Hybrid Event-driven and Vectorized Strategy Backtesting Library

TradeMind: C++ Algorithmic Trading and Backtesting Framework

TradeMind is a high-performance, professional-grade quantitative trading platform designed for algorithmic trading, with a focus on low-latency execution, advanced strategy development, and real-time market microstructure visualization analysis.

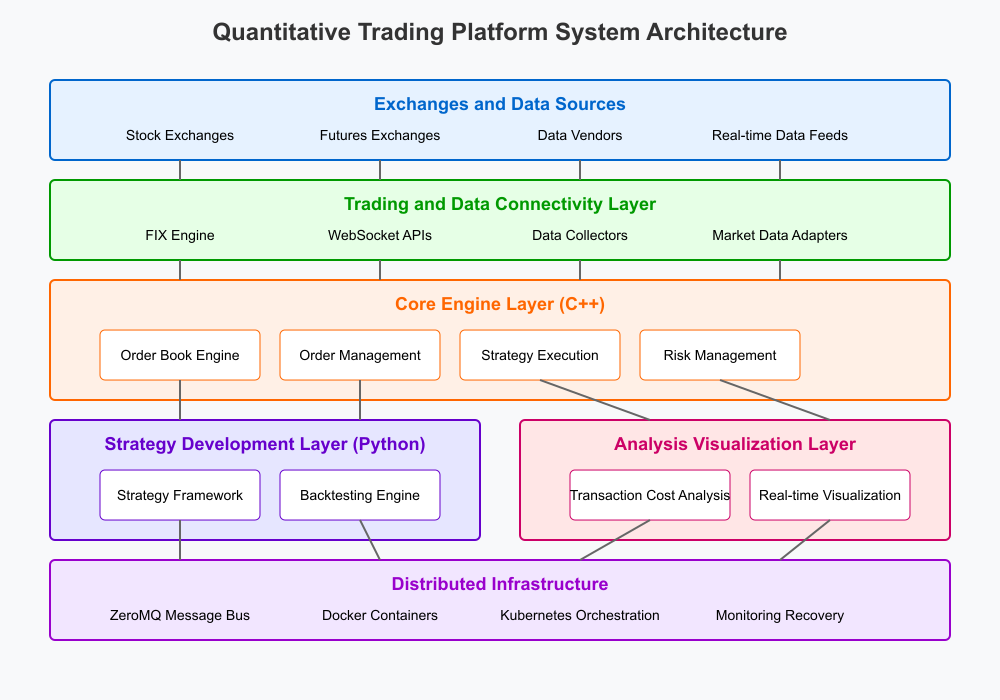

System Architecture

The platform consists of five key layers:

- Exchanges and Data Sources Layer

- Trading and Data Connectivity Layer

- Core Engine Layer (C++)

- Strategy Development Layer (Python)

- Analysis & Visualization Layer

All these components are supported by a robust Distributed Infrastructure layer that includes: - ZeroMQ message bus for low-latency inter-component communication - Docker containerization for deployment flexibility - Kubernetes orchestration for scaling and management - Comprehensive monitoring and automatic recovery systems

Key Features

- High-Performance Core Engine: C++ implementation of critical components ensures microsecond-level response time

- Real-time Market Microstructure Analysis: Capture and analyze order book dynamics and liquidity metrics

- Flexible Strategy Development: Python API for rapid strategy development using machine learning and quantitative models

- Comprehensive Backtesting: Event-driven backtesting engine with realistic market simulation

- Low-Latency Order Execution: FIX protocol integration for direct exchange connectivity

- Distributed Architecture: Microservices design with ZeroMQ messaging for horizontal scalability

- Cloud-Ready Deployment: Containerized services that can be deployed in cloud environments

Getting Started

Prerequisites

- C++17 compatible compiler (GCC 7+, Clang 5+, MSVC 2019+)

- CMake 3.15+

- Python 3.8+

- ZeroMQ 4.3+

- Boost 1.70+

- Fix8 (for FIX protocol support)

- YAML-CPP

Building from Source

- Clone the repository:

git clone https://github.com/jialuechen/trademind.git

cd trademind- Build the C++ components:

mkdir build && cd build

cmake ..

make -j$(nproc)- Install the Python package:

cd python

pip install -e .Configuration

Edit the configuration files in the config directory to set up:

- Exchange connections

- Market data sources

- Risk parameters

- Logging preferences

- Performance settings

config/config.yaml.

Running the Platform

To start the platform with default settings:

./bin/trademindTo specify a custom configuration file:

./bin/trademind --config /path/to/custom_config.yamlStrategy Development

TradeMind provides a powerful Python API for developing trading strategies. Here's a minimal example:

from pyquant import Strategy, Context, OrderSide, OrderType

class SmaStrategy(Strategy): def initialize(self) -> None: # Set strategy parameters self.parameters = { "symbol": "AAPL", "fast_period": 10, "slow_period": 30, "trade_size": 100 } # Add symbols to trade self.context.symbols = [self.parameters["symbol"]] def onbar(self, context: Context, bardict) -> None: symbol = self.parameters["symbol"] bars = bar_dict[symbol] # Calculate moving averages fastma = bars['close'].rolling(self.parameters["fastperiod"]).mean() slowma = bars['close'].rolling(self.parameters["slowperiod"]).mean() # Get current position position = context.get_position(symbol) # Trading logic: Buy when fast MA crosses above slow MA if fastma.iloc[-2] <= slowma.iloc[-2] and fastma.iloc[-1] > slowma.iloc[-1]: if position.quantity <= 0: self.buy(symbol, self.parameters["trade_size"]) # Sell when fast MA crosses below slow MA elif fastma.iloc[-2] >= slowma.iloc[-2] and fastma.iloc[-1] < slowma.iloc[-1]: if position.quantity >= 0: self.sell(symbol, self.parameters["trade_size"])

Backtesting

To backtest a strategy:

from pyquant import BacktestEngine, BacktestVisualizer, Timeframe

import pandas as pd

Load historical data

data = pd.readcsv("data/AAPLdaily.csv", indexcol='date', parsedates=True)

Create and configure strategy

strategy = SmaStrategy()

Set up backtest engine

backtest = BacktestEngine()

backtest.add_strategy(strategy)

backtest.addbardata("AAPL", Timeframe.D1, data)

Run backtest

results = backtest.run(

start_time=data.index[100],

end_time=data.index[-1],

initial_capital=100000.0

)

Visualize results

visualizer = BacktestVisualizer()

visualizer.generate_report(results)Parameter Optimization

TradeMind includes tools for strategy parameter optimization:

from pyquant import StrategyOptimizer

Create optimizer

optimizer = StrategyOptimizer(SmaStrategy)

optimizer.addbardata("AAPL", Timeframe.D1, data)

Define parameter grid

param_grid = {

"fast_period": [5, 10, 15, 20],

"slow_period": [20, 30, 40, 50],

}

Run grid search

bestparams = optimizer.gridsearch(

paramgrid=paramgrid,

start_time=data.index[100],

end_time=data.index[-1],

optimizemetric='sharperatio'

)

print(f"Best parameters: {best_params}")

Distributed Deployment

For production environments, TradeMind can be deployed as a distributed system using Docker and Kubernetes:

cd docker

docker-compose up -dFor Kubernetes deployment:

kubectl apply -f kubernetes/trademind.yamlContributing

Contributions are welcome! Please check out our contributing guidelines for details on how to submit pull requests, report issues, or suggest improvements.

License

This project is licensed under the Apache License 2.0 - see the LICENSE file for details.