An optimal trading trajectory solver.

Last updated Mar 31, 2026

40

Stars

9

Forks

0

Issues

0

Stars/day

Attention Score

29

Language breakdown

No language data available.

▸ Files

click to expand

README

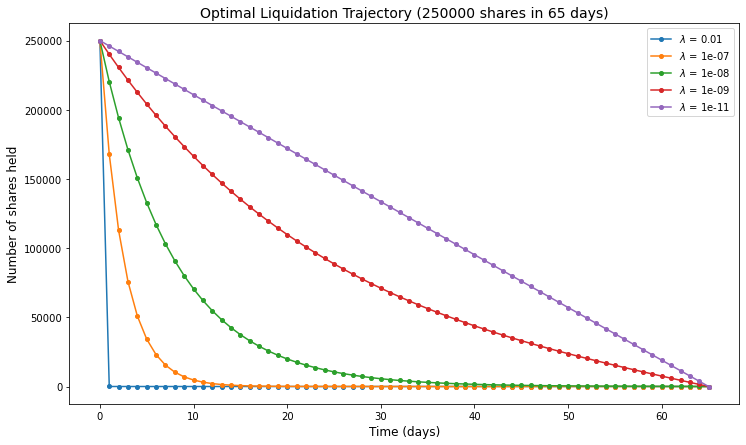

Almgren-Chriss Optimal Execution Model

The aim of the Almgren-Chriss optimal execution model is to minimize a combination of volatility risk and transaction costs arising from permanent and temporary market impact. In this notebook, we study the model for liquidation of large positions with real financial data.

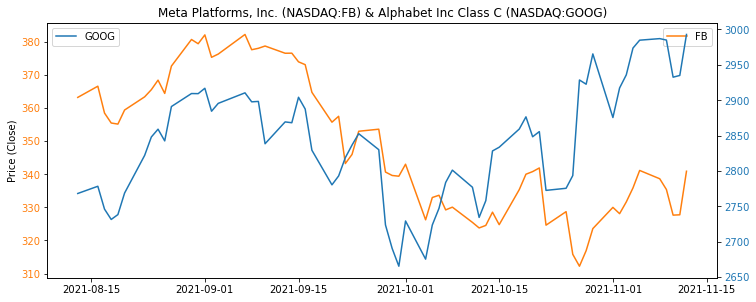

Correlated Assets

We numerically illustrate the model with financial data for two correlated assets. In particular, we use the daily historical prices of Alphabet Inc. (NASDAQ:GOOG) and Meta Platforms, Inc. (NASDAQ:FB) over three months.Stock Prices

Optimal Trading Trajectory

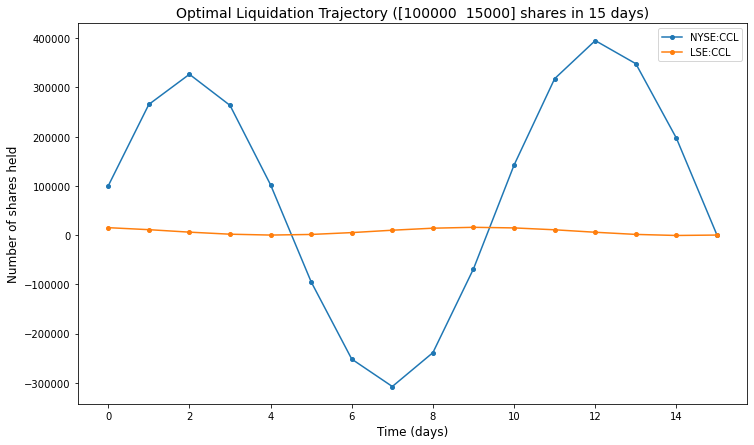

Cross-Market Manipulation

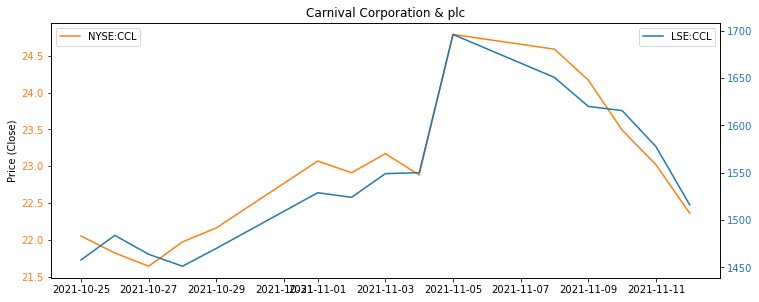

We explore a particular case of trading shares of the same company on different exchanges. In particular, we explore the optimal strategy for closing a position of Carnival Corporation & plc (CCL) over 15 days. CCL is a British-American cruise operator which is currently the world's largest travel leisure company. Shares of CCL are traded on both the NYSE and the LSE. See Jupyter notebook for more details.Stock Prices

Optimal Trading Trajectory