📈 Personae is a repo of implements and environment of Deep Reinforcement Learning & Supervised Learning for Quantitative Trading.

![]()

![]() [

[![]() ]()

]() ![]()

Personae - RL & SL Methods and Envs For Quantitative Trading

Personae is a repo that implements papers proposed methods in Deep Reinforcement Learning & Supervised Learning and applies them to Financial Market.

Now Personae includes 4 RL & 3 SL implements and a simulate Financial Market supporting Stock and Future. (Short Sale is still implementing)

More RL & SL methods are updating!

WARNING

This repo is being reconstructing,

It will start from 2018-08-24 to ~2018-09-01~ a timestamp that I successfully found a job.

Attentions

- The features as inputs are naive.

- Day frequency is clearly not enough.

- It's recommended that you could replace the features here to your own.

Contents

Implement of DDPG with TensorFlow. > arXiv:1509.02971: Continuous control with deep reinforcement learning Implement of Double-DQN with TensorFlow. > arXiv:1509.06461: Deep Reinforcement Learning with Double Q-learning Implement of Dueling-DQN with TensorFlow. > arXiv:1511.06581: Dueling Network Architectures for Deep Reinforcement Learning Implement of Policy Gradient with TensorFlow. > NIPS. Vol. 99. 1999: Policy gradient methods for reinforcement learning with function approximation Implement of arXiv:1704.02971, DA-RNN with TensorFlow. > arXiv:1704.02971: A Dual-Stage Attention-Based Recurrent Neural Network for Time Series Prediction Implement of TreNet with TensorFlow. > IJCAI 2017. Hybrid Neural Networks for Learning the Trend in Time Series Implement of simple LSTM based model with TensorFlow. > arXiv:1506.02078: Visualizing and Understanding Recurrent NetworksEnvironment

A basic simulate environment of Financial Market is implemented.

Implement of Market, Trader, Positions as a gym env (gym is not required), which can give a env for regression or sequence data generating for RL or SL model. For now, Market support Stock Data and Future Data.Also, more functions are updating.

Experiments

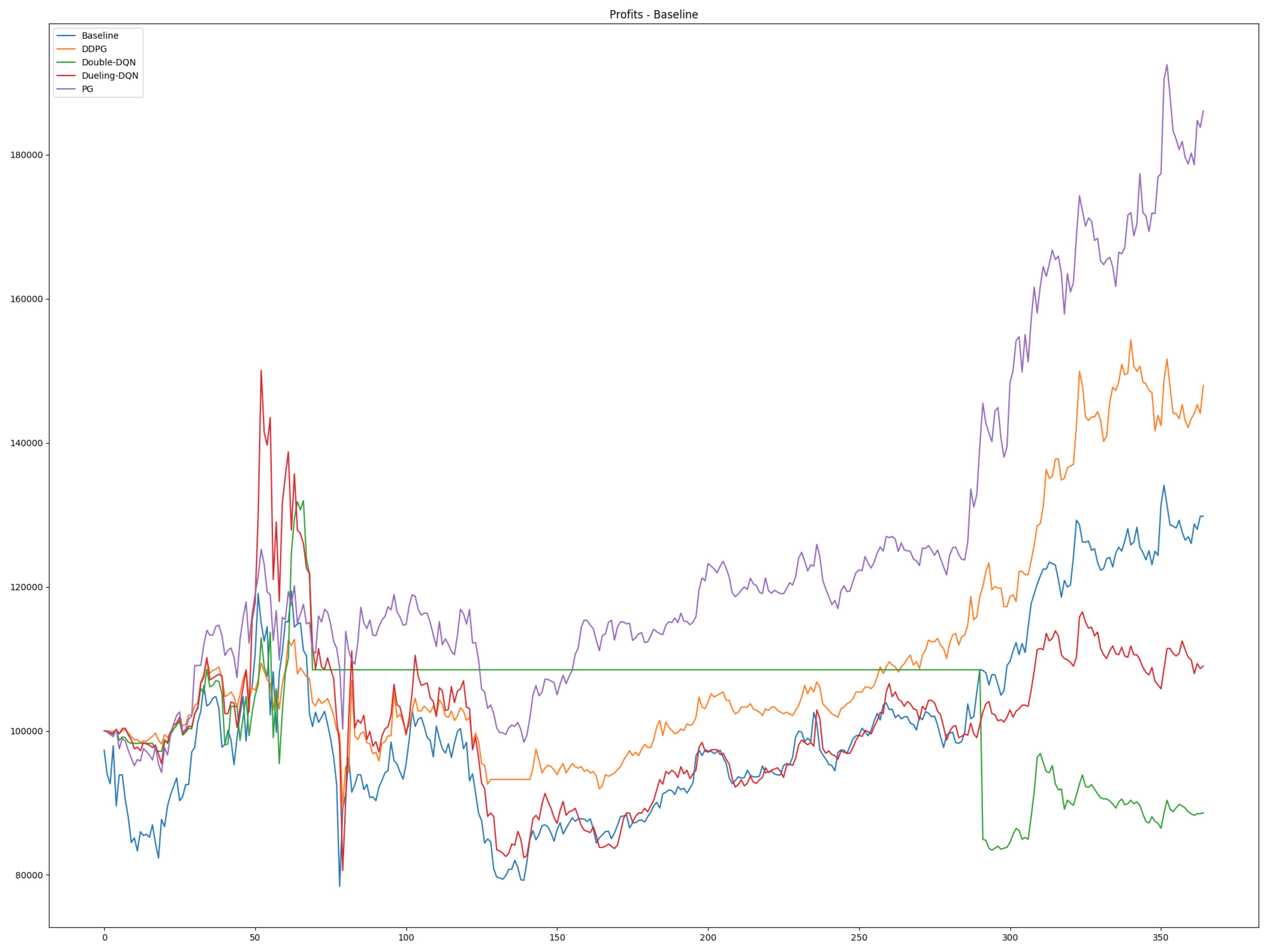

Train a Agent to trade in stock market, using stock data set from 2012-01-01 to 2018-01-01 where 70% are training data, 30% are testing data.  Total Profits and Baseline Profits. (Test Set)

Total Profits and Baseline Profits. (Test Set)

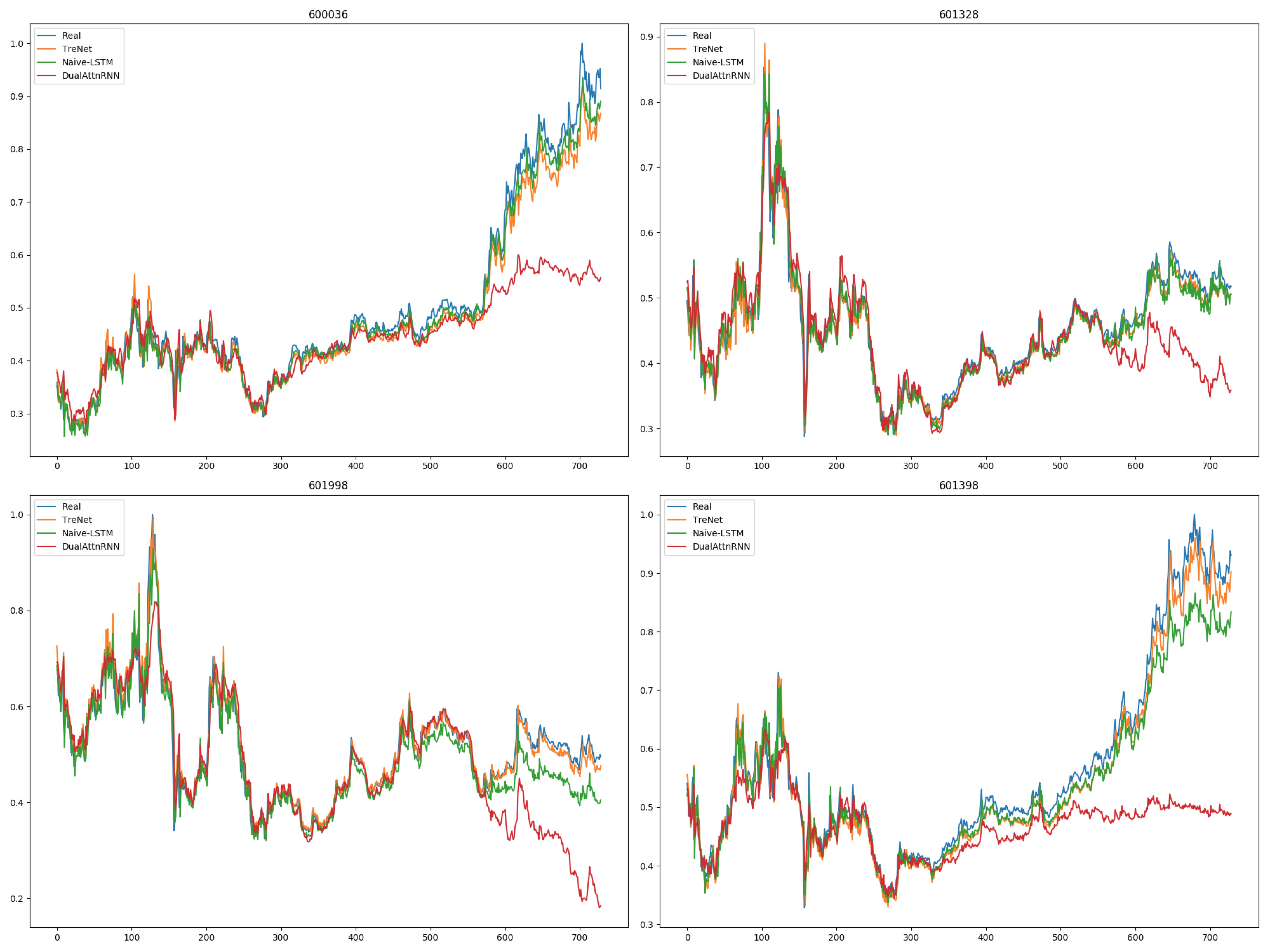

Prices Prediction Experiments on 4 Bank Stocks. (Test Set)

Prices Prediction Experiments on 4 Bank Stocks. (Test Set)

Requirements

Before you start testing, following requirements are needed.

- Python3.5

- TensorFlow1.4

- numpy

- scipy

- pandas

- rqalpha

- sklearn

- tushare

- matplotlib

- mongoengine

- CUDA (option)

- ta-lib (option)

- Docker (option)

- PyTorch (option)

How to Use

If you use Docker

About base image

My image for this repo is ceruleanwang/personae, and personae is inherited from ceruleanwang/quant-base. The image ceruleanwang/quant-base is inherited from nvidia/cuda:8.0-cudnn6-runtime. So please make sure your CUDA version and cuDNN version are correct.Instructions

First you should make sure you have stocks data in your mongodb.If you don't have, you can use a spider writen in this repo to crawl stock or future data, but before you start, you should make sure a mongodb service is running.

If you don't have mongodb service running, you can also use a mongodb container (option) by following code:

docker run -p 27017:27017 -v /data/db:/data/db -d --network=your_network mongodocker run -t -v localprojectdir:dockerprojectdir --network=yournetwork ceruleanwang/personae spider/stockspider.pydocker run -t -v localprojectdir:dockerprojectdir --network=yournetwork ceruleanwang/personae spider/futurespider.pystock_codes = ["600036", "601328", "601998", "601398"]future_codes = ["AU88", "RB88", "CU88", "AL88"]docker run -t -v localprojectdir:dockerprojectdir --network=yuornetwork ceruleanwang/personae algorithm/RL or SL/algorithmname.pyIf you use Conda

You can create an env yourself, and install Python3.5 and all dependencies required, then just run algorithm in your way.One thing should be noticed is that the hostname in mongoengine config should be your own.

About training & testing

For now, all models implemented with TensorFlow support persistence. You can edit many parameters when you are training or testing a model. For example, following codes show some parameters that could be edited.env = Market(codes, startdate="2008-01-01", enddate="2018-01-01", **{

"market": market,

"mixindexstate": True,

"trainingdataratio": trainingdataratio,

})

algorithm = Algorithm(tf.Session(config=config), env, env.trader.actionspace, env.datadim, **{ "mode": mode, "episodes": episode, "enable_saver": True, "enablesummarywriter": True, "savepath": os.path.join(CHECKPOINTSDIR, "RL", model_name, market, "model"), "summarypath": os.path.join(CHECKPOINTSDIR, "RL", model_name, market, "summary"), })

TODO

- More Implementations of Papers.

- More High-Frequency Stocks Data.