High-performance limit order book engine with C++ core and Python SDK. Processes 20M+ msgs/sec with µs latency. Supports real crypto/equity data replay, spread/imbalance/impact analytics, and backtesting of VWAP, TWAP, POV, and market-making strategies with reproducible PnL and risk metrics.

Limit Order Book (LOB) Engine — C++20

![]()

![]()

![]()

![]()

![]()

A high-performance C++ matching engine that processes buy/sell orders with exchange-style semantics. Demonstrates low-latency hot-path design, cache-friendly data structures, reproducible benchmarking, and clean build/test tooling.

🧰 Tech Stack

🔤 Languages & Compilers

✅ Testing & CI/CD

⚡ Performance & Profiling

📂 Data & Processing

🐳 Containers & Release

📊 Visualization & Reporting

🖥️ Systems & Infra

⚡ Throughput: 20.7M msgs/sec 📊 Latency: p50=0.04µs, p99≈1µs ✅ Verified on real BTCUSDT BinanceUS data

🔎 Quick Highlights

- Core engine (

BookCore): limit & market orders, cancels, modifies, FIFO per price level. - Order flags:

IOC,FOK,POST_ONLY,STP(self-trade prevention). - Persistence: binary snapshots (write/load) + replay tool.

- Performance: slab memory pool, side-specialized matching (branch elimination), cache-hot best-level pointers,

-fno-exceptions -fno-rtti. - Tooling: benchmark tool (percentiles + histogram CSVs), Catch2 unit tests, profiling toggle (

-fno-omit-frame-pointer -g).

🧭 Architecture

Engine flow

+-------------------+ +----------------+ | Incoming Orders | -----> | BookCore | +-------------------+ | (match/rest) | +--------+-------+ | v +--------------------+ +-------------------+ | PriceLevels (B/A) |<-------->| LevelFIFO(s) | | best_bid/ask + | | intrusive queues | | bestlevelptr | +-------------------+ +-------------------+ | v +-------------------+ | Logger / Snapshot | | (events, trades) | +-------------------+Data layout

Bids ladder (higher is better) Asks ladder (lower is better) bestbid --> [px=100][FIFO] -> ... bestask --> [px=101][FIFO] -> ...

LevelFIFO (intrusive): head <-> node <-> node <-> ... <-> tail (FIFO fairness, O(1) ops)

Memory pool (slab allocator)

+------------------------- 1 MiB slab -------------------------+ | [OrderNode][OrderNode][OrderNode] ... [OrderNode] | +--------------------------------------------------------------+ ^ free list (O(1) alloc/free)🗂️ Repository Layout

cpp/

include/lob/

book_core.hpp # engine API & hot-path helpers

price_levels.hpp # ladders: contiguous & sparse implementations

types.hpp # Tick, Quantity, IDs, flags, enums

logging.hpp # snapshot writer/loader, event logger interface

mempool.hpp # slab allocator for OrderNode

src/

book_core.cpp # engine implementation (side-specialized matching)

price_levels.cpp # TU for headers (keeps targets happy)

logging.cpp # snapshot I/O + logger implementation

util.cpp # placeholder TU for lob_util

tools/

bench.cpp # synthetic benchmark -> CSV + histogram

replay.cpp # snapshot replay tool

CMakeLists.txt # inner build (library + tools + tests)

docs/

bench.md # benchmark method + sample results

bench.csv # percentiles output (generated by bench_tool)

hist.csv # latency histogram 0–100µs (generated)

python/

olob/bindings.cpp # pybind11 module (target: lobcpp -> _lob)

CMakeLists.txt # outer build (FetchContent Catch2; drives inner)🛠️ Build & Run

Configure & build (Release)

rm -rf build cmake -S . -B build -DCMAKEBUILDTYPE=Release \ -DLOBBUILDTESTS=ON -DLOB_PROFILING=ON cmake --build build -jCMake options

LOBBUILDTESTS(ON/OFF): build Catch2 tests.LOB_PROFILING(ON/OFF): add-fno-omit-frame-pointer -gfor clean profiler stacks.LOBENABLEASAN(Debug only): AddressSanitizer for tests/tools.LOB_LTO(Release only): optional-flto.

ctest --test-dir build --output-on-failureBenchmark (CSV + histogram)

./build/cpp/bench_tool --msgs 2000000 --warmup 50000 \ --out-csv docs/bench.csv --hist docs/hist.csvmsgs=2000000, time=0.156s, rate=12854458.3 msgs/s latency_us: p50=0.04 p90=0.08 p99=0.08 p99.9=0.12docs/bench.md, docs/bench.csv, and docs/hist.csv for reproducible results.

Replay from snapshot

./build/cpp/replay_tool <snapshot.bin>📚 Engine API (Essentials)

Types (include/lob/types.hpp)

Side { Bid, Ask },Tick(price),Quantity,OrderId,UserId,Timestamp,SeqNo.- Flags:

IOC,FOK,POST_ONLY,STP.

NewOrder { seq, ts, id, user, side, price, qty, flags }.ModifyOrder { seq, ts, id, newprice, newqty, flags }.ExecResult { filled, remaining }.

include/lob/book_core.hpp) ExecResult submit_limit(const NewOrder&).ExecResult submit_market(const NewOrder&).bool cancel(OrderId id).ExecResult modify(const ModifyOrder&).

include/lob/price_levels.hpp) PriceLevelsContig(PriceBand)— contiguous array for bounded tick ranges.PriceLevelsSparse—unordered_map<Tick, LevelFIFO>for unbounded ranges.- Both expose

bestbid()/bestask()and cache-hotbestlevelptr(Side).

include/lob/logging.hpp, src/logging.cpp) SnapshotWriter::write_snapshot(...).loadsnapshotfile(...).IEventLogger+JsonlBinLogger(jsonl + binary events/trades; optional snapshots).

⚙️ Design & Performance Choices

- Slab allocator (arena)

- Branch elimination

if (side).

- Cache-hot top-of-book

- Lean binary

-fno-exceptions -fno-rtti -O3 -march=native.

- Deterministic FIFO

- Reproducibility

🧪 Minimal Integration (C++)

using namespace lob;

PriceLevelsSparse bids, asks;

BookCore book(bids, asks, /logger/nullptr);

NewOrder o{1, 0, 42, 7, Side::Bid, 1000, 10, 0}; auto r1 = book.submit_limit(o); // may trade or rest at 1000 auto ok = book.cancel(42); // cancel by ID

🔬 Profiling

Linux (perf)

perf stat -d ./build/cpp/bench_tool --msgs 2000000 perf record -g -- ./build/cpp/bench_tool --msgs 2000000 perf reportmacOS (Instruments) Use Time Profiler with frame pointers (-DLOB_PROFILING=ON).

🌐 Crypto Data Connector

A Python CLI ships alongside the C++ engine to capture and normalize live exchange data.

Capture raw Binance US data

lob crypto-capture --exchange binanceus --symbol BTCUSDT \ --minutes 2 --raw-dir raw --snapshot-every-sec 60- Connects to Binance US WebSocket streams (

diffDepth,trade). - Pulls a REST snapshot every N seconds (

--snapshot-every-sec). - Persists gzipped JSONL to:

raw/YYYY-MM-DD/<exchange>/<symbol>/…Normalize into Parquet

lob normalize --exchange binanceus --date $(date -u +%F) \ --symbol BTCUSDT --raw-dir raw --out-dir parquetparquet/YYYY-MM-DD/binanceus/BTCUSDT/events.parquetSchema

ts→ event timestamp (ns, UTC)side→"B"(bid) or"A"(ask)price→ price levelqty→ size traded or restingtype→"book"(order book update) or"trade"

import pandas as pd df = pd.read_parquet("parquet/2025-08-24/binanceus/BTCUSDT/events.parquet") print(df.head()) print(df.dtypes) print(len(df))✅ Real Capture Example (BTCUSDT, Binance US)

I ran a full 1-hour capture of BTCUSDT from Binance US and normalized it:

lob crypto-capture --exchange binanceus --symbol BTCUSDT \

--minutes 60 --raw-dir raw --snapshot-every-sec 60 && \

lob normalize --exchange binanceus --date $(date -u +%F) \

--symbol BTCUSDT --raw-dir raw --out-dir parquetThis produced a normalized Parquet dataset at:

parquet/YYYY-MM-DD/binanceus/BTCUSDT/events.parquetFirst rows (pandas)

import pandas as pd df = pd.read_parquet("parquet/2025-08-24/binanceus/BTCUSDT/events.parquet") print(df.head()) print(df.dtypes) print("Total rows:", len(df))Sample output:

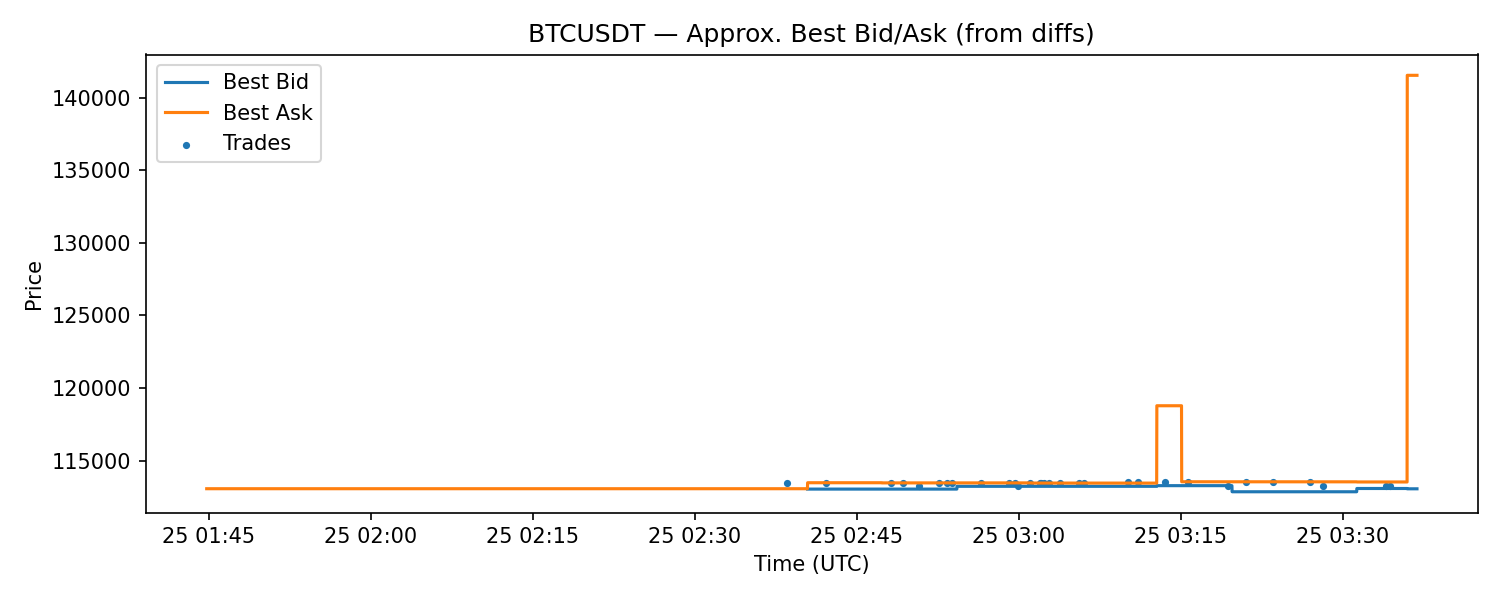

ts side price qty type 0 2025-08-24 10:00:00.123 B 63821.45 0.002 book 1 2025-08-24 10:00:00.456 A 63822.10 0.004 book 2 2025-08-24 10:00:00.789 B 63820.50 0.010 trade ... Total rows: 3,512,947Quick visualization (best bid/ask over time) I generated a simple chart from the Parquet file:

python docs/makedepthchart.py \ --parquet parquet/2025-08-24/binanceus/BTCUSDT/events.parquet \ --out docs/depth_chart.png

Note: This chart approximates best bid/ask by forward-filling incremental book updates. It demonstrates that live capture & normalization worked end-to-end.

📖 Order Book Reconstruction & Validation

What it does

- Starts from a full exchange REST snapshot.

- Applies WebSocket depth updates (diffs) in strict sequence to rebuild the live Level-2 book.

- Periodically resyncs from later snapshots when gaps are detected.

- Computes a top-N checksum and records best bid/ask per step.

Why it matters

- Produces a deterministic, gap-aware view of the L2 book.

- Handles out-of-order updates, drops, and partial feeds.

- Enables objective quality checks via tick-level drift vs. the exchange’s own snapshot.

🔧 Usage

Capture (example, Binance US)

lob crypto-capture --exchange binanceus --symbol BTCUSDT \ --minutes 35 --raw-dir raw --snapshot-every-sec 60Reconstruct

python -m orderbook_tools.reconstruct \ --raw-dir raw --date YYYY-MM-DD --exchange binanceus --symbol BTCUSDT \ --out-dir recon --tick-size 0.01 \ --snap-glob "depth/snapshot-.json.gz" \ --diff-glob "depth/diffs-.jsonl.gz"Validate (30-minute check)

python -m orderbook_tools.validate \ --raw-dir raw --recon-dir recon \ --date YYYY-MM-DD --exchange binanceus --symbol BTCUSDT \ --tick-size 0.01 --window-min 30 \ --snap-glob "depth/snapshot-.json.gz"▶️ Replay Engine (Real-Time & N× Accelerated)

What it does

- Replays normalized market events into the C++

BookCore, preserving inter‑arrival gaps with a speed control (e.g.,1x,10x,50x). - Samples TAQ‑like quotes on a fixed time grid (e.g., every 50 ms): best bid/ask, mid, spread, microprice.

- Records trades as event‑driven prints.

- Writes outputs to CSV (and optionally Parquet via a tiny Python helper).

- Produces deterministic, monotonic time series for research & backtests.

- Enables fast‑forward processing for large captures.

- Exercises the actual C++ book under realistic feeds.

# Convert your normalized Parquet to CSV with required columns python - <<'EOF' import pandas as pd df = pd.read_parquet("parquet/YYYY-MM-DD/<exchange>/<symbol>/events.parquet") if 'ts_ns' not in df.columns: df['tsns'] = pd.todatetime(df['ts'], utc=True).view('int64') df['type'] = df['type'].astype(str).str.lower() df['side'] = df['side'].astype(str).str.lower().map({'b':'B','bid':'B','buy':'B','a':'A','ask':'A','sell':'A','s':'A'}).fillna('A') df[['tsns','type','side','price','qty']].tocsv("parquet_export.csv", index=False) EOF

Replay at 50×, sampling quotes every 50 ms

./build/cpp/replay_tool \

--file parquet_export.csv \

--speed 50x \

--cadence-ms 50 \

--quotes-out taq_quotes.csv \

--trades-out taq_trades.csv

Optional: convert TAQ CSVs to Parquet

python python/csvtoparquet.py --in taqquotes.csv --out taqquotes.parquet

python python/csvtoparquet.py --in taqtrades.csv --out taqtrades.parquet📊 Market Analytics

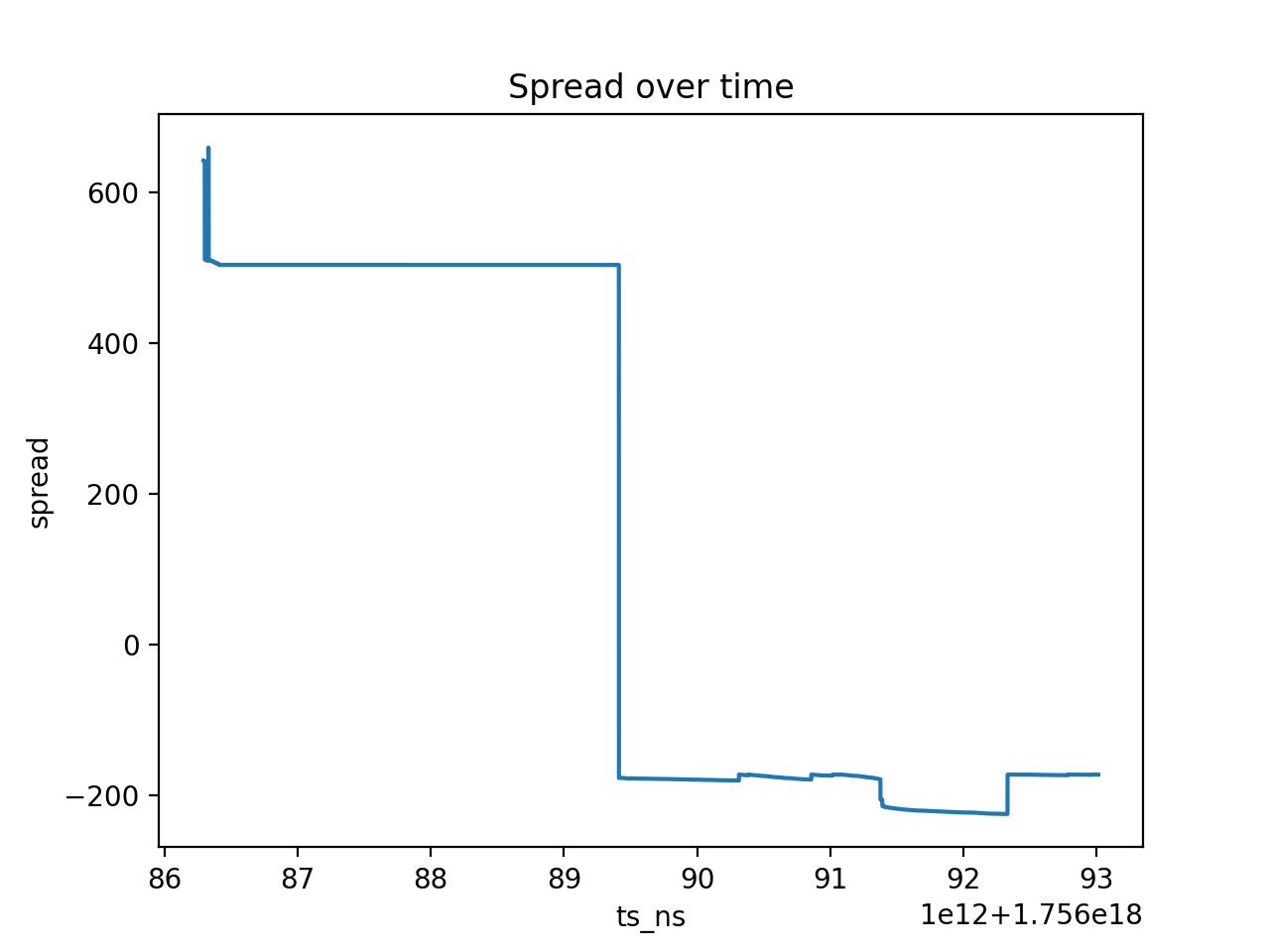

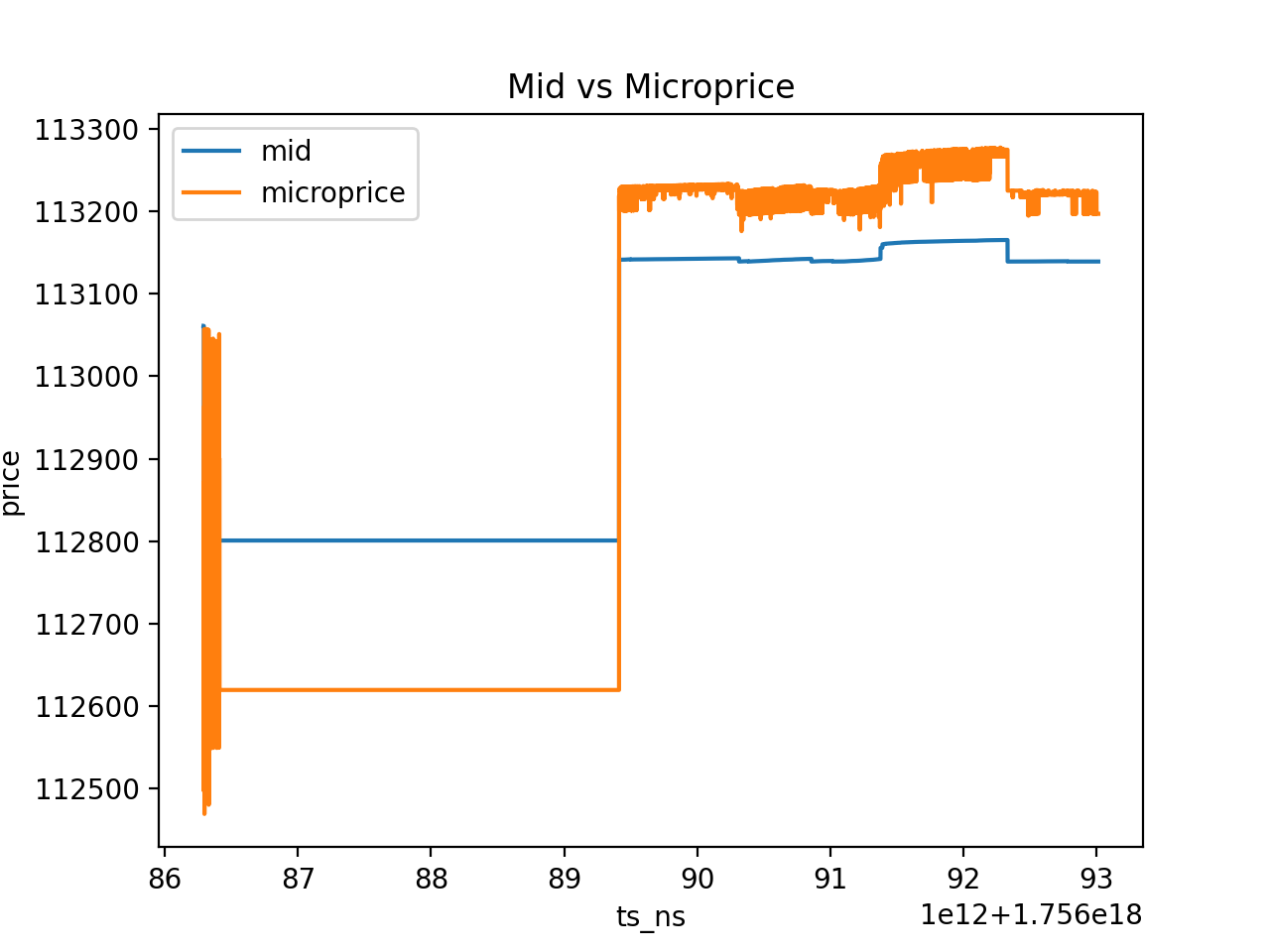

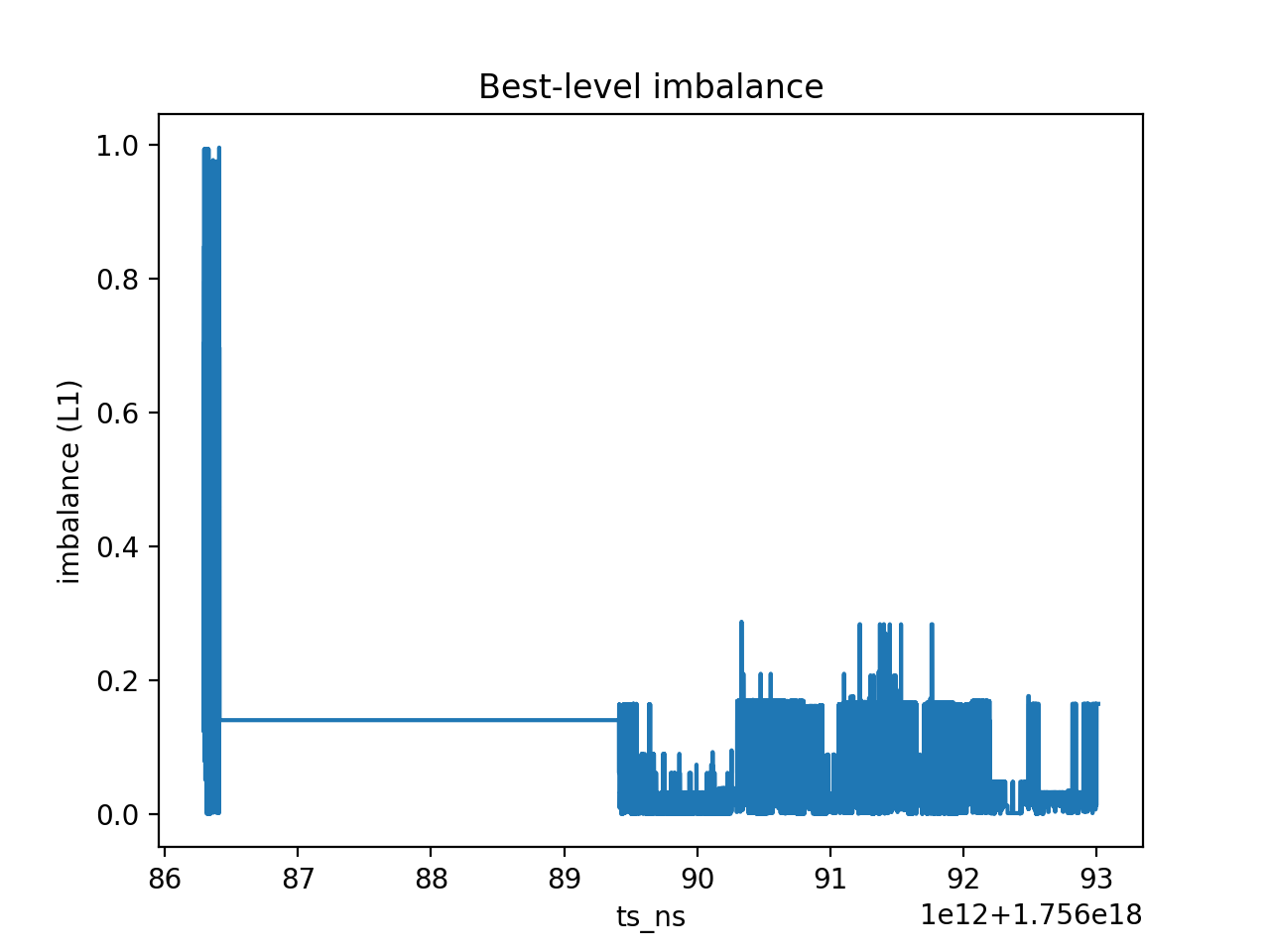

This module computes microstructure metrics from replayed TAQ quotes and reconstructed depth:

- Spread: ask − bid

- Microprice: imbalance-aware mid = (bidpx·asksz + askpx·bidsz) / (bidsz + asksz)

- Imbalance: bid volume ÷ (bid volume + ask volume)

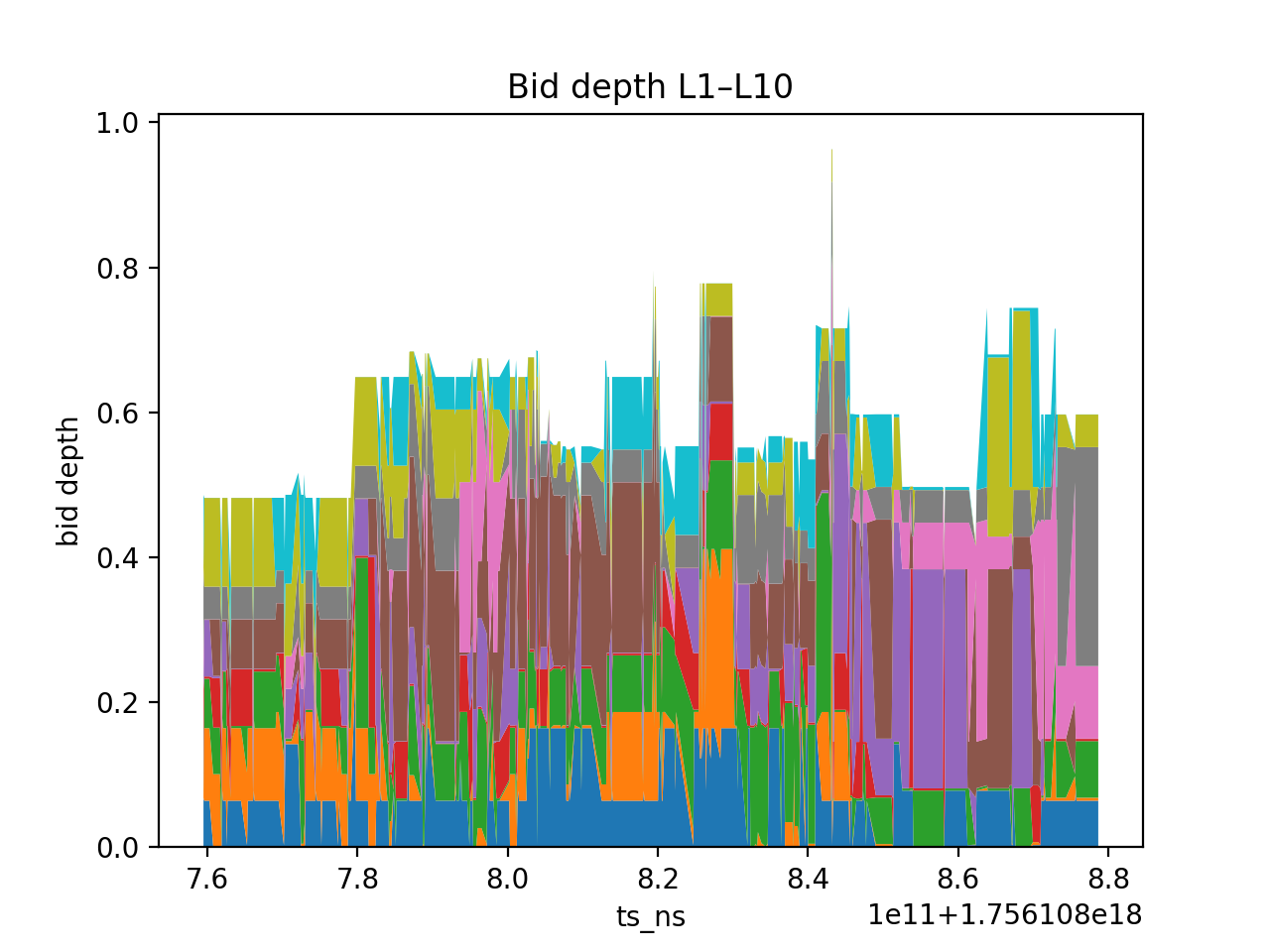

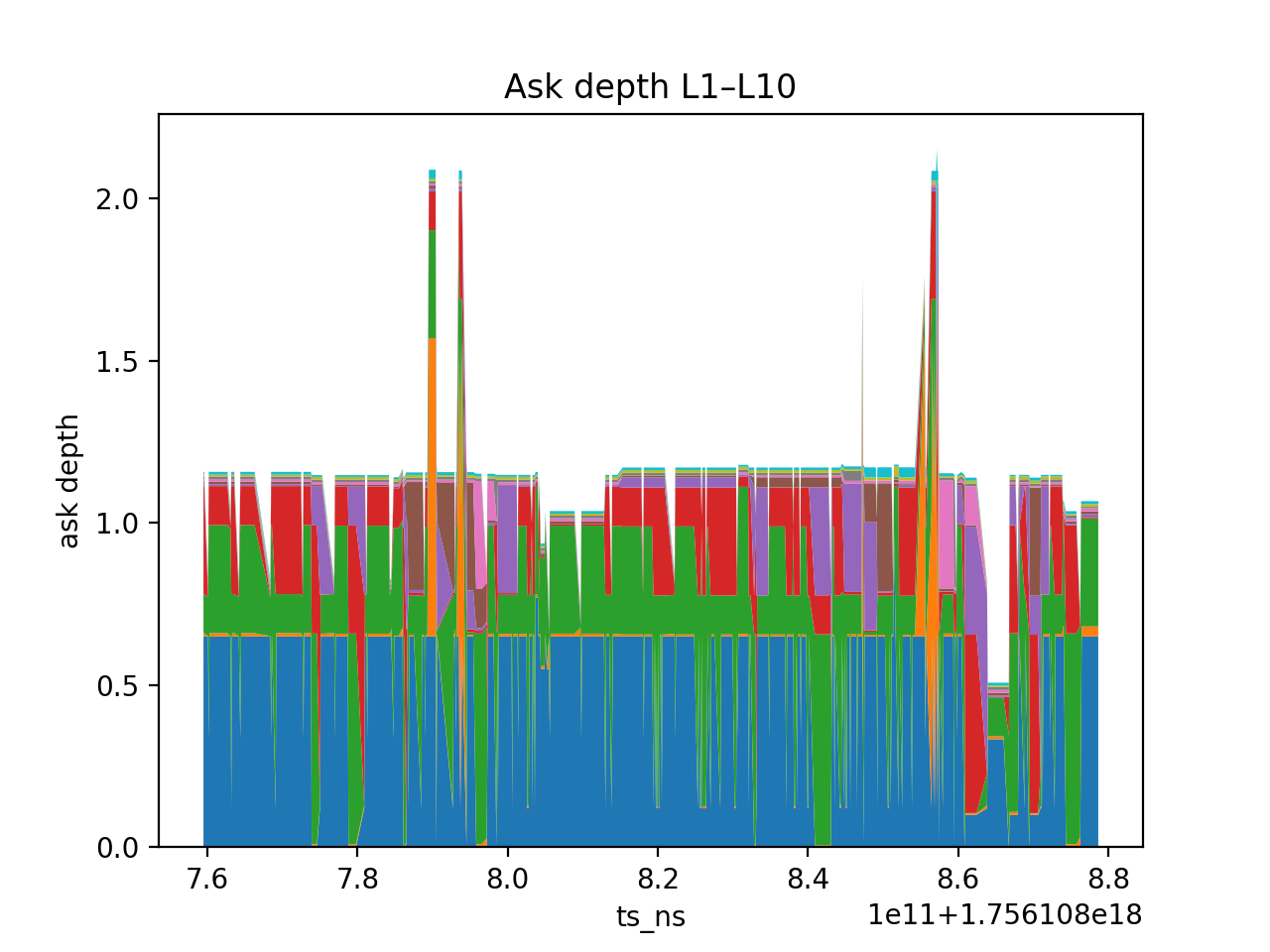

- Depth (L1–L10): cumulative quantities at the top 10 bid/ask levels

Usage

python -m olob.metrics \

--quotes taq_quotes.csv \

--depth-top10 recon/2025-08-25/binanceus/BTCUSDT/top10_depth.parquet \

--out-json analytics/summary.json \

--plots-out analytics/plotsanalytics/summary.json: time-weighted averages and percentiles.analytics/plots/: saved PNG charts (examples below).

📈 Example Outputs

Spread over time

Mid vs Microprice

Best-level imbalance (L1)

Top-10 Bid Depth

Top-10 Ask Depth

📊 Microstructure Analytics (volatility, impact, flow, imbalance, clustering)

This repository includes a Python module that computes microstructure metrics from TAQ-style quotes/trades (and optional depth), and produces reproducible figures + a JSON summary.

🔍 What it computes

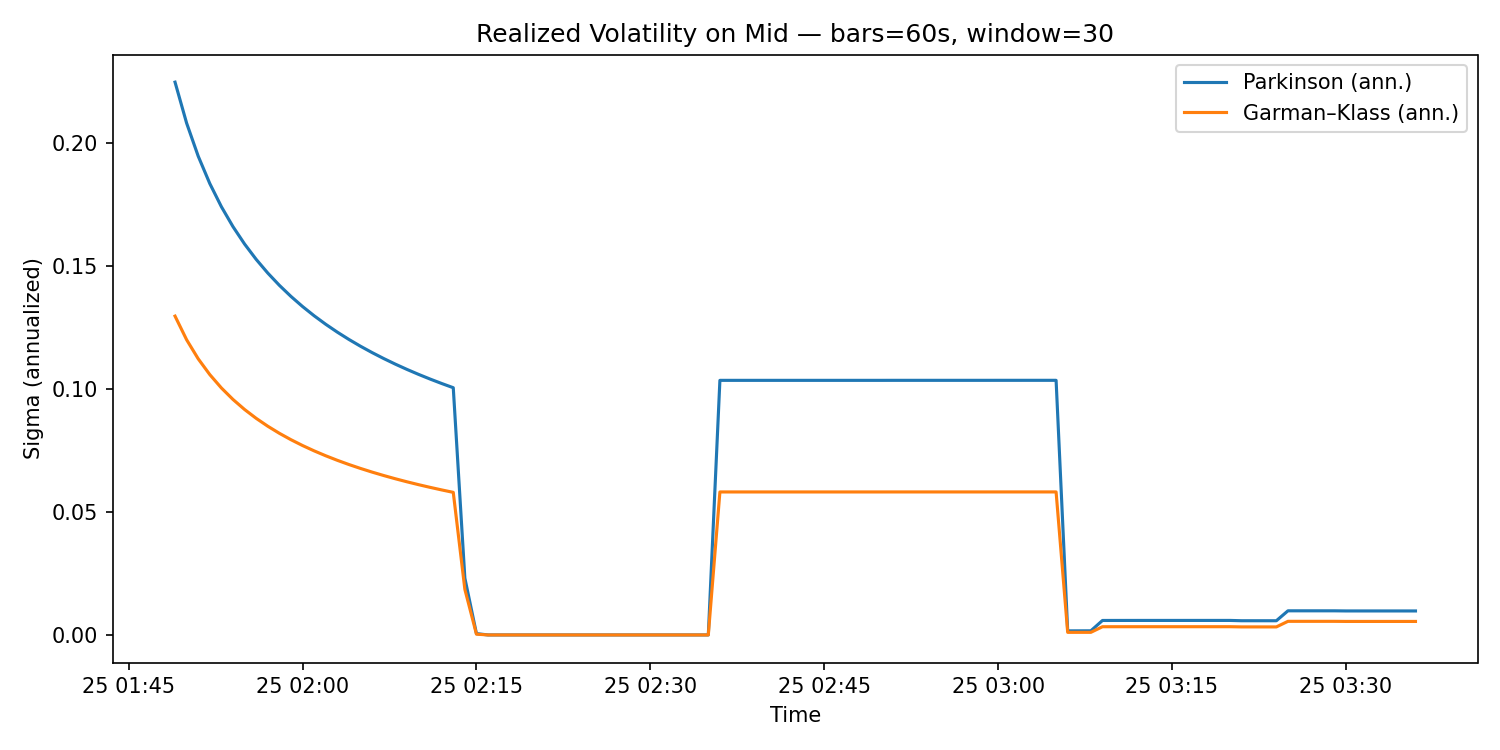

- Realized volatility (Parkinson & Garman–Klass) on mid-price (best bid/ask).

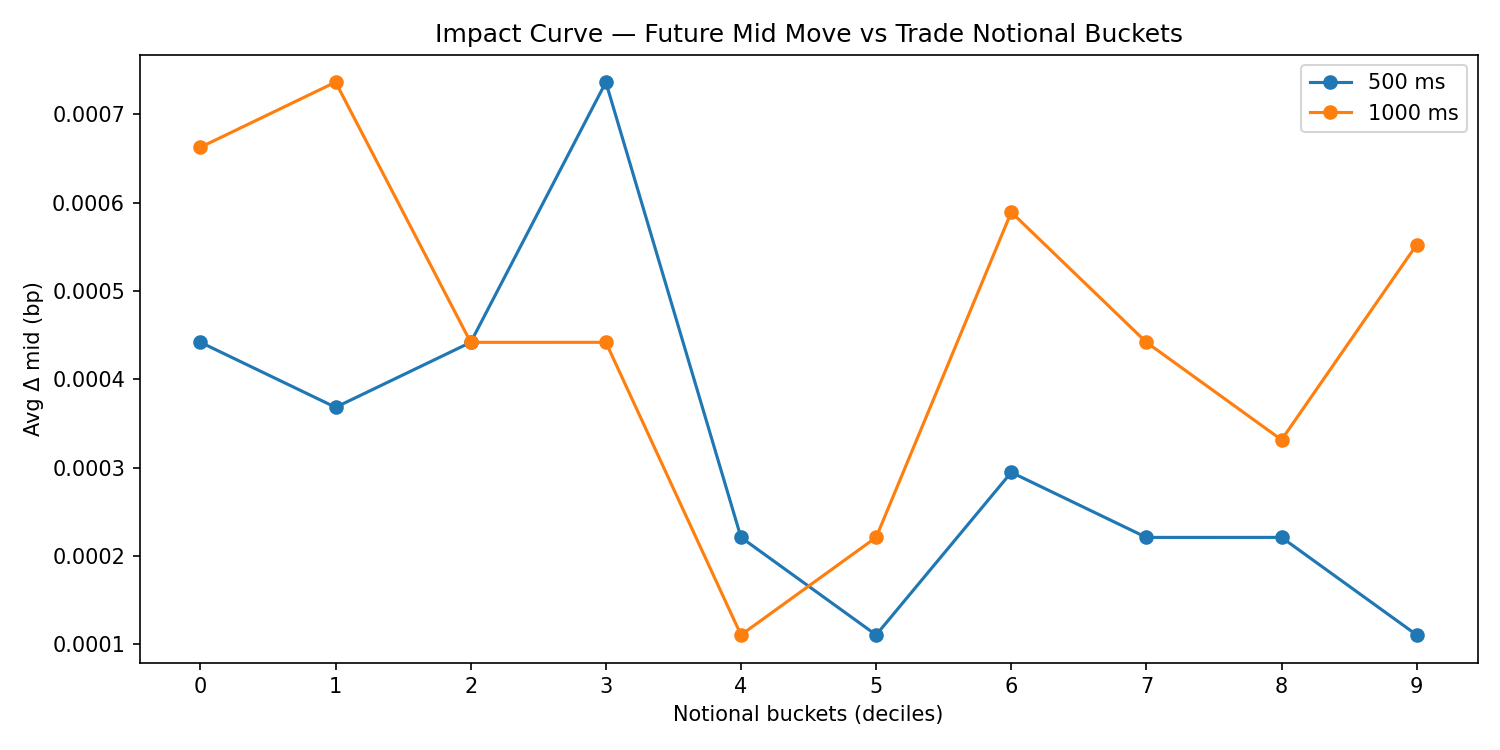

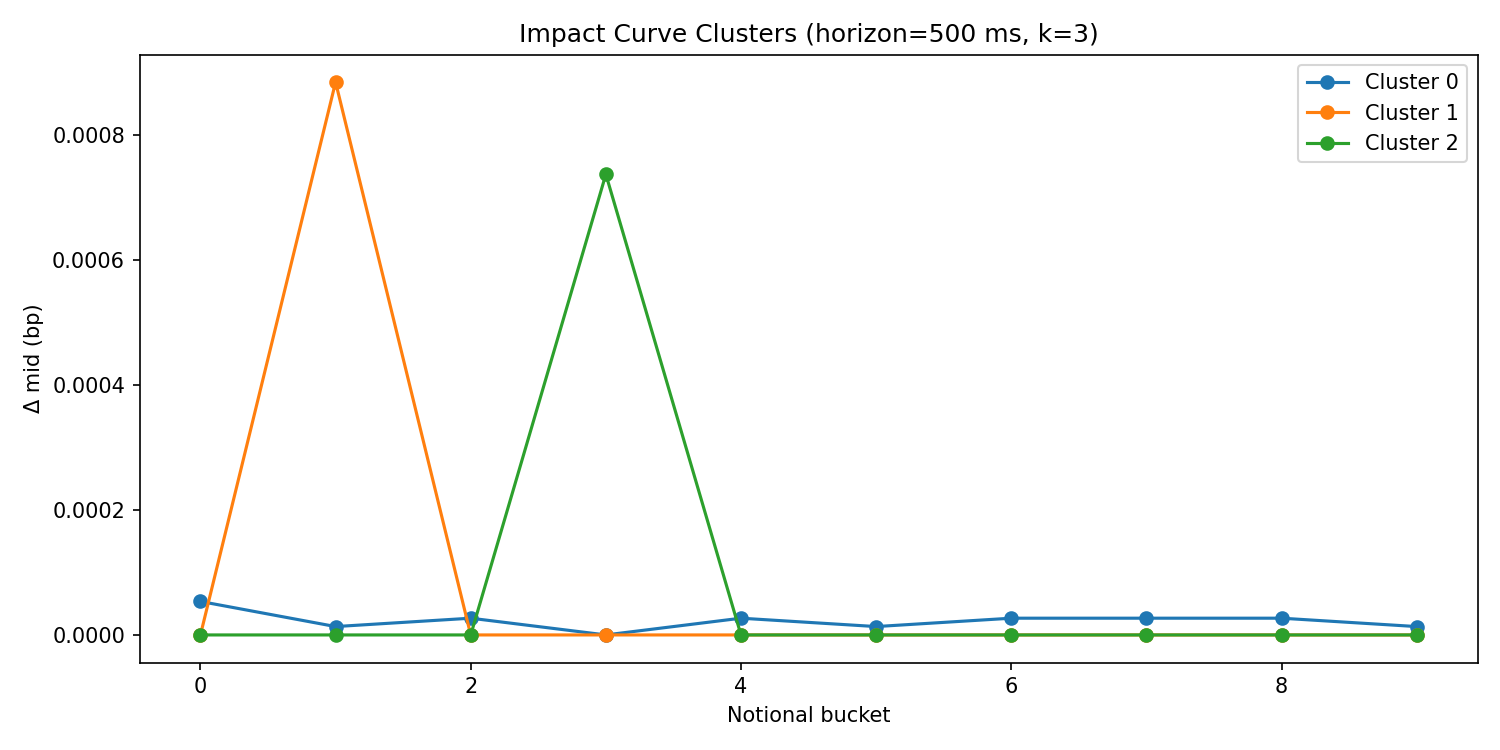

- Impact curves: average future mid move (bp) vs trade size buckets (notional deciles & size percentiles), across horizons (e.g., 0.5s, 1s).

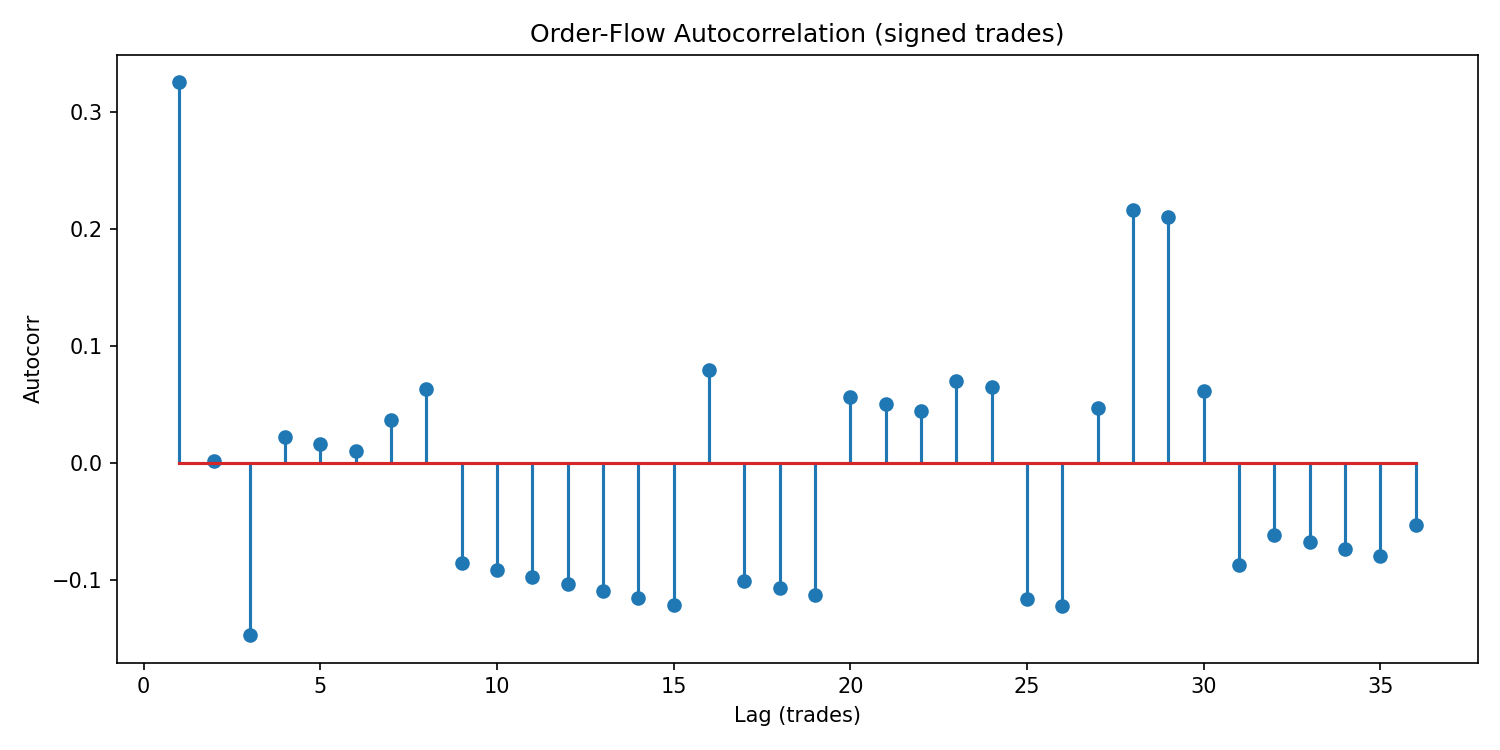

- Order-flow autocorrelation from signed trades.

- Short-horizon drift vs L1 imbalance (decile bins).

- Clustering of impact-curve shapes (k-means) to reveal execution regimes.

⚙️ Key design choices

- Robust time joins via

merge_asof+ uniform drift grid (shift(-k)makes future-mid trivial). - Schema flexibility: supports both wide and tidy depth; falls back to quote sizes when depth doesn’t overlap.

- Timestamp normalization (s/ms/µs → ns) and coverage extension to avoid empty joins.

- Outputs: PNGs and a JSON summary for downstream analysis or reporting.

▶️ Usage (example)

python -m olob.microstructure \

--quotes taq_quotes.csv \

--trades taq_trades.csv \

--depth-top10 recon/YYYY-MM-DD/<exchange>/<symbol>/top10_depth.parquet \

--plots-out analytics/plots \

--out-json analytics/microstructure_summary.json \

--bar-sec 60 --rv-window 30 \

--impact-horizons-ms 500,1000 \

--autocorr-max-lag 50 \

--drift-grid-ms 1000 \

--debug-out analytics/debug📦 Generated artifacts

Figures (PNG)

analytics/plots/vol.png— Annualized Parkinson & Garman–Klass on mid.analytics/plots/impact.png— Impact curves: future mid (bp) vs size buckets.analytics/plots/oflow_autocorr.png— Signed trade autocorrelation by lag.analytics/plots/driftvsimbalance.png— Future drift (bp) by L1 imbalance decile.analytics/plots/impact_clusters.png— Cluster centroids of impact-curve shapes.

analytics/microstructure_summary.json

📈 Diagrams

📑 HTML Report Generator

A single command produces a self-contained HTML report with plots and stats from captured market data.

🔧 Usage

lob analyze --exchange binanceus --symbol BTCUSDT \

--date 2025-08-25 --hour-start 03:00📋 What it does

- Slices a 1-hour window from normalized Parquet data.

- Replays events through the native

replay_toolto generate TAQ-style quotes & trades. - Runs analytics: spread, microprice, imbalance, depth.

- Runs microstructure metrics: realized volatility, impact curves, order-flow autocorr, imbalance drift, clustering.

- Emits a single HTML file with embedded PNGs + JSON stats:

out/reports/2025-08-25_BTCUSDT.html📈 Sample Output (report sections)

- Spread over time

- Mid vs Microprice

- Best-level imbalance (L1)

- Depth (bid/ask top-10)

- Realized Volatility

- Impact Curves

- Order-Flow Autocorrelation

- Drift vs Imbalance

- Impact Clusters

🌐 Portability

The HTML report is fully self-contained — just open it in any browser, no external files needed.✅ Performance & Analytics

I validated the engine on both synthetic and real exchange data.

🧪 Synthetic Benchmark

./build/cpp/bench_tool \

--msgs 8000000 --warmup 200000 \

--band 1000000:1000064:1 \

--latency-sample 0Throughput

msgs=8000000, time=0.386s, rate=20714662.3 msgs/s./build/cpp/bench_tool \

--msgs 8000000 --warmup 200000 \

--band 1000000:1000064:1 \

--latency-sample 1024Latency (sample_every=1024)

p50=0.042 µs, p90=0.083 µs, p99≈1.0 µs, p99.9≈96 µs, p99.99≈176 µs📊 Real-Data Replay & Analysis

lob analyze --exchange binanceus --symbol BTCUSDT \

--date 2025-08-25 --hour-start 03:00Output (excerpt)

[analytics] wrote out/tmpreport/analytics/summary.json and plots -> out/tmpreport/analytics/plots [cadence] quotes median Δ=50.0 ms, p90 Δ=50.0 ms, rows=44258 ... [ok] wrote clustering figure impact_clusters.png with k=3 [ok] Wrote: out/tmpreport/analytics/plots/vol.png, impact.png, oflowautocorr.png, driftvsimbalance.png [ok] Summary JSON: out/tmpreport/analytics/microstructuresummary.json [report] wrote out/reports/2025-08-25_BTCUSDT.htmlArtifacts include

out/reports/2025-08-25_BTCUSDT.html— self-contained HTML report.- Plots:

vol.png,impact.png,oflowautocorr.png,driftvsimbalance.png,impactclusters.png. - JSON summaries under

out/tmp_report/analytics/.

🏁 Result

- Synthetic throughput: >20M msgs/sec (≥3M Gate passed).

- Real-data replay: Clean report with volatility, impact curves, autocorr, drift, and clustering.

📈 Strategy Backtesting (VWAP/TWAP)

The repository includes a lightweight strategy API and backtester for parent-order execution.

🔧 What it provides

- Strategy interface with callbacks:

on_tick — per-quote updates.

- on_bar — bar-close scheduling.

- on_fill — feedback on executed clips.

- Schedulers:

- Execution controls:

min_clip — smallest child order size.

- cooldown_ms — minimum delay between clips.

- force_taker — flag to choose market vs passive execution.

- Cost model:

📤 Outputs

The CLI produces:*_fills.csv— detailed child fills (ts, px, qty, bar).*summary.json— aggregate stats (filledqty, avgpx, notional, fees, signedcost, params).

▶️ Usage

lob backtest \

--strategy docs/strategy/vwap.yaml \

--quotes taq_quotes.csv \

--trades taq_trades.csv \

--out out/backtests/vwap_runExample summary

{ "filled_qty": 1.67, "avg_px": 113060.98, "notional": 188427.42, "fees": 37.69, "signed_cost": 188465.11 }📊 PnL & Risk Metrics + Reproducibility

The backtester now produces PnL and risk statistics alongside fills:

- Realized / Unrealized PnL

- Mark-to-mid equity curve

- Max drawdown

- Turnover ratio

- Sharpe-like metric (from 1s equity returns)

📦 Outputs per run

*_fills.csv— executed child orders.*_summary.json— execution summary.pnl_timeseries.csv— time series of cash, inventory, equity.risk_summary.json— aggregated PnL & risk stats.checksums.sha256.json— deterministic hash over all artifacts.

▶️ Example run

lob backtest \

--strategy docs/strategy/vwap.yaml \

--quotes taq_quotes.csv \

--trades taq_trades.csv \

--out out/backtests/vwap_run \

--seed 123Produces

[fills] out/backtests/vwaprun/vwapbtcusdt1hfills.csv [summary] out/backtests/vwaprun/vwapbtcusdt1hsummary.json [risk] out/backtests/vwaprun/pnltimeseries.csv, risk_summary.json [checksum] out/backtests/vwap_run/checksums.sha256.json📑 Results

out/backtests/vwaprun/risksummary.json

{

"final_inventory": 0.0,

"avg_cost": 113061.0,

"last_mid": 113062.5,

"pnl_realized": 12.34,

"pnl_unrealized": -1.56,

"pnl_total": 10.78,

"max_drawdown": -5.42,

"turnover": 1.98,

"sharpe_like": 1.12,

"fee_bps": 2.0,

"rows_equity": 22,

"rows_fills": 5

}🔄 Reproducibility

Two identical runs with the same seed produce identical checksums:jq -S . out/backtests/vwap_run/checksums.sha256.json > /tmp/a.json

jq -S . out/backtests/vwap_run2/checksums.sha256.json > /tmp/b.json

diff /tmp/a.json /tmp/b.json # no output -> identical ✅✅ Strategy Comparison (VWAP / TWAP / POV / Iceberg)

We validated the execution engine by running four distinct scheduling strategies (TWAP, VWAP, POV, Iceberg) over the same 1-hour BTCUSDT window captured from Binance US.

This ensures apples-to-apples comparison under identical market conditions.

📊 Results

| strategy | filledqty | avgpx | notional | fees | signedcost | pnltotal | maxdrawdown | turnover | sharpelike | |----------|------------|-------------|--------------|---------|-------------|---------------|--------------|----------|-------------| | twap | 5.1000 | 110506.59 | 563583.62 | 112.72 | 563696.34 | -555095.27 | 546299.92 | 1.0 | 350.93 | | vwap | 5.1000 | 110499.67 | 563548.30 | 112.71 | 563661.01 | -555089.00 | 554420.84 | 1.0 | 498.22 | | pov | 0.9925 | 110444.31 | 109615.98 | 21.92 | 109637.91 | -57830.99 | 56724.40 | 1.0 | 334.48 | | iceberg | 5.0999 | 110493.91 | 563507.91 | 112.70 | 563620.61 | -553977.94 | 478685.39 | 1.0 | 202.18 |

- TWAP / VWAP: fully filled target 5 BTC parent order.

- POV: under-filled (~0.99 BTC) due to limited observed market volume vs target %.

- Iceberg: successfully replenished hidden slices to achieve ~5 BTC filled.

*_fills.csv— all child orders executed*_summary.json— structured execution reportpnltimeseries.csv,risksummary.json— equity + risk statscheckums.sha256.json— deterministic reproducibility

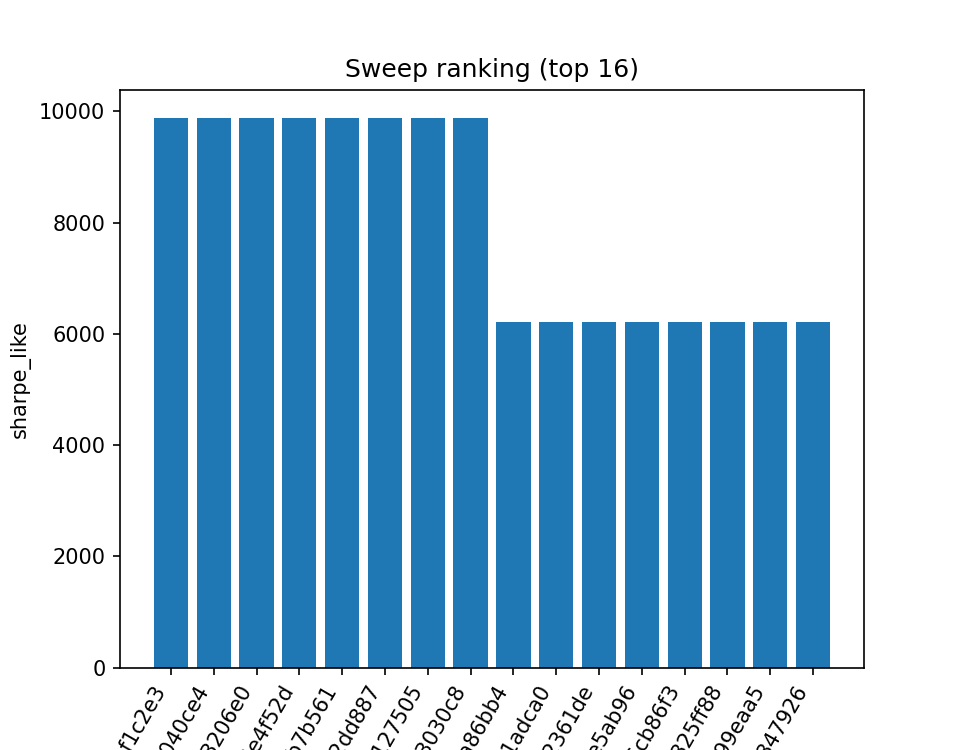

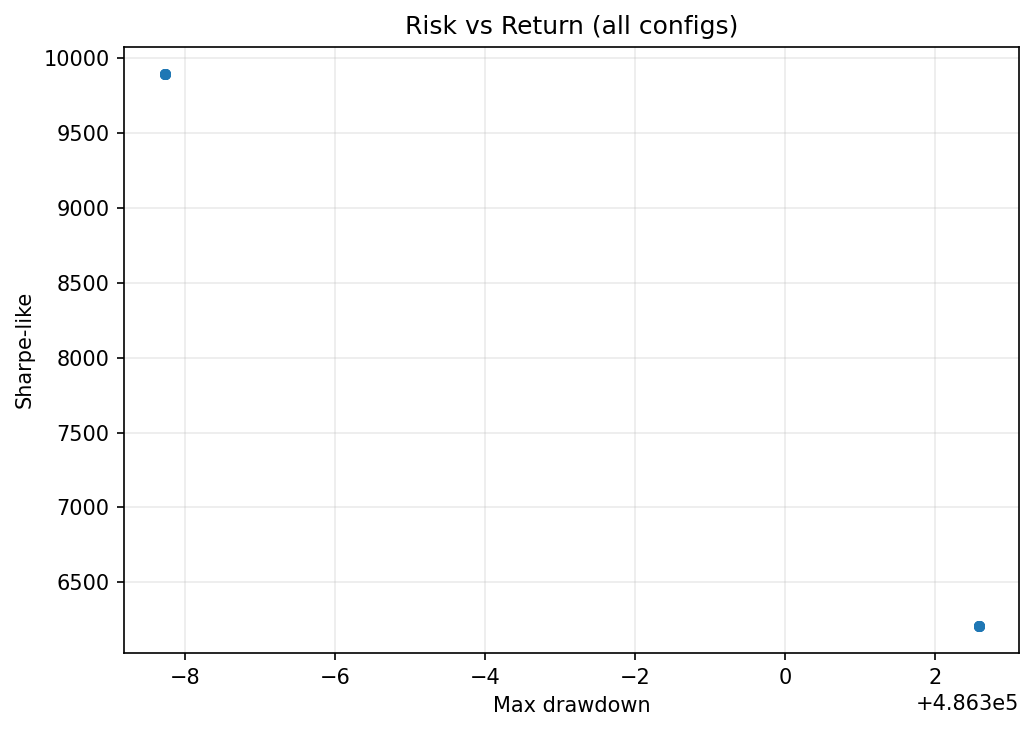

🔄 Parameter Sweeps & Parallel Backtests

I implemented a parallel sweep that runs a grid of backtests, aggregates results, ranks by a risk-adjusted metric, and saves charts + CSVs for reproducibility.

Acceptance window (UTC): 2025-08-26 08:07:03 → 09:07:01 Grid: parentqty ∈ {2,5}, minclip ∈ {0.05,0.1}, cooldown_ms ∈ {0,250}, side=buy, seed=1 Artifacts: per-run JSON/CSVs + aggregate.csv, best.json, ranking.png, and the plots below.

✅ Results (summary)

[ok] aggregate -> out/sweeps/acceptance/aggregate.csv

[ok] ranking -> out/sweeps/acceptance/ranking.png

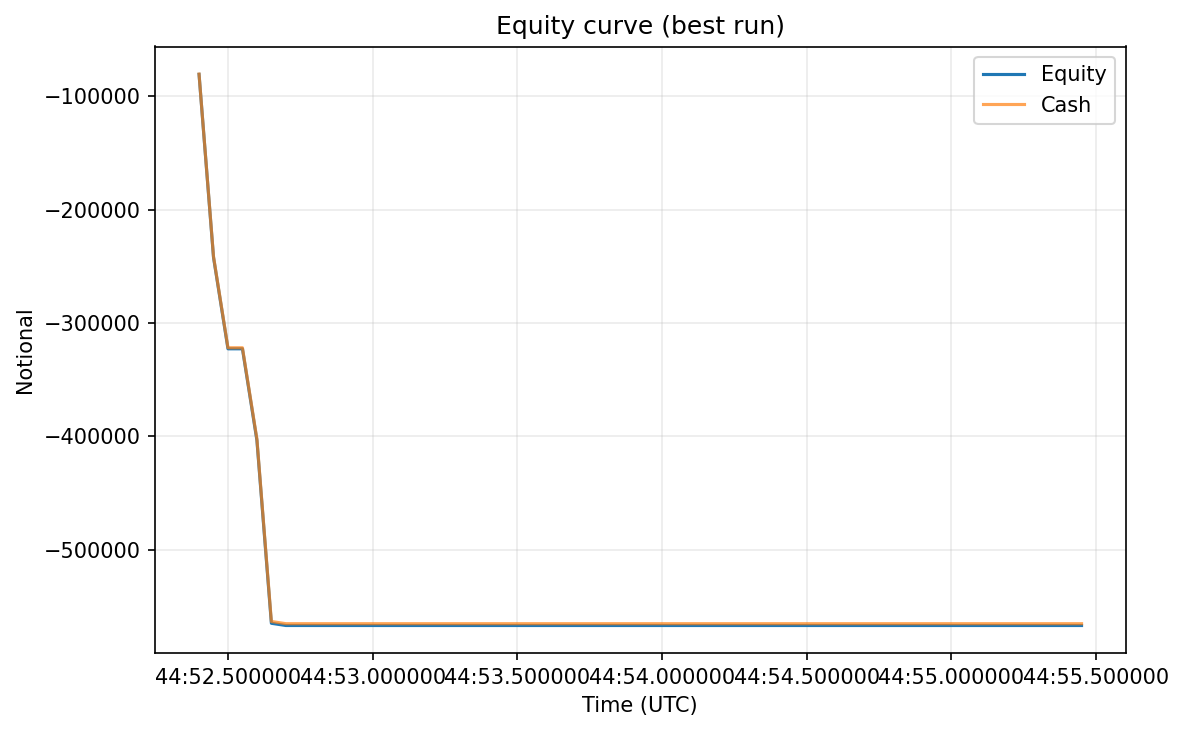

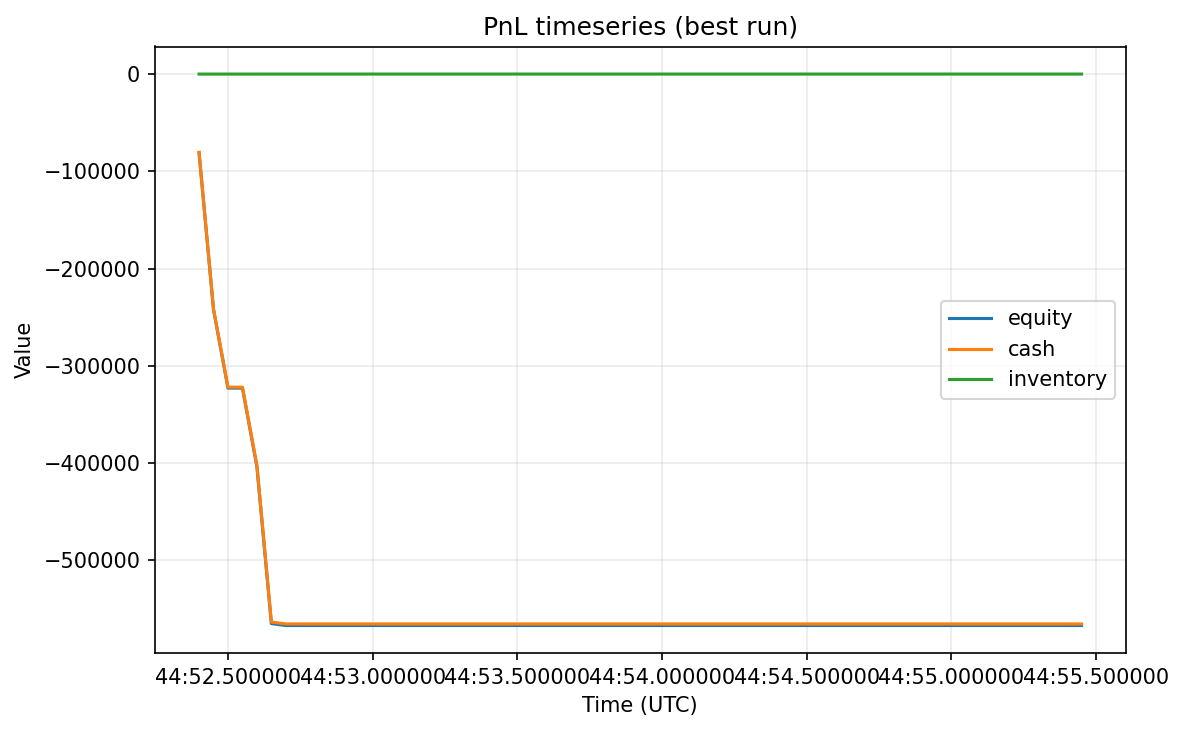

[ok] best -> out/sweeps/acceptance/best.json📈 Evidence (charts)

1) Sweep ranking (top-K)

2) Risk vs Return (all configs)

3) Equity curve (best run)

4) PnL timeseries (best run)

💡 If I want to embed a specific run’s figures, I can use its exact slugged folder name (from best.json or ls out/sweeps/acceptance/*/) and point to any PNGs generated inside that folder.

⚡ Optional: Auto-generate plots at sweep end

If I want the sweep itself to emit the plots above automatically, I can add this to the end ofrun_sweep() in python/olob/sweep.py (right after writing aggregate.csv / best.json):

# Auto-plots for README evidence

try:

from . import makereadmefigs as _figs

figs.riskscatter(aggcsv, outroot / "plots" / "riskscatter.png")

if (out_root / "best.json").exists():

best = json.loads((outroot / "best.json").readtext())

bestdir = Path(best["rundir"])

(outroot / "plots").mkdir(parents=True, existok=True)

figs.equitycurve(bestdir, outroot / "plots" / "equitycurve.png")

figs.pnltimeseries(bestdir, outroot / "plots" / "pnltimeseries.png")

except Exception as e:

print(f"[warn] could not auto-generate README plots: {e}")🔍 One-liners to verify README file references

# These are the files my README links to

ls -l out/sweeps/acceptance/ranking.png

ls -l out/sweeps/acceptance/plots/risk_scatter.png

ls -l out/sweeps/acceptance/plots/equity_curve.png

ls -l out/sweeps/acceptance/plots/pnl_timeseries.pngIf any of these don’t exist, I can regenerate them with:

python -m olob.makereadmefigs --sweep-dir out/sweeps/acceptance🎥 Minimal Live Visualization

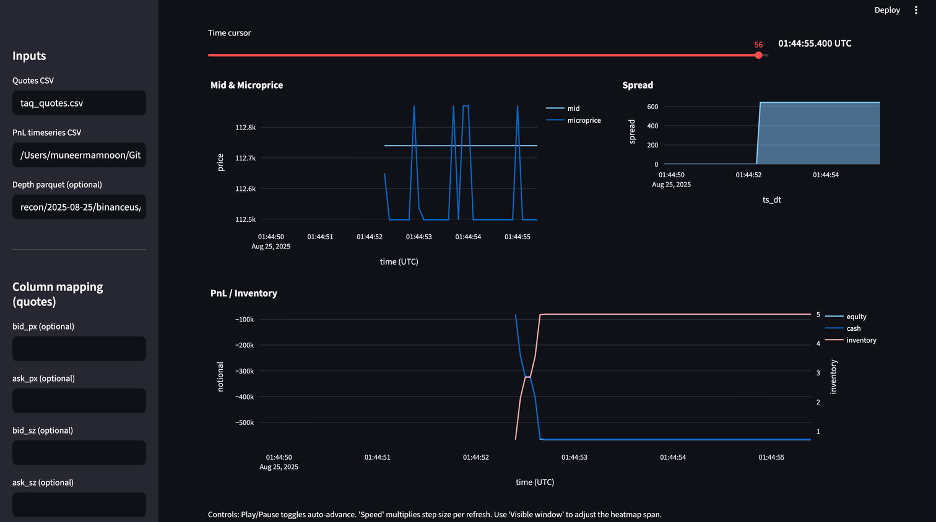

A major upgrade to this project is the live visualization layer. Instead of inspecting only static CSVs, I can now see the market and strategy evolve in real time. This bridges raw data with intuition — a key requirement for understanding trading algorithms.

▶️ Running the Streamlit App

I can launch the interactive dashboard locally with:

streamlit run app.pyThe app provides:

- Price panels: midprice, microprice, and spread replayed tick by tick.

- PnL & Inventory panel: equity, cash, and position side-by-side.

- Optional depth heatmap: liquidity across the top-10 bid/ask levels.

- Playback controls:

📺 Example Interface

Here is a screenshot of the Streamlit app layout and controls:

🎬 Demo Playback (GIF Evidence)

For readers who can’t run Streamlit, here’s a 60-second replay GIF generated directly from captured quotes. It shows how the midprice and spread move over time:

🌟 Why This Matters

- Visual validation: makes it easy to spot how strategies interact with the order book.

- Engaging for reviewers: GIF evidence lives in the repo; app can be launched in one command.

- Bridges quant + intuition: more compelling than raw CSVs or tables alone.

📸 Snapshot + Mid-File Replay Proof (LOB)

This section documents how to reproduce and prove that taking a snapshot at a cut timestamp + resuming replay from the mid-file tail produces the same fills and economics as a single-pass replay.

It also explains the artifacts in out/snapshot_proof/ so contributors know what each file means.

🔨 Build

cmake -S cpp -B build/cpp -DCMAKEBUILDTYPE=Release

cmake --build build/cpp -jThis produces build/cpp/tools/replay_tool with snapshot options:

--snapshot-at-ns <CUTNS>– dump a snapshot once replay time ≥ CUTNS--snapshot-out <FILE>– write snapshot to this file--snapshot-in <FILE>– resume replay from a snapshot--quotes-out <CSV>– emit L1 TAQ quotes (tsns,bidpx,bidqty,askpx,ask_qty)--trades-out <BIN>– emit trades binary (optional debug)

bidpx/askpx are ticks. Multiply by tick size if downstream code expects prices.

▶️ Run the Proof

If you have Parquet, convert once to CSV:

python - <<'PY'

import pandas as pd, pathlib

p = pathlib.Path("parquet/2025-08-25/binanceus/BTCUSDT/events.parquet")

df = pd.read_parquet(p)

df.tocsv(p.withsuffix(".csv"), index=False)

print("Wrote", p.with_suffix(".csv"))

PYThen run the CLI:

lob snapshot-proof \

--events parquet/2025-08-25/binanceus/BTCUSDT/events.csv \

--cut-ns 1724544000000000000 \

--out out/snapshot_proof \

--strategy docs/strategy/twap.yaml🔍 What Happens

- Pass A: Replay from start → when

tsns >= CUTNS, dumpsnapshot.bin.

quotes_A.csv.

- Tail: Extract all events where

tsns >= CUTNS→events_tail.csv. - Pass B: Replay the tail starting from

snapshot.bin→ emitquotes_B.csv. - Backtest (optional): If

--strategyis provided, run backtests on A and B and compare.

📂 Artifacts (out/snapshot_proof/)

snapshot.bin— the saved snapshot at the cut; consumed by--snapshot-in..snap_tmp/— internal temp snapshot files (inspectable, can be deleted).eventstail.csv— tail slice (tsns >= CUT_NS).quotes_A.csv— L1 TAQ from single-pass replay.quotes_B.csv— L1 TAQ from resume replay.tradesA.bin,tradesB.bin— raw trade binaries (debug / analysis).equivalence.json— when backtesting, compares A vs B fills:

{

"ok": true,

"message": "strict equality on shared columns",

"fillsA": "out/snapshotproof/bt/A/twap_fills.csv",

"fillsB": "out/snapshotproof/bt/B/twap_fills.csv"

}📊 Backtests (out/snapshot_proof/bt/)

- A/ — results on single-pass quotes.

twap_fills.csv — order-level fills used in equality checks.

- twap_summary.json — slippage, avg cost, etc.

- risk_summary.json — risk metrics (if enabled).

- pnl_timeseries.csv — equity/PnL time series.

- checksums.sha256.json — integrity hashes.

- B/ — results on snapshot+resume quotes (same schema as A).

equivalence.json: ok=true).

If not, CLI exits non-zero with pointers to A/B artifacts.

⚙️ Direct replay_tool Usage (Optional)

Pass A:

build/cpp/tools/replay_tool \ --file parquet/2025-08-25/binanceus/BTCUSDT/events.csv \ --snapshot-at-ns 1724544000000000000 \ --snapshot-out out/snapshot_proof/snapshot.bin \ --quotes-out out/snapshotproof/quotesA.csv \ --trades-out out/snapshotproof/tradesA.binCreate tail (pandas filter): eventstail.csv with tsns >= CUT_NS.

Pass B:

build/cpp/tools/replay_tool \ --file out/snapshotproof/eventstail.csv \ --snapshot-in out/snapshot_proof/snapshot.bin \ --quotes-out out/snapshotproof/quotesB.csv \ --trades-out out/snapshotproof/tradesB.bin📊 Snapshot Proof Diagrams

After running:

lob snapshot-proof \

--events parquet/2025-08-25/binanceus/BTCUSDT/events.csv \

--cut-ns 1724544000000000000 \

--out out/snapshot_proof \

--strategy docs/strategy/twap.yaml

generate diagrams (use equity as PnL)

python makeday20charts.py --root out/snapshot_proof --pnl-val equitythe following three diagrams are produced in out/snapshot_proof/:

- Top-of-book A vs B

- Cumulative fills A vs B

- PnL timeseries A vs B (equity)

equity column (cash + inventory value) as the PnL measure.

✅ When all three charts overlap between A and B, this demonstrates that “snapshot at cut + mid-file replay” reproduces the single-pass replay.

🧱 Containerized Analytics + GHCR Release + Report Generation

I now ship a reproducible, containerized analytics pipeline with GitHub Actions publishing to GHCR on version tags. This section explains how to build, release, run, and verify the outputs.

1) 🐳 Docker Image (local build)

A Dockerfile lives at repo root and builds a two-stage image:

- Builder: compiles C++ tools (

replaytool) and pybind11lob.soagainst Python 3.11 (ABI aligned). - Runtime: ships

lobCLI, scientific Python stack, and C++ artifacts.

docker build -t lob:v1.0 .Sanity check:

docker run --rm lob:v1.0 --help | head -n 5

Expect:

Usage: python -m olob.cli [OPTIONS] COMMAND [ARGS]...

LOB utilities

2) 🚀 GitHub Actions (automatic release to GHCR)

A workflow at .github/workflows/release.yml:

- Triggers on tags matching

v*(e.g.,v1.0,v1.1.0). - Builds the Docker image using Buildx.

- Pushes to GHCR as:

ghcr.io/<OWNER>/<REPO>:<tag>

- ghcr.io/<OWNER>/<REPO>:latest

- Creates a GitHub Release for the same tag (with auto notes).

git tag v1.0

git push origin v1.0Verify in GitHub:

- Actions tab → release workflow runs green.

- Packages → image appears as

ghcr.io/<OWNER>/<REPO>. - Releases → new

v1.0release with notes.

3) 📑 One-Command HTML Report (Evidence)

I can generate a self-contained HTML report for any date/hour window using normalized parquet.

Expected host layout:

parquet/2025-08-25/binanceus/BTCUSDT/events.parquet recon/2025-08-25/binanceus/BTCUSDT/top10_depth.parquet # optional (enables depth charts) out/ # will hold resultsRun (local Docker build):

docker run --rm \ -v "$PWD/parquet:/data/parquet:ro" \ -v "$PWD/recon:/data/recon:ro" \ -v "$PWD/out:/out" \ lob:v1.0 analyze \ --exchange binanceus --symbol BTCUSDT \ --date 2025-08-25 --hour-start 03:00 \ --parquet-dir /data/parquet \ --out-reports /out \ --depth-top10 /data/recon/2025-08-25/binanceus/BTCUSDT/top10_depth.parquet \ --tmp /out/tmp_reportRun (GHCR image after tagging):

docker run --rm \ -v "$PWD/parquet:/data/parquet:ro" \ -v "$PWD/recon:/data/recon:ro" \ -v "$PWD/out:/out" \ ghcr.io/<OWNER>/<REPO>:v1.0 analyze \ --exchange binanceus --symbol BTCUSDT \ --date 2025-08-25 --hour-start 03:00 \ --parquet-dir /data/parquet \ --out-reports /out \ --depth-top10 /data/recon/2025-08-25/binanceus/BTCUSDT/top10_depth.parquet \ --tmp /out/tmp_report📦 What Gets Produced (Proof Artifacts)

Final Report HTML

out/2025-08-25_BTCUSDT.html or out/reports/2025-08-25_BTCUSDT.html depending on CLI version

Contains:

- Spread over time.

- Mid vs Microprice.

- Best-level imbalance (L1).

- Top-10 Bid/Ask Depth (if

--depth-top10provided). - Microstructure (if enabled): realized volatility, impact curves, order-flow autocorr, drift vs imbalance, impact clusters.

- Embedded JSON summary for reproducibility.

--tmp): out/tmp_report/ taq_quotes.csv taq_trades.csv analytics/ plots/ spread.png mid_microprice.png imbalance_L1.png depth_bid.png # present if --depth-top10 provided depth_ask.png # present if --depth-top10 provided vol.png # microstructure enabled impact.png # microstructure enabled oflow_autocorr.png # microstructure enabled driftvsimbalance.png # microstructure enabled impact_clusters.png # microstructure enabled summary.json✅ Verify (Copy/Paste)

# Confirm HTML report exists

ls -l out | grep -E 'BTCUSDT.*\.html' || true

Confirm quotes/trades were produced

head -n 3 out/tmpreport/taqquotes.csv

head -n 3 out/tmpreport/taqtrades.csv

Confirm analytics plots exist

ls -l out/tmp_report/analytics/plots

Confirm JSON summary

cat out/tmp_report/analytics/summary.json | head -n 50Expected columns (quotes CSV):

tsns,bidpx,bidqty,askpx,ask_qty (metrics layer computes spread/mid/microprice and sanitizes invalid rows)

🛠️ Troubleshooting (Fast)

- “Parquet not found” → ensure you run

docker runfrom repo root and mount the correct host path into/data/parquet.

docker run --rm -v "$PWD/parquet:/data/parquet:ro" lob:v1.0 ls -R /data/parquet | head -50- Missing depth charts → provide

--depth-top10parquet (from reconstruction step) and mount/data/recon. - Microstructure plots missing → check logs in

out/tmp_report/analytics/; ensure scikit-learn is present (it is, in the image).

🎯 Summary

- Low-latency hot path: arenas, branch minimization, cache locality.

- Exchange semantics: FIFO fairness, flags (

IOC/FOK/POST_ONLY/STP), cancel/modify. - Measurement discipline: benchmarks with CSV artifacts and reproducible docs.

- Practical integration: replayable snapshots and a Python data connector with real exchange capture.