Quantitative factor research skills for AI coding assistants

Alpha Skills

Your AI-Powered Senior Quant Researcher.

Discover alpha. Evaluate factors. Monitor decay. Backtest strategies.

All through natural language — in any AI coding assistant.

Quick Start · What Can It Do · Multi-Market · Skills · Contribute

Hiring a quant researcher costs $300K/year. This one is free, open-source, and works 24/7.>

Alpha Skills turns any AI coding assistant into a senior quantitative researcher. It discovers factors, evaluates them with institutional-grade methodology (IC/ICIR/quintile/robustness), monitors for alpha decay, and runs multi-factor backtests — all from a single sentence.>

招一个量化研究员年薪百万。这个免费、开源、7×24小时工作。

What Can It Do

You say one sentence. It does the rest.

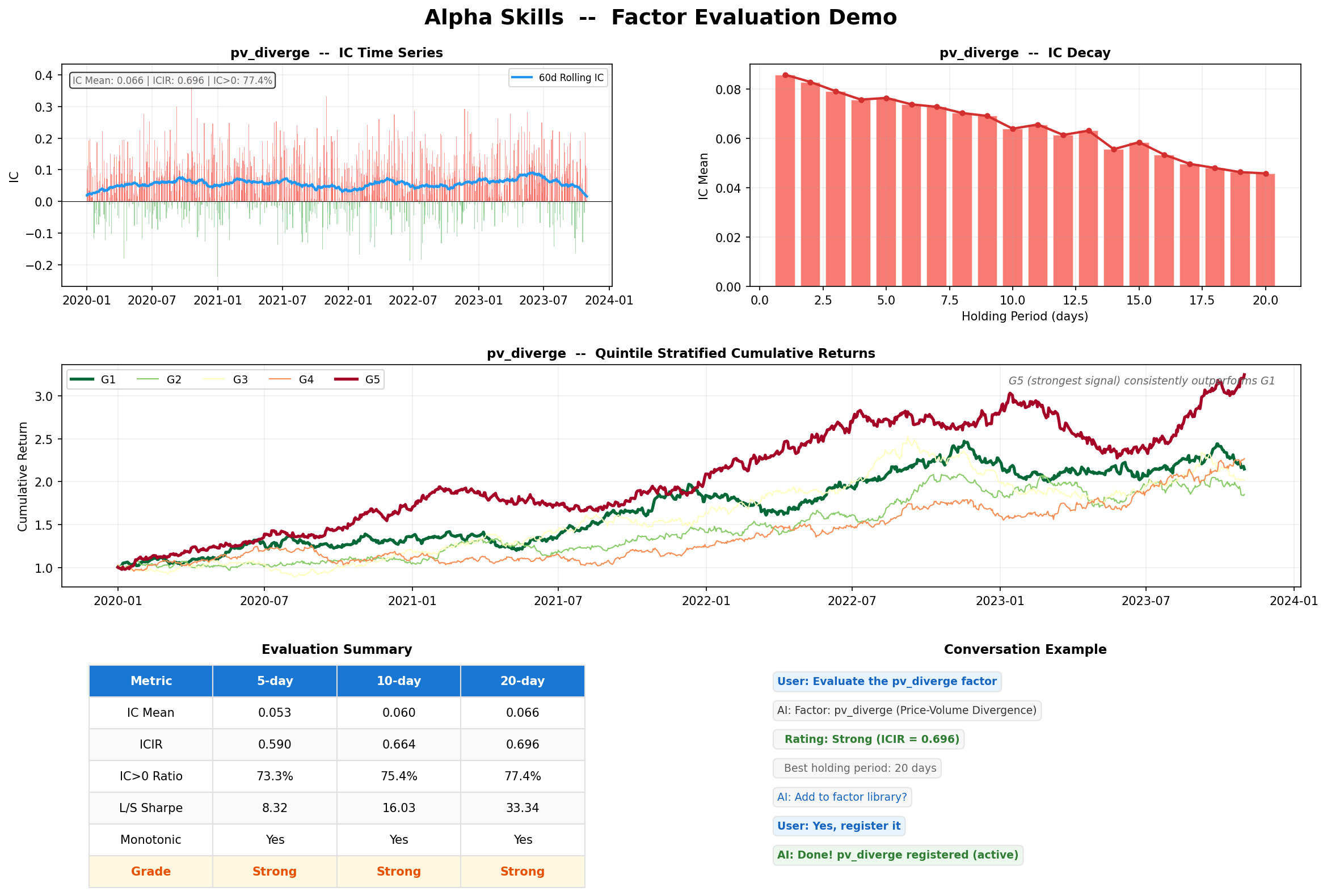

You: "Evaluate the price-volume divergence factor"

AI: 📊 IC Mean=0.066 | ICIR=0.696 | Rating: ⭐ Strong

Quintile spread monotonic. Best holding period: 20 days.

Report saved → output/evalpvdiverge.png

You: "Mine 50 candidate factors and show me the best ones" AI: ⛏️ Scanned 50 candidates → 12 passed IC screen Top: PV divergence 20d (ICIR=0.70), Low downside vol (ICIR=0.53)... Register to library?

You: "Backtest using my top 3 factors" AI: 📈 Sharpe=0.74 | MaxDD=-13.9% | Profit Factor=2.24 Gate check: ✓ PF>1 ✓ MDD>-25% ✗ Sharpe<1.0

No boilerplate. No notebooks. No 200 lines of pandas. Just results.

Skills Reference

| Skill | What It Does | Try Saying | |-------|-------------|------------| | 🔍 alpha-discover | Design factors from natural language | "find me a low-volatility factor" | | 📊 alpha-evaluate | IC / ICIR / quintile / long-short / robustness | "evaluate reversal_5" | | ⛏️ alpha-mine | Auto-mine factor candidates, IC screen, rank | "mine 50 factors" | | 📚 alpha-library | Register, list, search, retire factors (SQLite) | "show my factor library" | | 📈 alpha-backtest | Single & multi-factor portfolio backtest | "backtest with pv_diverge + turnover" | | 🏥 alpha-monitor | Detect IC decay, crowding, regime shift | "check factor health" | | 📋 alpha-report | Panoramic, deep-dive, comparison reports | "generate factor report" | | 📡 alpha-signal | Daily trading signal — target portfolio output | "today's signals" / "生成信号" | | 🤖 alpha-autopilot | Autonomous loop: mine → evaluate → register → monitor → retire | "run autopilot" / "自动驾驶" |

Quick Start

1. Get the skills

git clone https://github.com/VernonOY/alpha-skills.git2. Load into your AI assistant

| Platform | How | |----------|-----| | Cursor | Copy skills/alpha-*/SKILL.md → .cursorrules | | Windsurf | Copy → .windsurfrules | | Claude Code | cp -r skills/alpha-* ~/.claude/skills/ | | Any LLM | Paste SKILL.md as system prompt |

3. Install Python deps

pip install pandas numpy scipy matplotlib pyarrow

pip install tushare # A-share

pip install yfinance # US / HK4. Talk to it

"evaluate the momentum_20 factor"

"mine volatility factors"

"backtest my top 3 factors, 2022 to 2025"Multi-Market: A-Share · Hong Kong · US

Works out of the box for three markets. Auto-adapts trading rules per market:

| | A-share 🇨🇳 | Hong Kong 🇭🇰 | US 🇺🇸 | |---|---|---|---| | Data | Tushare Pro | Yahoo Finance | Yahoo Finance | | Price Limit | ±10% | None | None | | T+N | T+1 | T+0 | T+0 | | Cost | 0.3% | 0.2% | 0.1% | | Benchmark | CSI 300 | HSI | S&P 500 | | Pool | 5000+ stocks | 78 HSI constituents | 143 S&P 500 |

Switch markets in one line:

MARKET: US

DATAMODULE: examples.usdata_yfinanceBring your own data. Write a 7-function Python adapter for Bloomberg, AkShare, Binance, or any source — see interface spec.

How It Works

┌─────────────────────────────────────────────┐

│ You (natural language) │

├─────────────────────────────────────────────┤

│ AI Coding Assistant │

│ (Cursor / Windsurf / Claude Code / ...) │

├─────────────────────────────────────────────┤

│ Alpha Skills (7 SKILL.md) │

│ discover · evaluate · mine · library │

│ backtest · monitor · report │

├─────────────────────────────────────────────┤

│ Python (pandas/numpy/scipy/matplotlib) │

│ → factor computation │

│ → IC/ICIR/quintile evaluation │

│ → portfolio backtesting │

│ → SQLite factor registry │

├─────────────────────────────────────────────┤

│ Data: Tushare │ YFinance │ CSV │ Custom │

└─────────────────────────────────────────────┘Zero framework dependency. Each skill is a self-contained Markdown file. The AI reads it, writes the Python, runs it. Nothing to install except standard data science packages.

Evaluation Pipeline

Your AI quant researcher doesn't just compute IC. It runs a 4-level institutional-grade evaluation:

| Level | What | Speed | |-------|------|-------| | L0 | Syntax + data validation | instant | | L1 | Quick IC screen (sampled 200 stocks × 2 years) | <30s | | L2 | Full: IC series, ICIR, quintile returns, long-short, monotonicity | 1-3 min | | L3 | Robustness: parameter perturbation, rolling window, start-date sensitivity | 5-15 min |

Plus optional qtype pre-flight — static analysis to catch look-ahead bias before you waste compute on fake alpha.

Factor Mining Engine

alpha-mine systematically searches the factor expression space:

3 mining strategies:

- Template-based — momentum, mean-reversion, volatility, volume, composite templates × multiple window sizes

- Combinatorial — chain operators:

csrank(tscorr(close, volume, 20)) - Mutation — take a known strong factor, mutate parameters/operators

Overfitting guard: Every surviving factor gets an economic intuition score (Strong / Moderate / Weak). Factors without a clear behavioral story are flagged as potential data mining.

Built-in Factors (25+)

| Category | Factors | |----------|---------| | Price-Volume | momentum · reversal · volatility · pvdiverge · rsi · macd · bollinger · atrratio · turnover · abnormal_turnover | | Fundamental | roe · roa · grossmargin · netprofitgrowth · revenuegrowth | | Valuation | pettm · pb · psttm · dividend_yield · peg | | Composite | qualityscore · valuescore · growth_momentum |

All gate checks and evaluation thresholds are user-configurable:

GATE_SHARPE: 1.0

GATEMAXDRAWDOWN: -0.25

GATEPROFITFACTOR: 1.0

EVALICIRSTRONG: 0.5What's New

v0.3 — Autopilot & Live Signals

alpha-signal: daily trading signal generator — outputs target portfolio from active factorsalpha-autopilot: autonomous research loop — auto-mine, evaluate, register, monitor, retire- Professional knowledge base: 6 expert-level reference documents (2,795 lines)

alpha-mine: systematically search factor expression space, IC screen, economic intuition scoring- All skills fully self-contained — zero external package dependencies

- Optional qtype pre-flight check

- 7 core skills · A-share/HK/US support · bilingual EN/ZH · multi-platform

Roadmap

- [x] 9 skills (discover / evaluate / mine / library / backtest / monitor / report / signal / autopilot)

- [x] Daily signal generation (target portfolio output)

- [x] Autonomous research loop (mine → evaluate → register → monitor → retire)

- [x] Professional knowledge base (6 expert-level documents, 2,795 lines)

- [x] A-share, HK, and US market support

- [x] Market-aware trading rules

- [x] Automated factor mining (template + combinatorial + mutation)

- [x] Custom data source support

- [x] Multi-platform (Cursor, Windsurf, Claude Code, ChatGPT, local models)

- [x] qtype integration for static code checks

- [ ] Portfolio construction (factor → tradeable portfolio)

- [ ] Market regime detection & factor-regime mapping

- [ ] Factor crowding detection

- [ ] Web UI dashboard

License

Apache 2.0

Contributing

See CONTRIBUTING.md — add skills, data adapters, or improve methodology.

Stop writing boilerplate. Start finding alpha.

Built by quants who got tired of copy-pasting the same IC calculation for the 500th time.