Autonomous arbitrage scanner - monitors price spreads across 4 Solana DEXes, evaluates paths with Claude, executes in milliseconds.

Cascade

Autonomous cross-venue arbitrage scanner for Solana. Monitors price spreads across four DEXes every 3 seconds and uses a Claude agent to evaluate, simulate, and execute opportunities before they close.

Live Arbitrage Scanner

Real-time scanner view for Cascade: live venue quotes from Jupiter, Raydium, Orca, and Meteora, selected opportunity, route quality checks, decision queue, recent opportunity log, and guardrails that keep stale or low-quality spreads out of execution.

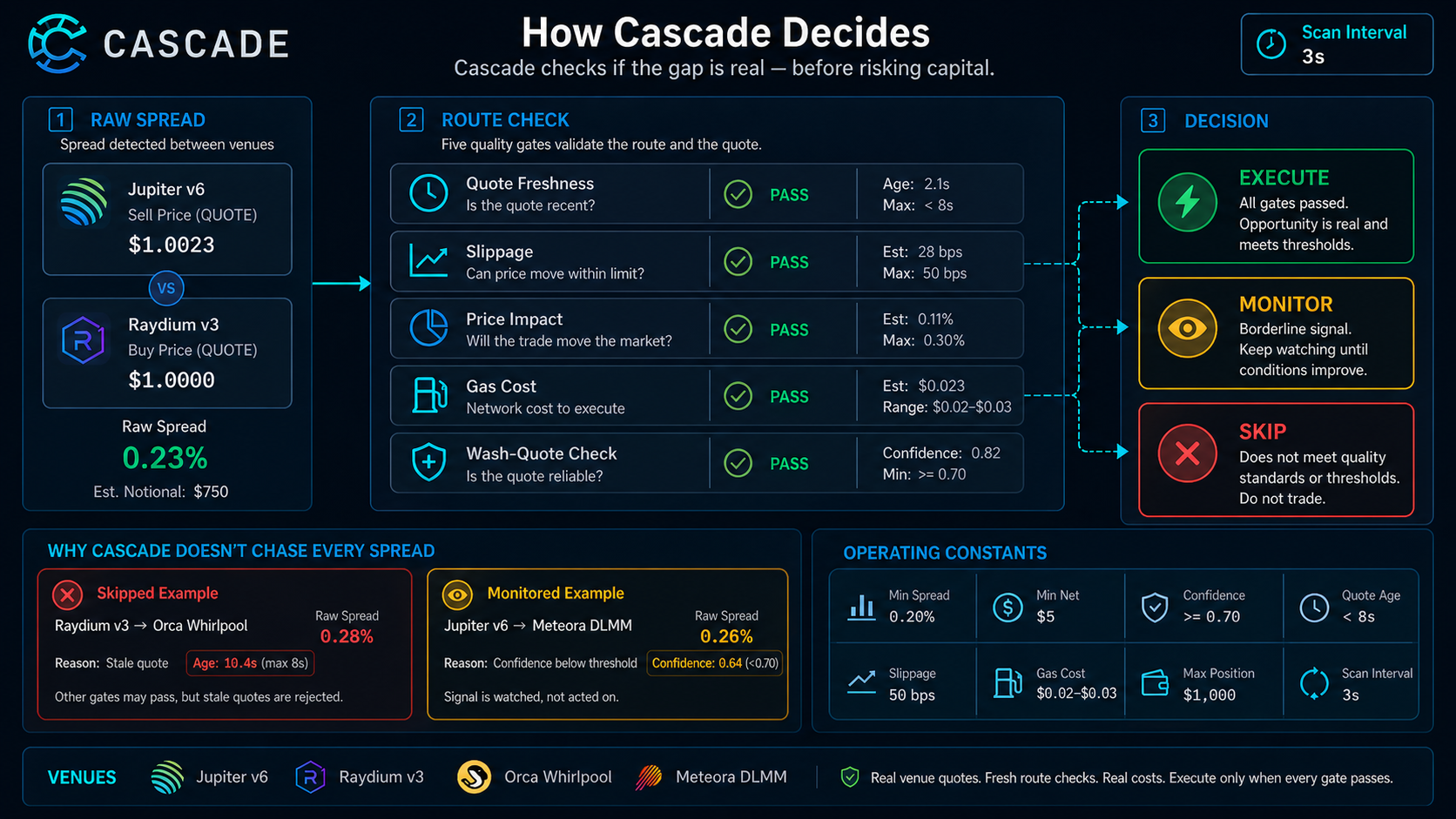

How Cascade Decides

Cascade checks whether the price gap is real before risking capital: raw spread detection, quote freshness, slippage, price impact, gas, wash-quote checks, and the final EXECUTE, MONITOR, or SKIP decision.

The opportunity

Prices across Solana DEXes are never perfectly synchronized. Jupiter, Raydium, Orca, and Meteora each run independent AMM curves — when one updates faster than the others, a window opens. Most windows are under 0.1% and close in seconds. The ones worth taking average 0.2–0.5% and last 3–15 seconds.

Cascade watches all four venues simultaneously, finds those windows, and lets Claude decide whether to act.

What it does

Every 3 seconds:

- Scan — fetch prices for all watched pairs from Jupiter, Raydium, Orca, and Meteora in parallel

- Spread — compute best bid/ask across venues, flag pairs where spread exceeds

MINSPREADPCT - Find paths — for each viable spread, calculate an arb path with gas-adjusted net profit

- Agent evaluates — Claude calls

simulate_pathto apply price impact + slippage, then issuesEXECUTE,SKIP, orMONITOR - Execute — approved paths go through

TradeExecutor(paper mode by default)

Agent decision loop

The Claude agent has two tools per evaluation:

simulate_path → refines gross profit with price impact + slippage model

arb_decision → final verdict: EXECUTE | SKIP | MONITORIt always simulates before deciding. If the post-simulation profit drops below MINNETPROFIT_USD, it skips regardless of the raw spread. This filters out a large class of false positives from stale quotes.

Quickstart

git clone https://github.com/YOUR_USERNAME/cascade

cd cascade

bun install

cp .env.example .env # fill in ANTHROPICAPIKEY + HELIUSAPIKEY

bun run dev # paper trading by defaultRun the historical simulation:

bun run simConfiguration

| Variable | Default | Description | |----------|---------|-------------| | PAPER_TRADING | true | Safe default — no on-chain execution | | MINSPREADPCT | 0.20 | Minimum spread to trigger agent evaluation | | MINNETPROFIT_USD | 5 | Minimum post-gas, post-slippage profit | | MAXPOSITIONUSD | 1000 | Max size per arb trade | | SLIPPAGE_BPS | 50 | Slippage tolerance (0.5%) | | SCANINTERVALMS | 3000 | Price fetch frequency | | WATCH_PAIRS | SOL/USDC,... | Comma-separated pairs to monitor | | CONFIDENCE_THRESHOLD | 0.70 | Minimum agent confidence to execute |

Adding a venue

Create venues/your-venue.ts extending BaseVenue, implement getPrice() and isHealthy(), then add it to PriceMonitor.venues in scanner/monitor.ts. The rest of the pipeline picks it up automatically.

Technical Spec

Price Impact Model — Constant Product AMM

Cascade uses a Constant Product approximation for price impact estimation on Raydium v3 and Orca Whirlpool:

impactFactor = 1 − tradeSize / (reserveDepth + tradeSize)

adjustedProfit = grossProfit × impactFactorReserve depth is approximated conservatively at 20× the trade size (if the actual pool depth is unknown from the quote). This over-estimates impact, which is the correct bias — it's better to skip a profitable trade than to take a losing one.

Meteora DLMM note: DLMM bins have discrete price steps. Real impact is stepwise, not smooth. The CP model still applies as a conservative lower bound — actual impact is typically lower if the trade stays within a single bin.

Stale Quote Filter

Arb windows on Solana close in 3–15 seconds. Cascade rejects paths where the spread snapshot is older than MAXQUOTEAGE_SECONDS (default 8s) before making a Claude agent call. This avoids spending ~800ms on an agent evaluation for a spread that almost certainly no longer exists.

Data age is also passed to the agent prompt as Quote freshness: fresh | stale — the agent factors this into its confidence score.

Wash-Quote Heuristic

A spread where exactly one venue diverges > 0.3% from the median of the rest is flagged as a potential bad quote before reaching the agent:

sorted prices: [1.2340, 1.2342, 1.2343, 1.2387] ← Raydium only outlier

→ isPotentialWashQuote = true → agent scrutinizes before EXECUTEThis catches a large class of stale Jupiter aggregator quotes and venue API glitches before they reach the decision layer.

Gas Cost Model

Solana transaction cost is approximated at:

baseFee = 5000 lamports (~$0.0007 at $140/SOL) priorityFee = 100_000 lamports typical (~$0.014) total ≈ $0.015 per txA 2-leg arb (buy + sell) costs ~$0.03 in gas. This is already included in estimatedGasCostUsd before the agent sees the path. The MINNETPROFIT_USD threshold (default $5) provides 166× gas coverage.

Why No Flash Loans

Solana does not support EVM-style atomic flash loans in a single transaction. Cross-program invocations (CPIs) can compose, but there's no native "borrow-swap-repay-or-revert" primitive. Cascade executes legs sequentially with MAXPOSITIONUSD as the capital ceiling.

Stack

- Runtime: Bun 1.2

- Agent: Claude Agent SDK —

simulatepath → arbdecisiontool loop - Venues: Jupiter v6 · Raydium v3 · Orca Whirlpool · Meteora DLMM

- Simulation: price impact + slippage model before every execution decision

License

MIT