[NeurIPS 2025 & ICLR 2025 Financial AI Best Paper Award] A multi-agent framework that leverages LLMs to simulate socio-economic systems

TwinMarket: A Scalable Behavioral and Social Simulation for Financial Markets

![]()

![]()

![]()

![]()

![]()

![]()

## 💡 Update

- 09/2025: TwinMarket was accepted to NeurIPS 2025. See you in San Diego! 🌊

- 04/2025: TwinMarket won the Best Paper Award 🏆 at the Advances in Financial AI Workshop @ ICLR 2025.

📖 Overview

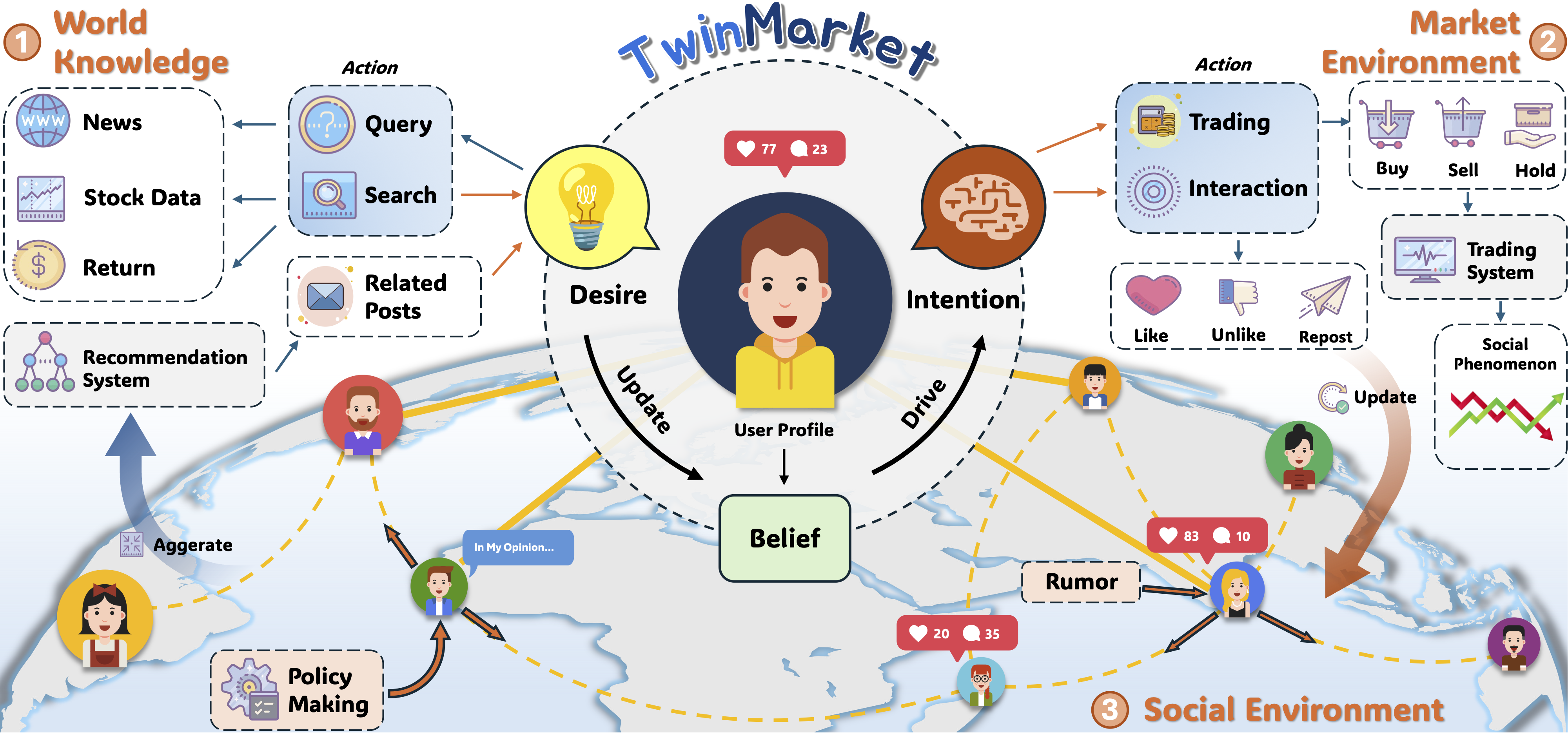

TwinMarket is an innovative stock market simulation system powered by Large Language Models (LLMs). It simulates realistic trading environments through multi-agent collaboration, covering personalized trading strategies, social network interactions, and news/information analysis for an end-to-end market simulation.

🎯 Key Features

- 🤖 Intelligent Trading Agents: LLM-driven, personalized decision-making

- 🌐 Social Network Simulation: Forum-style interactions and user relationship graphs

- 📊 Multi-dimensional Analytics: Technical indicators, news, and market sentiment

- 🎲 Behavioral Finance Modeling: Includes disposition effect, lottery preference, and more

- ⚡ High-performance Concurrency: Scalable simulation for large user populations

- 📈 Real-time Matching Engine: Full order matching and execution

🚀 Quick Start

# Configure your API and embedding models

cp config/api_example.yaml config/api.yaml

cp config/embedding_example.yaml config/embedding.yaml

Run the demo

bash script/run.sh📝 Development Guide

Extend Trading Strategies

Implement new strategies in trader/trading_agent.py:

def customstrategy(self, marketdata):

"""Custom trading strategy"""

# Implement your strategy logic here

passAdd New Evaluation Metrics

Add metrics in trader/utility.py:

def calculatecustommetric(trades):

"""Compute custom metric"""

# Implement metric calculation here

pass📚 Awesome Papers Using TwinMarket

We welcome community contributions. If your paper uses TwinMarket, feel free to open a PR and add it here.

| Title | Code | Paper | | --- | --- | --- | | Interpreting Emergent Extreme Events in Multi-Agent Systems | https://github.com/mjl0613ddm/IEEE | https://arxiv.org/abs/2601.20538 |

🧾 Citation

@inproceedings{yang2025twinmarket,

title = {TwinMarket: A Scalable Behavioral and Social Simulation for Financial Markets},

author = {Yuzhe Yang and Yifei Zhang and Minghao Wu and Kaidi Zhang and

Yunmiao Zhang and Honghai Yu and Yan Hu and Benyou Wang},

booktitle = {The Thirty-ninth Annual Conference on Neural Information Processing Systems (NeurIPS)},

series = {NeurIPS},

volume = {39},

year = {2025},

url = {https://arxiv.org/abs/2502.01506}

}📄 License

This project is licensed under the MIT License. See LICENSE for details.