Technical analysis in R: indicators, candlestick pattern detection, and interactive trading charts.

{talib}: Fast TA-Lib indicators and candlestick patterns for R

![]()

![]()

![]()

{talib} provides fast R bindings to the TA-Lib C library for OHLCV data: technical indicators, candlestick pattern recognition, rolling-window utilities, and composable financial charts. It is designed for researchers, analysts, and quant developers who need technical-analysis features in R without building a heavy dependency stack. Core computations are executed in C through .Call(), while charting support is available through optional {plotly} and {ggplot2} integrations.[^1]

The API covers 150+ TA-Lib-backed functions across momentum, overlap, volatility, volume, cycle, price-transform, rolling-statistics, and candlestick-pattern families, including 61 candlestick pattern detectors.

Why {talib}?

| Need | {talib} | |:---------------------|:----------------------------------------------------------------------------------------| | Technical indicators | TA-Lib-backed moving averages, momentum, volatility, volume, cycle, and overlap studies | | Candlestick patterns | Built-in Japanese candlestick pattern recognition | | OHLCV workflows | Works directly with open, high, low, close, and volume columns | | Performance | Computation delegated to C routines through .Call() | | Dependencies | Minimal required R dependencies; plotting packages are optional | | Charts | Composable financial charts with optional {plotly} and {ggplot2} support |

Installation[^2]

Install the release version from CRAN:

r

install.packages("talib")Install the development version from GitHub:

r

pak::pak("serkor1/ta-lib-R")Quick start

All functions provide S3 methods for <data.frame>, <matrix>, and—where applicable—<vector> inputs. The general convention is simple: the output uses the same container type as the input.

r

calculate the

relative strength index

relativestrengthindex <- talib::RSI(

talib::BTC

)

display results

tail(

relativestrengthindex

)

#> RSI

#> 2024-12-26 01:00:00 46.48851

#> 2024-12-27 01:00:00 43.85488

#> 2024-12-28 01:00:00 45.93888

#> 2024-12-29 01:00:00 43.12301

#> 2024-12-30 01:00:00 41.47686

#> 2024-12-31 01:00:00 43.37358Indicator outputs preserve input length, which keeps results aligned with the original OHLCV rows.

r

combine multiple

indicators

features <- cbind(

talib::relativestrengthindex(talib::BTC),

talib::bollinger_bands(talib::BTC),

talib::engulfing(talib::BTC)

)

tail(features) #> RSI UpperBand MiddleBand LowerBand CDLENGULFING #> 2024-12-26 01:00:00 46.48851 100487.38 96698.61 92909.83 -1 #> 2024-12-27 01:00:00 43.85488 100670.65 96512.96 92355.27 0 #> 2024-12-28 01:00:00 45.93888 100632.13 96581.91 92531.69 0 #> 2024-12-29 01:00:00 43.12301 99628.77 95576.60 91524.43 -1 #> 2024-12-30 01:00:00 41.47686 96403.53 94231.31 92059.09 0 #> 2024-12-31 01:00:00 43.37358 95441.13 93774.23 92107.34 0

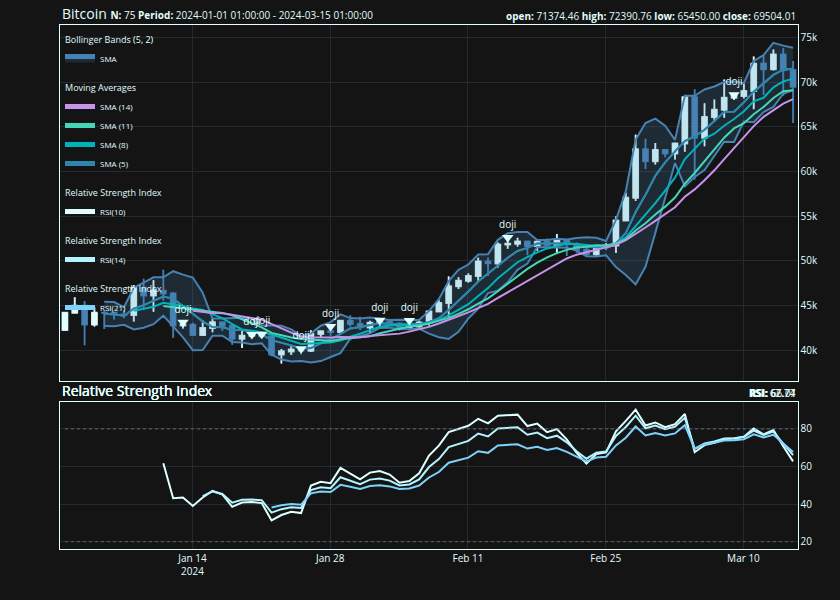

Charting

{talib} comes with a composable charting API built on two core functions: indicator() and chart()—both functions are built on model.frame for maximum flexibility:

r

subset data and

store as 'BTC'

BTC <- talib::BTC[1:75, ]

construct chart in a brace block

alternatively use |>

{

## initialize main chart

talib::chart(

x = BTC,

title = "Bitcoin"

)

## add Bollinger Bands to ## the existing chart talib::indicator( talib::BBANDS )

## add Simple Moving Averages (SMA) ## to the chart in a loop for (n in seq(5, 15, by = 3)) { talib::indicator( talib::SMA, n = n ) }

## similar subchart indicators ## like the Relative Strength Index ## can be grouped to avoid repeated ## subpanels talib::indicator( talib::RSI(n = 10), talib::RSI(n = 14), talib::RSI(n = 21) )

## identify Doji patterns ## and add them to the chart talib::indicator( talib::doji ) }

Implementation: {talib} vs upstream (TA-Lib Core)

Functions use descriptive snake_case names, but every function is aliased to its TA-Lib shorthand for compatibility with the broader ecosystem:

| Category | TA-Lib (C) | {talib} | {talib} alias | |:----------------------|:---------------------|:----------------------------|:------------------| | Overlap Studies | TABBANDS() | bollingerbands() | BBANDS() | | Momentum Indicators | TACCI() | commoditychannel_index() | CCI() | | Volume Indicators | TAOBV() | onbalance_volume() | OBV() | | Volatility Indicators | TAATR() | averagetrue_range() | ATR() | | Price Transform | TAAVGPRICE() | averageprice() | AVGPRICE() | | Cycle Indicators | TAHTSINE() | sinewave() | HTSINE() | | Pattern Recognition | TACDLHANGINGMAN() | hangingman() | CDLHANGINGMAN() |

Interface: R vs Python

The main difference between the R and Python interfaces is how OHLCV series are passed into each indicator function. Below is an example of identifying Doji patterns in R and Python.

In Python, each series is passed independently:

python

import numpy as np

import talib

o = np.array([1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1], dtype=float) h = np.array([2, 2, 2, 2, 2, 2, 2, 2, 2, 2, 2], dtype=float) l = np.array([1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1], dtype=float) c = np.array([2, 2, 2, 2, 2, 2, 2, 2, 2, 2, 1], dtype=float)

print( talib.CDLDOJI(o, h, l, c) )

In R the series are passed as a tabular container:

r

ohlc <- data.frame(

open = c(1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1),

high = c(2, 2, 2, 2, 2, 2, 2, 2, 2, 2, 2),

low = c(1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1),

close = c(2, 2, 2, 2, 2, 2, 2, 2, 2, 2, 1)

)

talib::CDLDOJI( ohlc )

All default series arguments are handled internally, and the R interface is therefore higher-level: users pass one OHLC container rather than manually splitting the series.

Contributing and cloning

Contributions are welcome. For non-trivial changes, please open an issue first to discuss the proposed design, API impact, and testing approach.

This repository vendors TA-Lib as a Git submodule. Clone the repository with submodules enabled:

sh

git clone --recurse-submodules https://github.com/serkor1/ta-lib-R.git

cd ta-lib-RIf you already cloned the repository without submodules, initialize them with:

sh

git submodule update --init --recursiveMost indicator wrappers, helper functions, documentation fragments, and unit tests are generated from the scripts in codegen/. The charting interface is maintained separately.

Common development tasks are exposed through Make targets:

sh

make helpSee CONTRIBUTING.md for the full development workflow.

Code of Conduct

Please note that {talib} is released with a Contributor Code of Conduct. By contributing to this project, you agree to abide by its terms.

[^1]: See benchmark/ for detailed benchmarks against [{TTR}]() and general performance across multiple indicators.

[^2]: {talib} is a compiled package. CRAN binaries are available for standard platforms when provided by CRAN. Source installation requires a working compiler toolchain and CMake.