Scalable implementation of Lee / Mykland (2012), Ait-Sahalia / Jacod (2012) and Ait-Sahalia / Jacod / Li (2012) Jump tests for noisy high frequency data

JumpDetectR

JumpDetectR

Name of QuantLet : JumpDetectR

Published in : "Understanding jumps in high frequency digital asset markets" (https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3944865)

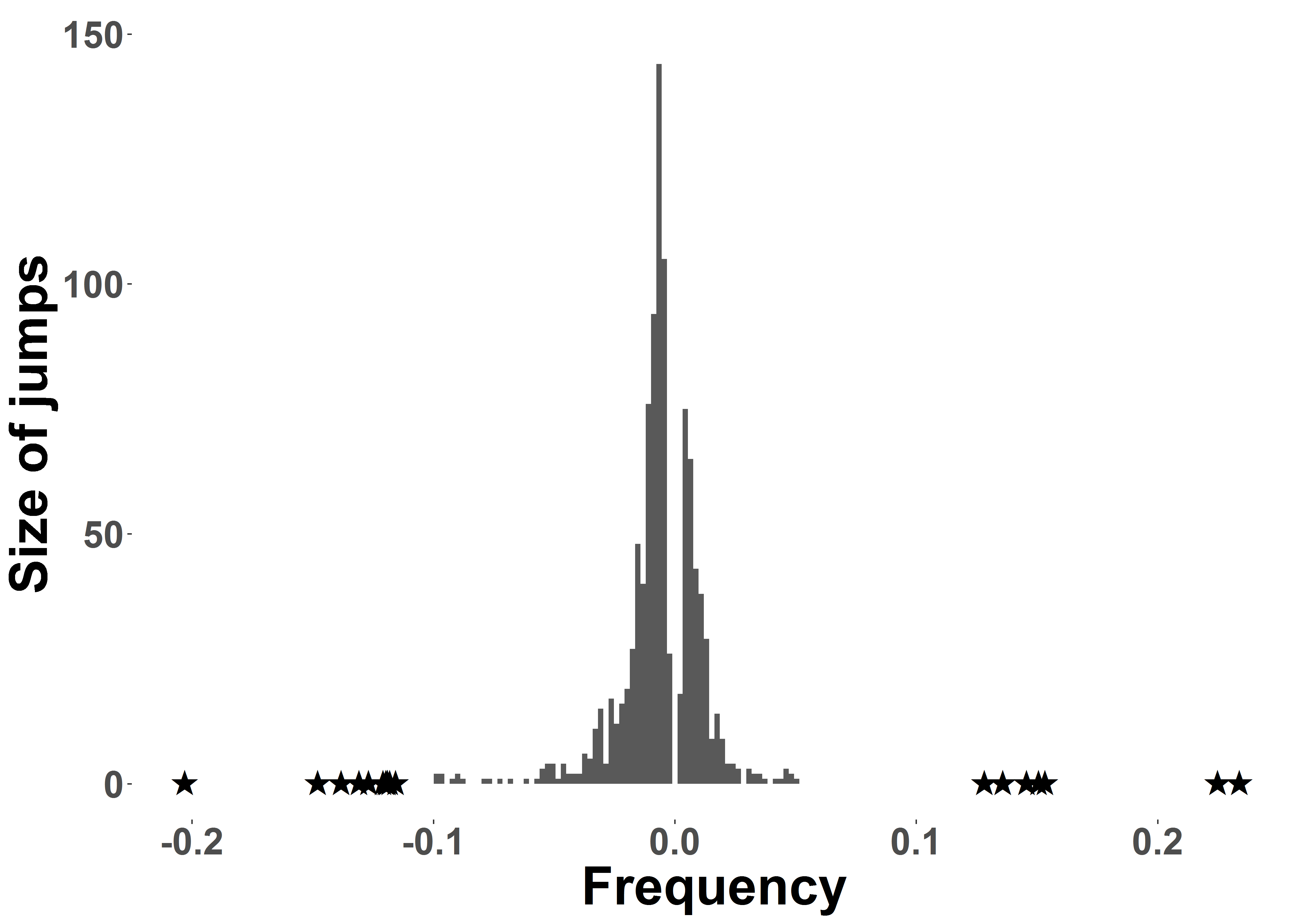

Description : 'Scalable implementation of Lee / Mykland (2012) and Ait-Sahalia / Jacod / Li (2012) Jump tests for noisy high frequency data'

Keywords : Jumps, jump test, high frequency, time series, Ait-Sahalia, Jacod, Lee, Mykland, stochastic processes, cryptocurrencies, cryptocurrency, crypto, spectrogram, microstructure, market microstructure noise, contagion, shocks

See also : 'Lee, S.S. and Mykland, P.A. (2012) Jumps in Equilibrium Prices and Market Microstructure Noise; Ait-Sahalia, Y. and Jacod, J., Jia Li (2012) Testing for jumps in noisy high frequency data'

Authors : Danial Florian Saef, Odett Nagy

Submitted : May 7 2021 by Danial Saef

R Code

## install and load packages ##

libraries = c("data.table")

lapply(libraries, function(x) if (!(x %in% installed.packages())) {install.packages(x)} )

invisible(lapply(libraries, library, quietly = TRUE, character.only = TRUE))

##

settings ####

Sys.setenv(LANG = "en") # set environment language to English

Sys.setlocale("LCTIME", "enUS.UTF-8") # set timestamp language to English

##

load functions #####

source("./functions/load_functions.R", echo = F)

##

load aggregate dataset ####

listDTagg <- loadandsplit("./data/raw/DTaggsub.csv")

get LM result ##

DTLMresultid <- jumptest(DTsplitnoimpute, whichtest = "LMJumpTest")

get AJL result ##

DTAJLresultid <- jumptest(DTsplitimpute, whichtest = "AJLJumpTest")

save results ##

fwrite(DTLMresultid, file = "./data/JumpTestResult/DTLMresultid.csv")

fwrite(DTAJLresultid, file = "./data/JumpTestResult/DTAJLresultid.csv")

##

automatically created on 2021-05-17