Application of reinforcement learning in trading financial markets.

Last updated May 15, 2024

20

Stars

6

Forks

0

Issues

0

Stars/day

Attention Score

14

Language breakdown

No language data available.

▸ Files

click to expand

README

Madigan

Code Associated with the paper Reinforcement Learning for Trading in Financial Markets: Theory and ApplicationsAims

This repository contains a framework for conducting experiments exploring the use of reinforcement learning in trading financial markets. With a focus on statistical arbitrage, the eventual goal is to create autonomous systems for making trading decisions and executing them. The process will be much like scientific inquiry whereby hypotheses will be succesively tested in a directed manner. To this end, robust software is needed to allow for the process of implementing, validating and deploying ideas, along without the necessary hardware to allow for running experiments.Approach

Current approach consists of formalizing the trading problem/context in the Markov decision process (MDP) framework. An agent makes decisions in interacting with an environment via a defined action space, seeking to maximize rewards given by the environment.*agent -> trader

environment -> 'market', broker, exchange, data, participants

action space -> buy/sell/hold, desired portfolio

reward -> equity returns / sharpe / sortino, transaction costs*

Main Components

Environment

Should serve the main roles of Broker/Exchange, data source and subsequently pre-processors.- Written in C++ with bindings to python - gives peace of mind with respect to speed.

- Currently contains bare minimum functionality for accounting and provides an interface where desired

Objective Function

Objective function and reward shaping for rl should reflect the objectives of a trader. I.e risk-adjusted returns, margin constraints, transaction costs etc Currently Implemented: - Raw Log returns - Naive sharpe and sortino aggregations - Differential sharpe and sortino updates (DSR & DDR) - Proximal Portfolio Constraint (PPC, see paper)Input Space

The input space refers to the representation of data which is presented to any model or agent. This may be a matrix with dimensions corresponding to time, asset , features etc. Or it could be a flat vector containing the corresponding compressed information. Raw data is obtained from a dataSource which is the source of data returned by the environment through env.step() and available via env.dataSource. This data is sent to the preprocessor which does its job. - Currently the default preprocessor just concatenates a sliding window of observations. - Several different normalization schemes available. When using CNNs on raw price, log transform is often enough.RL Algorithm (Agent)

Rl algorithms should be as simple as possible while performing the tasks, and advanced methods should be incrementally integrated. This neccesiates a modular design of Agent classes. Currently implemented:- Deep Q learning (DQN) + Rainbow components: Noisy Nets, PER, Dueling, Double

- Implicit Quantile Networks (IQN)

- Deep Deterministic Policy Gradient (DDPG) (work in progress in terms of translating model output to transactions, works for long/short only but numerically unstable if allowing both)

- Contrastive Unsupervised Representation Loss (CURL)

Partially implemented / In Progress:

- RQDN - Recurrent DQN as a base for recent improvements in recurrent rl such as agent 57

- Soft Actor Critic (SAC) - need to fix bugs

Function Approximation

Given an RL algorithm, a suitable model must be placed as the core agent. Neural Networks are good general function approximators, and despite high degrees of freedom, can often generalize well, are composable and provide opportunity for customization. Currently Implemented:- Convolutional Neural Networks (CNNs)

Usage

See the default config file at madigan/config.yaml for a templateGiven a config file conf.yaml, from the project base directory:

python madigan/train.py /path/to/conf.yaml -nsteps 1000000bash madigan/train.sh 1000000DashBoard

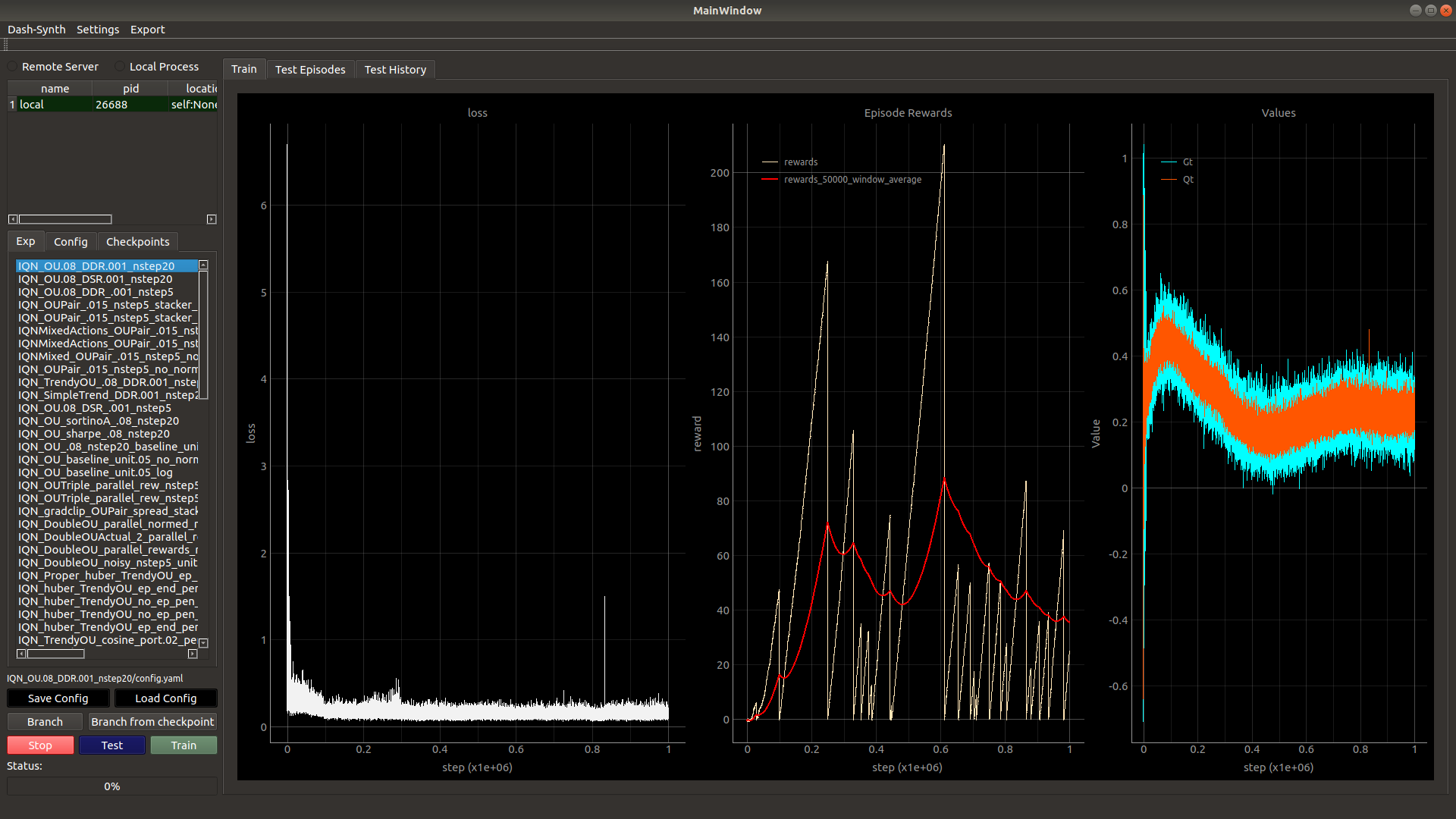

The dashboard is really handy when evaluating experimental results. As it is written using pyqt5 and pyqtgraph, it is native and cross-platform. When using for the first time, the app will prompt for the folder where all experiment logs are kept (determined by savepath/datapath in your config file), with sub-folder in that folder assumed to be the experiment name and containing the log data. This can be changed by going to the Settings tab then -> Set Experiments Folder. From the base directory:python madigan/run_dash.py

Installation

Requirements:- C++ 17 Compiler

- CMake

- Pybind11

- Eigen

- CUDA+CuDNN - if using gpu - recommended

- Python 3.7 >=

Install c++ components as shared library via:

(from project base directory)

cd madigan/environments/cpp

mkdir build && cd build

cmake ..

make

make test(from project base directory)

python setup.py installpip install .To Do

- [X] Train agents to trade Sine Waves

- [X] Train agents to trade OU Process

- [X] Train agents to trade trending series

- [X] Train agents to trade noisier trending series

- [X] Compose many different series and test multi asset allocation

- [X] Train on synthetic series with multi asset stat arb opportunities

- [X] Train on groups of synthetic series.

- [X] HDFDataSource for market data

- [ ] Order semantics (I.e Market vs Limit/Timed/Stop etc).

- [ ] Wrap Broker, Account, Portfolio into a backtesting co-ordinator (event driven)

- [ ] Feature Engineering and training on market data

- [ ] Perform backtests and classify agents into a taxonomy (I.e risk profile,