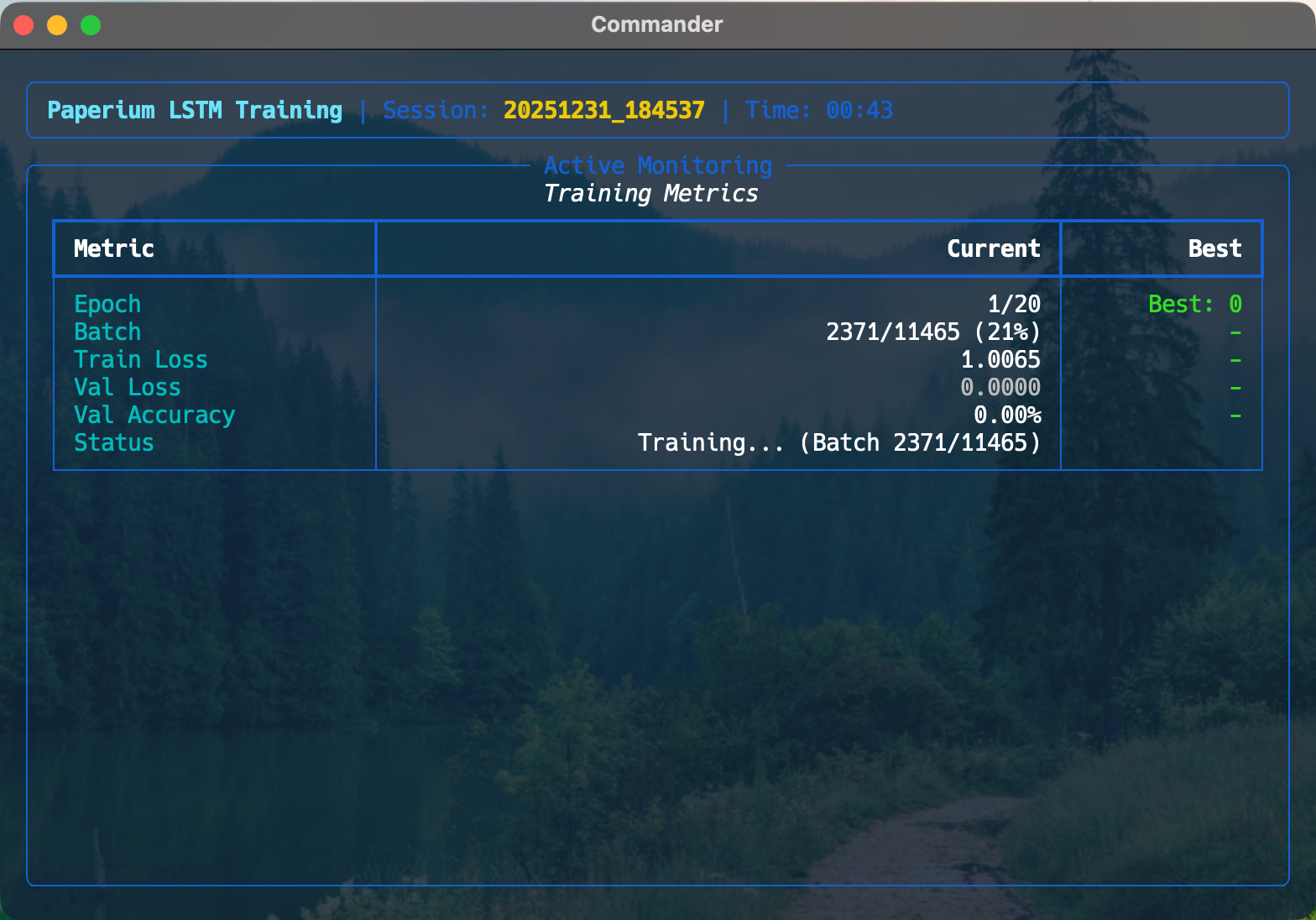

╭─ Paperium LSTM Training | Session: 20251231_143022 | Time: 02:15 ─╮ │ Training Metrics │ │ ┏━━━━━━━━━━━━━━┳━━━━━━━━━━━━━━━━━┳━━━━━━━━━━━━━━━━┓ │ │ ┃ Metric ┃ Current ┃ Best ┃ │ │ ┃ Epoch ┃ 15/50 ┃ Best: 12┃ │ │ ┃ Batch ┃ 127/200 (63%)┃ - ┃ │ │ ┃ Train Loss ┃ 0.8234 ┃ - ┃ │ │ ┃ Val Loss ┃ 0.7891 ┃ 0.7654┃ │ │ ┃ Val Accuracy ┃ 68.23% ┃ - ┃ │ │ └──────────────┴─────────────────┴────────────────┘ │ ╰────────────────────────────────────────────────────────────────────╯

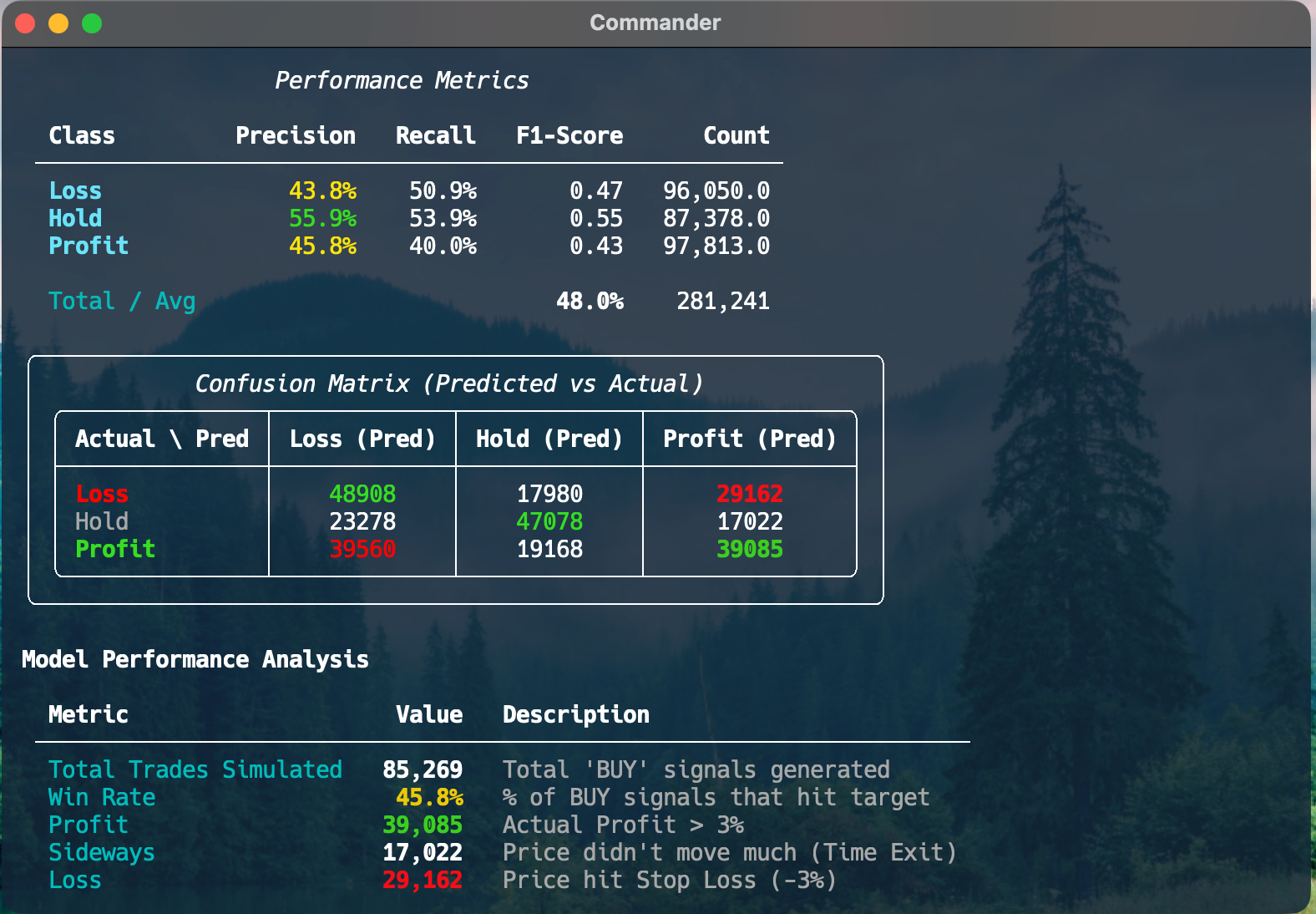

Evaluation & Backtesting

uv run python scripts/eval.py --start 2024-01-01 --end 2025-12-31What it does:

- Walk-forward testing on historical data

- Simulates real trading conditions

- Reports win rate, average return, Sharpe ratio

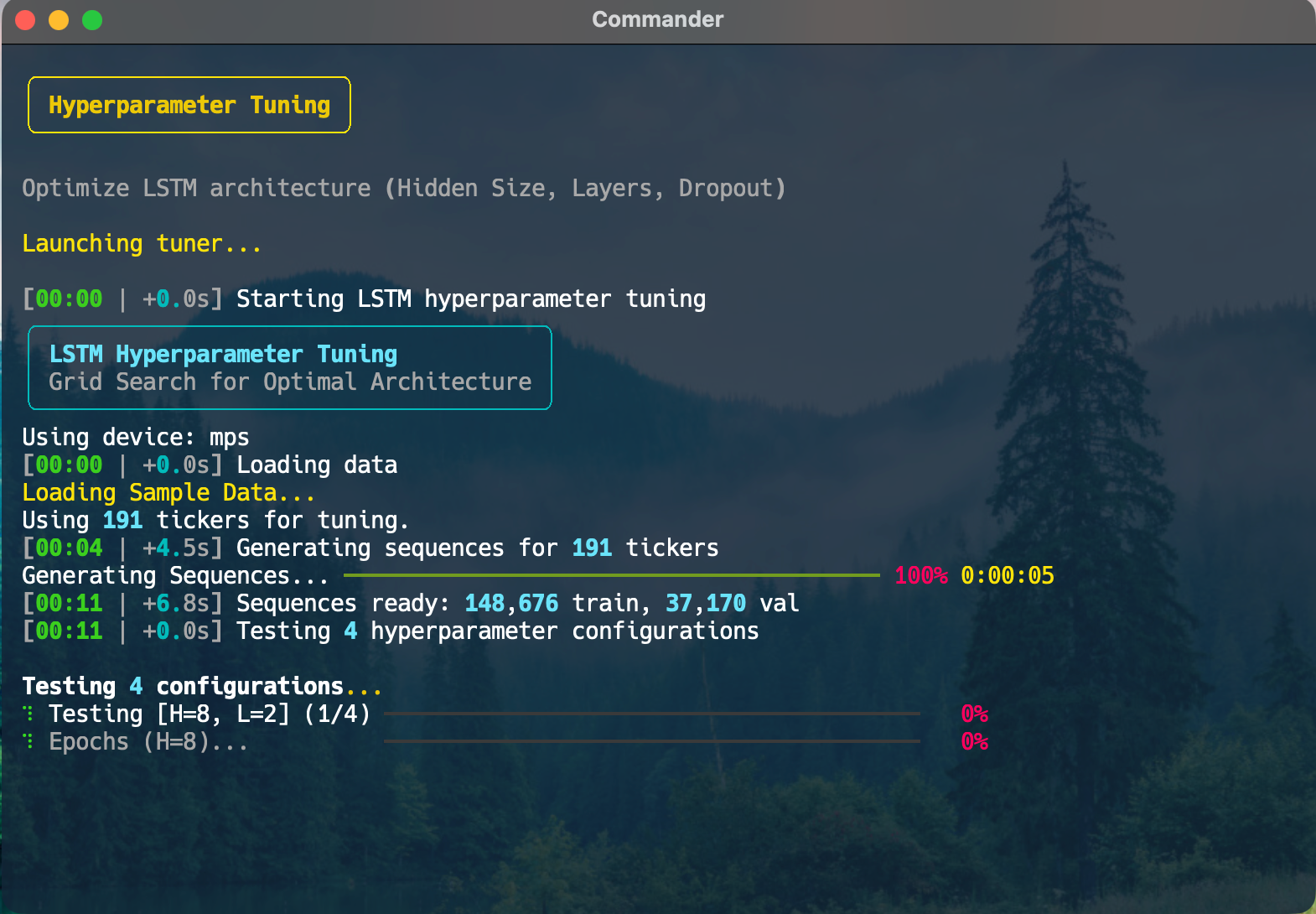

Hyperparameter Tuning

uv run python scripts/tune_lstm.py

Tests combinations of:

- Hidden sizes: [4, 8, 16, 32]

- Number of layers: [1, 2, 3]

- Dropout rates: [0.0, 0.1, 0.2]

Evening Update (Post-Market)

uv run python scripts/eod_retrain.pyWhat it does:

- Fetches latest EOD data

- Updates position statuses (SL/TP hits)

- Checks if retrain trigger is met

- Optionally retrains model with fresh data

Model Details

LSTM Architecture

Input Shape: (Batch, 100, 5)

- 100 days of lookback

- 5 features: Open, High, Low, Close, Volume (normalized)

Input (100, 5)

↓

LSTM Layer 1: hidden_size=8

↓

LSTM Layer 2: hidden_size=8

↓

Fully Connected Layer

↓

Softmax (3 classes)Output Classes:

- Class 0: LOSS - Hit lower barrier first (-3%)

- Class 1: NEUTRAL - Time expired (5 days)

- Class 2: PROFIT - Hit upper barrier first (+3%)

Why Small Hidden Size?

Financial data is extremely noisy. Large networks (32+ units) tend to overfit. Testing showed hidden_size=8 provides:

- Best generalization

- Fastest training

- Lowest validation loss

Data Pipeline

1. Ingestion

Source: Yahoo Finance API via yfinance

Fetching:

from data.fetcher import DataFetcher

fetcher = DataFetcher(stock_universe)

data = fetcher.fetch_batch(days=1825) # 5 yearsCaching:

- Hourly pickle cache in

.cache/folder - Cache key includes date + hour + ticker hash

- Speeds up repeated fetches from ~5 min to <1 sec

2. Storage

Database: SQLite (data/ihsg_trading.db)

Schema:

CREATE TABLE prices (

id INTEGER PRIMARY KEY,

date TEXT NOT NULL,

ticker TEXT NOT NULL,

open REAL,

high REAL,

low REAL,

close REAL,

volume INTEGER,

createdat TEXT DEFAULT CURRENTTIMESTAMP,

UNIQUE(date, ticker)

);Indexing:

idxpricesdateidxpricesticker

3. Normalization

Prices: Normalized relative to first day of 100-day window

normalizedprice = (pricet / price_0) - 1Volume: Log-normalized

normalized_volume = log(volume + 1)4. Sequence Generation

Rolling Window:

- Size: 100 days

- Stride: 1 (overlapping sequences)

- Creates multiple training samples per ticker

def getlabel(entryprice, future_prices, horizon=5, barrier=0.03):

upper = entry_price * (1 + barrier) # +3%

lower = entry_price * (1 - barrier) # -3%

for day in range(1, horizon + 1): if future_prices[day]['high'] >= upper: return 2 # PROFIT if future_prices[day]['low'] <= lower: return 0 # LOSS

return 1 # NEUTRAL (time expired)

5. Train/Validation Split

Method: Time-ordered (chronological)

- Training: First 80%

- Validation: Last 20%

Training Strategy

Optimizer & Loss

Optimizer: Adam

- Learning rate: 0.001

- No weight decay

loss = CrossEntropyLoss()(predictions, labels)Batch Size: 64

Early Stopping

Patience: 10 epochs

If validation loss doesn't improve for 10 consecutive epochs, training stops automatically.

Why?

- Prevents overfitting

- Saves compute time

- Best model is already saved

Device Selection

Auto-detects available hardware:

if torch.backends.mps.is_available():

device = "mps" # Apple Silicon

elif torch.cuda.is_available():

device = "cuda" # NVIDIA GPU

else:

device = "cpu"Checkpointing

Auto-save:

models/best_lstm.pt- Best validation lossmodels/trainingsession<timestamp>/best.pt- Session bestmodels/trainingsession<timestamp>/last.pt- Latest epoch

uv run python scripts/train.py --resume models/trainingsessionX/last.ptSignal Generation & Capital Allocation

Confidence-Weighted Allocation

When both --capital and --num-stock parameters are provided, the system allocates capital proportionally to signal confidence:

Formula:

# Calculate weights based on confidence

totalconfidence = sum(signal['conf'] for signal in topN_signals)

weighti = signali['conf'] / total_confidence

Allocate capital

allocationi = totalcapital × weight_i

sharesi = int(allocationi / price_i / 100) × 100 # Round to lotsExample:

If you have Rp 100M to allocate across 3 stocks:

- Stock A (confidence: 75%) → Gets ~43% of capital

- Stock B (confidence: 60%) → Gets ~34% of capital

- Stock C (confidence: 50%) → Gets ~23% of capital

Blacklist Filtering

Automatically excludes 72 illiquid/suspended stocks defined in data/blacklist.py:

from data.blacklist import BLACKLIST_UNIVERSE

if ticker in BLACKLIST_UNIVERSE: continue # Skip blacklisted stock

Blacklisted tickers include: Penny stocks, suspended trading, low liquidity, high manipulation risk.

Risk Parameters

Per Position (from TBL):

- Stop Loss: Entry price × 0.97 (-3%)

- Take Profit: Entry price × 1.03 (+3%)

- Max Hold Period: 5 days

- Confidence Threshold: >50% for Class 2 (PROFIT)

estimatedprofit = allocation × tblbarrier # +3%

estimatedloss = allocation × tblbarrier # -3%Configuration

config.py Structure

class DataConfig:

dbpath = "data/ihsgtrading.db"

window_size = 100 # Days of lookback

lookback_days = 1825 # Historical fetch (5 years)

stockuniverse = IDXUNIVERSE

class MLConfig: input_size = 5 # OHLCV features hidden_size = 8 # LSTM units num_layers = 2 # LSTM layers num_classes = 3 # LOSS/NEUTRAL/PROFIT dropout = 0.0 batch_size = 64 learning_rate = 0.001

# Triple Barrier tbl_horizon = 5 # Days tbl_barrier = 0.03 # 3% threshold

class PortfolioConfig: totalvalue = 100000_000 # IDR 100M max_positions = 10

Tuning Parameters

If win rate is low:

- Increase

tbl_barrier(e.g., 0.04 = 4%) - Increase

tbl_horizon(e.g., 7 days)

- Add

dropout(e.g., 0.1) - Decrease

hidden_size(e.g., 4)

- Increase

hidden_size(e.g., 16) - Add more layers

Performance Optimization

Sequence Caching

Problem: Processing 957 tickers takes 30-60 seconds every training run.

Solution: Cache computed sequences to disk.

Cache Key:

cachekey = f"sequences{dbdate}{rowcount}{config_hash}.pkl"Performance:

- First run: ~45 seconds (cache miss)

- Subsequent runs: ~1 second (cache hit)

- New data added to database

- Configuration changes (window size, TBL params)

Data Fetching

Yahoo Finance caching:

- Hourly granularity

- Stored in

.cache/folder - Reduces API calls from minutes to sub-second

Training Optimizations

Progress tracking:

- Batch-level updates (every 10 batches for training, 5 for validation)

- Prevents UI freezing

- Shows ETA for completion

[00:00 | +0.0s] Initializing Session

[00:01 | +1.2s] ✓ Data Loaded

[00:45 | +44.1s] ✓ Sequences readyShows both total elapsed time and step duration.

Known Issues & Future Work

Current Limitations

- Class Imbalance

- Inference Speed

- Static Parameters

optimize_tbl.py for dynamic optimization

Planned Enhancements

- Multi-timeframe analysis - Add intraday data

- Ensemble methods - Combine multiple models

- Reinforcement learning - Adaptive position sizing

- Volatility regime detection - Adjust barriers by market conditions

- Transaction cost modeling - Include brokerage fees

Performance Notes

Optimal Hyperparameters

Window Size: 100 days

- Too short: Misses long-term patterns

- Too long: Overfits to noise

- Small networks prevent overfitting on noisy financial data

- Faster training and inference

- Tested multiple combinations

- Best balance of frequency and win rate for IHSG

Training Time

Dataset: ~45,000 sequences from 887 tickers

Hardware:

- Apple M1 (MPS): ~3 minutes per epoch

- NVIDIA RTX 3080: ~1 minute per epoch

- CPU only: ~10 minutes per epoch

Contributing

This is a research project. Contributions welcome for:

- Additional technical indicators

- Alternative labeling schemes

- Performance optimizations

- Documentation improvements

Disclaimer

This is a research project for educational purposes.

- Trading involves substantial risk of loss

- Past performance does not guarantee future results

- Always perform your own due diligence

- Never trade with money you cannot afford to lose

- The authors assume no liability for trading losses

License

MIT License