No description available.

Last updated Apr 7, 2026

13

Stars

5

Forks

0

Issues

0

Stars/day

Attention Score

7

Topics

Language breakdown

R 100.0%

▸ Files

click to expand

README

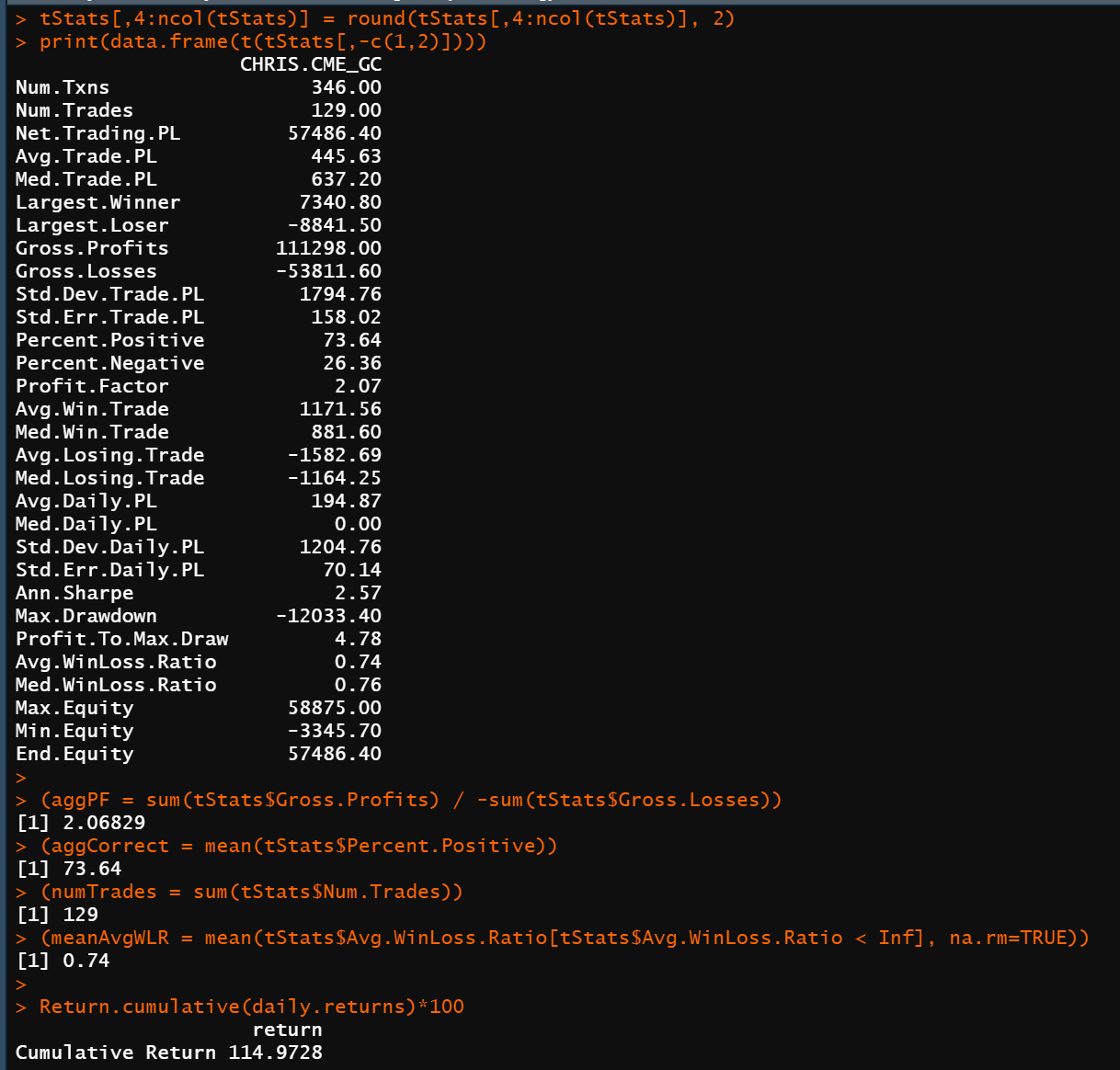

Gold Continuous-Futures Trading Algorithm in R

created using the quantstrat library_Huge credit and thank you to Ilya Kipnis for all of his time and effort spent creating walk-throughs and proper documentation for the quantstrat package.

For help getting started with quantstrat, quantmod, and performanceanalytics, check out the QuantstratTrader docs

This repository is created, developed, and maintained by:

Joseph Loss MS Financial Engineering University of Illinois at Urbana-Champaign contact: loss2@illinois.edu