Option pricing using Black-Scholes model, Bachelier model, Binomial Trees and Monte Carlo simulation under different stochastic processes

Option Pricer

This is a Python project made to apply what I've learned about option pricing during my MSc in Finance.References

- Hull, J. (2014) Options, Futures and Other Derivatives. 9th Edition

- A Black–Scholes user’s guide to the Bachelier model: https://arxiv.org/pdf/2104.08686.pdf

- Iacus, S.M. (2011) Option Pricing and Estimation of Financial Models with R

How to run

- Clone the repository or download it as ZIP file

- Run

(optional)install -r requirements.txt - Run

.py [arguments]

Requirements

numpyscipymatplotlib

Usage

- Supported underlying assets:

| Argument | Description | |----------|---------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------| | h | Print help message | | m | Pricing Method

- Black-Scholes model,

-m BS - Bachelier model,

-m BA - Binomial Tree,

-m BT - Monte Carlo Simulation,

-m MC

- European options:

EUC(call),EUP(put) - American options:

USC(call),USP(put) - Futures-style options:

FSTYLEC(call),FSTYLEP(put) - Bond options:

BC(call),BP(put)

-d 0.5 0.5 0.5 | | dt | Dividend Times. It refers to the times in which the dividends will be paid. In the example above we'll set: -dt 0.5 1 1.5 | | t | Time to Expiration. It can be expressed in different ways:- Years, using only a float value e.g.

-t 1 - Months, by adding "m" or "months" to a number e.g

-t 12 m - Weeks, by adding "w" or "weeks" e.g.

-t 52 w - Days, by adding "d" or "days" e.g.

-t 252 d

If it isn't included when the Bachelier pricing model is selected, the tool will automatically convert log-normal volatility in normal volatility. | | b | Current Bond Cash Price | | i | PV of Bond's Income | | steps | Number of Steps. Number of steps to use in the binomial tree. | | print | Print the Binomial Tree | | greeks | Print the Values of Delta, Theta, Gamma, Vega and Rho | | n | Number of Simulations | | process | Underlying process

- Geometric Brownian Motion,

-process GBM - Variance-Gamma Process,

-process VG - Merton Jump Process,

-process MJ

Examples

European option

A financial institution has just sold 1,000 seven-month European call options on the Japanese yen. Suppose that the spot exchange rate is 0.80 cent per yen, the exercise price is 0.81 cent per yen, the risk-free interest rate in the United States is 8% per annum, the risk-free interest rate in Japan is 5% per annum, and the volatility of the yen is 15% per annum. Calculate the delta, gamma, vega, theta, and rho of the financial institution’s position. Interpret each number

Black-Scholes

Input:python main.py -p EUC -s 0.8 -k 0.81 -r 0.08 -rf 0.05 -vol 0.15 -t 7 m -greeksOutput:

INFO - pricers - Pricing using Black-Scholes

INFO - main - The option price is: 0.03741

INFO - main - The Greeks are: Theta -0.03989 | Delta 0.52493 | Gamma 4.20593 | Vega 0.23553 | Rho 0.22315Bachelier

Input:python main.py -p EUC -s 0.8 -k 0.81 -r 0.08 -rf 0.05 -vol 0.15 -t 7 m -m BAOutput:

INFO - pricers - Pricing using Bachelier

INFO - main - The option price is: 0.03751Monte Carlo Simulation under GBM

Input:python main.py -p EUC -s 0.8 -k 0.81 -r 0.08 -rf 0.05 -vol 0.15 -t 7 m -m MC -n 5000Output:

INFO - pricers - Pricing using Monte Carlo Simulation

INFO - pricers - Pricing under Geometric Brownian Motion

INFO - main - The option price is: 0.03679Monte Carlo Simulation under Variance-Gamma process

Input:python main.py -p EUC -s 0.8 -k 0.81 -r 0.08 -rf 0.05 -vol 0.15 -t 7 m -m MC -n 5000 -process VG -params 0.02 1Output:

INFO - pricers - Pricing using Monte Carlo Simulation

INFO - pricers - Pricing under Variance Gamma Process

INFO - main - The option price is: 0.04568European option (dividend)

Consider a European call option on a stock when there are ex-dividend dates in two months and five months. The dividend on each ex-dividend date is expected to be $0.50. The current share price is $40, the exercise price is $40, the stock price volatility is 30% per annum, the risk-free rate of interest is 9% per annum, and the time to maturity is six months.Input:

python main.py -p EUC -d 0.5 0.5 -dt 0.16667 0.41667 -s 40 -k 40 -vol 0.3 -r 0.09 -t 0.5Output:

INFO - pricers - Pricing using Black-Scholes

INFO - main - The option price is: 3.67123Futures-style option

The strike price of a futures option is 550 cents, the risk-free rate of interest is 3%, the volatility of the futures price is 20%, and the time to maturity of the option is 9 months. The futures price is 500 cents ... (d) What is the futures price for a futures style option if it is a call?Input:

python main.py -p FSTYLEC -f 5 -k 5.5 -r 0.03 -vol 0.2 -t 0.75Output:

INFO - pricers - Pricing using Black-Scholes

INFO - main - The option price is: 0.16564Bond option

Use the Black’s model to value a one-year European put option on a 10-year bond. Assume that the current value of the bond is $125, the strike price is $110, the one-year risk-free interest rate is 10% per annum, the bond’s forward price volatility is 8% per annum, and the present value of the coupons to be paid during the life of the option is $10Input:

python main.py -p BC -b 105 -i 34.968 -r 0.1 -t 4 -vol 0.02 -k 100Output:

INFO - pricers - Pricing using Black-Scholes

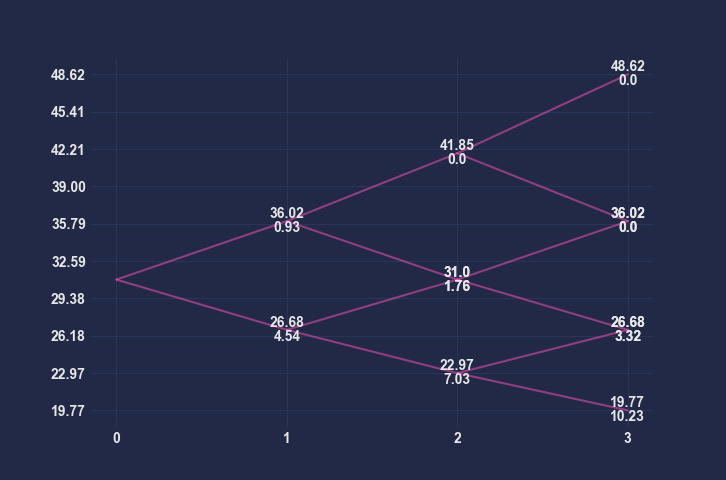

INFO - main - The option price is: 3.19007American Option

Three-step tree to value an American 9-month put option on a futures contract when the futures price is 31, strike price is 30, risk-free rate is 5%, and volatility is 30%

Input:

python main.py -m BT -steps 3 -p USP -f 31 -k 30 -r 0.05 -vol 0.3 -t 9 m -printOutput:

INFO - pricers - Pricing using Binomial Tree INFO - main - The option price is: 2.83564